Markets are getting hammered on Fed decision day after an escalation in Middle East hostilities drove the price of WTI crude back up towards $100. Tehran is vowing revenge on its adversaries after experiencing attacks on important energy infrastructure facilities, which is raising geopolitical angst on Wall Street. Meanwhile, a fire-hot PPI print marking the fourth consecutive month of acceleration is also sparking turbulence, as the awful February figure doesn’t include the impact of the war. The series of unfortunate events has a few fixed-income traders starting to place bets on a Fed hike this year, but those odds remain around 1%. Still, a cut is increasingly escaping the conversation, and across the Atlantic, rate watchers are already penciling in two 25-basis point increases by the European Central Bank this year as the continent, which depends on imports for fuel, responds to the oil crisis.

Markets Slide

Stocks are suffering losses across the major domestic benchmarks and the 11 sectors and subcategories, minus energy, of course. Treasuries are additionally retreating relatively evenly throughout the curve, as investors balance anticipation of a tighter central bank with rising inflation expectations, which is lifting the greenback. Non-energy commodities are lower overall. They are getting hit by weaker economic prospects, a firmer dollar and a lack of speculative enthusiasm; however, volatility protection instruments are catching bids in light of greater hedging demand.

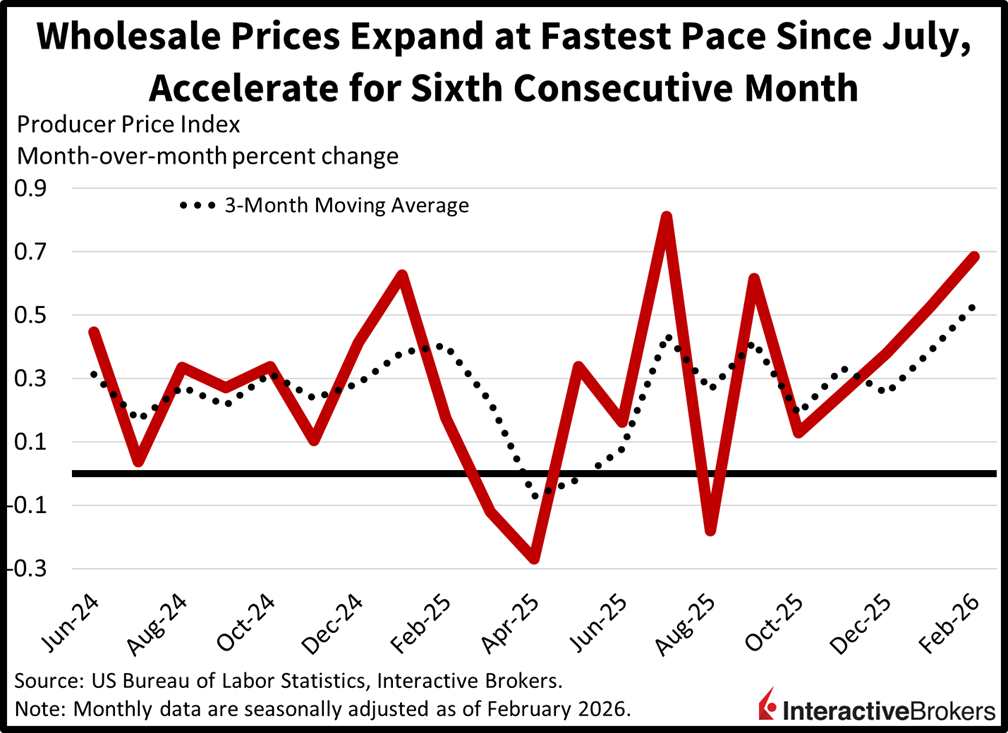

Wholesale Price Pressures Much Worse than Expected

Wholesale inflation in February accelerated for the fourth consecutive month and hit the