Intensifying tensions between Washington and Beijing are being offset by the US Treasury announcing that the White House is nearing trade deals with several countries. The news motivated traders to step out of the dugout and do some swinging, and the dip buying essentially turned a bloody morning into mixed results among equity benchmarks and sectors. Meanwhile, the stateside economic calendar wasn’t helpful, featuring sizeable misses on construction spending and more importantly from a corporate earnings perspective, ISM-manufacturing. And the lackluster prints aren’t pulling yields down much, since the latter release’s prices paid segment supported inflation expectations amidst bear-steepening action across the curve. Still, selling in the Treasury complex is contained and we’re seeing strong defense at 4.50% on tens and 5% on thirties. And while investors are trimming their fixed-income and greenback exposures, they are picking up stocks, commodity futures, volatility protection instruments and forecast contracts.

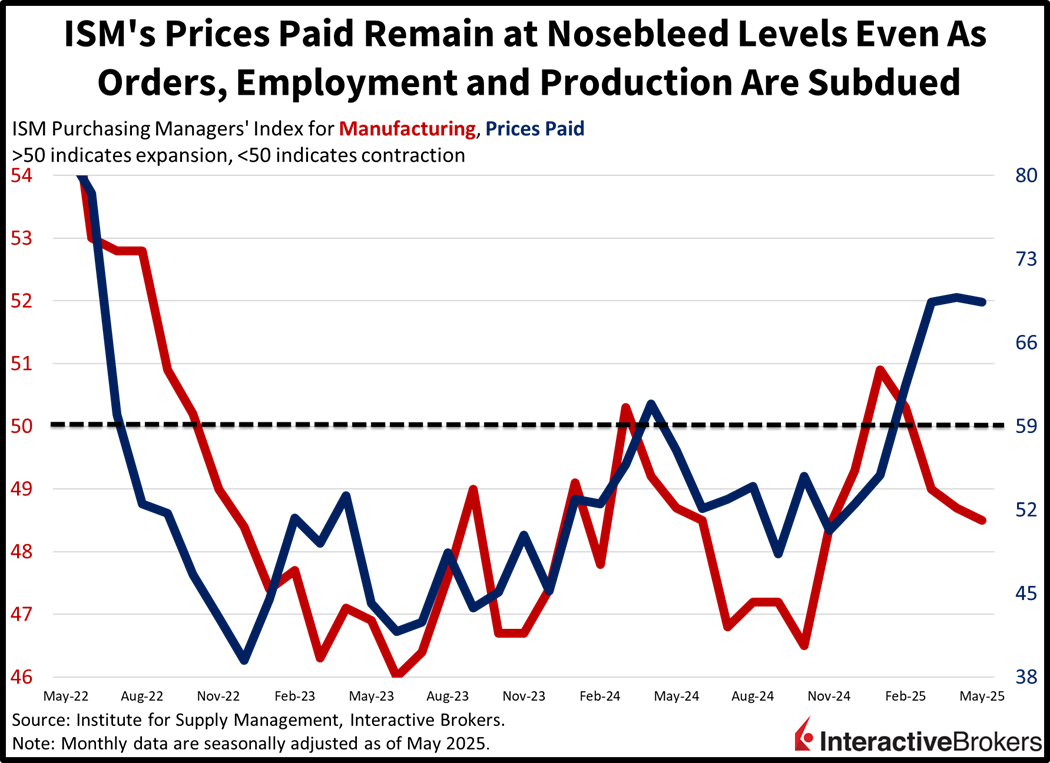

Manufacturing Contracts for the Third Consecutive Month

Conditions among goods producers contracted for the third consecutive month in May, according to the Institute for Supply Management’s (ISM) Purchasing Managers’ Index. The headline score of 48.5 arrived beneath the contraction-expansion threshold of 50, the 49.5 median estimate and April’s 48.7. Broad-based weakness existed across the report, with production, employment and new orders coming in at 45.4, 46.8 and 47.6. The lack of buying activity kept factories focused on reducing backlogs while manufacturers and customers alike lessened inventory levels. Prices, meanwhile, continue their firm upward trend, sporting a lofty 69.4 figure, down marginally from April’s 69.8, but still strongly in growth territory.

Past performance is not indicative of future results

No Customers in Sight For Builders

Elevated mortgage rates and extended prices drove a decline in April construction spending, as builders saw little reason to add supply. The headline figure retreated 0.4% month over month (m/m), its third consecutive monthly drop. It came in well below the expectation for a 0.3% uptick but shallower than the 0.8% plunge recorded in March. Fresh single-family builds weighed the most on results, with investment dollars dropping 1.1% m/m. Multi-family fared better, falling only 0.1% m/m. Other weak categories were religious, conservation/development, commercial, power and manufacturing, which experienced subtractions of 2.6%, 1.4%, 0.8%, 0.7% and 0.6%. Serving to offset some of the weakness, however, were the amusement/recreation, transportation, highway/street and health care, seeing capital expenditures increase 0.7%, 0.6%, 0.5% and 0.4% during the period.

Past performance is not indicative of future results

Closed Trade Deals to Extend Rally

This morning’s news of trade deals being near the finish line are supporting a bullish reversal in equities after mounting US-China tensions drove early volatility. Maintaining an adversarial posture against Beijing is tolerable for markets and the economy as long as there are agreements with most other cross border commerce partners. A similar dynamic occurred during Trump 1.0, a period of low inflation and robust growth. But in the very short-term folks, the economic calendar is also going to be pivotal for traders, with Tuesday bringing JOLTS and factory orders, Wednesday featuring ADP-Employment an ISM-Services, Thursday we have an update on unemployment claims and Job Friday’s main event. Investors and economists alike are hoping that labor conditions remain firm as that’ll serve to extend the economic expansion as well as support corporate earnings. So far so good, with the employment situation decelerating in a controlled way that is conducive to cooler price pressure amidst subdued joblessness.

International Roundup

UK Homebuyers Shrug Off End of Tax Holiday

After dropping 0.6% m/m in April, prices for residences climbed 0.5%, according to the Nationwide Home Price Index. The consensus estimate called for an unchanged figure. Costs also climbed 3.5% y/y in May and surpassed the estimate for a 2.9% gain as well as the 3.4% advance from the prior month. In a statement, Nationwide, which is a mortgage provider, said demand has been resilient following the March termination of a tax holiday on real estate purchases. Nationwide also believes that low unemployment, real wage gains, strong household balance sheets and the potential for moderating financing costs are likely to sustain home valuations and transaction volumes.

The Bank of England (BoE), meanwhile, reports that an increase in repayments resulted in borrowing for home financing being negative by GBP800 million in April compared to a large GBP13.0 billion jump in March. Also in April, the number of approvals declined m/m by 3,100 to 60,460 in April. Economists anticipated that 63,000 mortgages would be approved.

UK Consumer Spending Grows

Shoppers increased their use of credit cards in April, with total consumer debt issuance hitting GBP1.6 billion, up from GBP1.1 billion in the preceding month, according to the BoE. Economists anticipated no m/m/ change. The April financing boost was driven by credit card borrowing doubling to GBP800 million.

Hong Kong Retail Contraction Continues

April retail sales fell year over year (y/y) for the 14th-consecutive month, but the drop eased slightly. After sinking 3.5% in March, transactions contracted 2.3%, according to preliminary data from the Census and Statistics Department. Most significantly, durable goods sales tanked 22.9% while the clothing, footwear and allied products category sank 5.5%. Online sales also weakened, falling 8.1%. On a positive note, ecommerce, other consumers goods, foods markets, and department store sales rose 19.2%, 10.2%, 3% and 2.1%. A government spokesman says that the strengthening mainland China economy and Hong Kong’s efforts to promote tourism should improve consumption

Singapore Manufacturing Decline Slows

Singapore’s goods production continued to contract last month, but the pace moderated with the sector’s Purchasing Managers’ Index climbing from 49.6 in April to 49.7, just slightly below the contraction-expansion threshold of 50. Electronics consists of nearly one-third of the city-state’s manufacturing and that segment’s PMI strengthened from 49.8 to 49.9, according to the Singapore Institute of Purchasing and Materials Management, which provides the index.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Bond Investments

As with all investments, your capital is at risk.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account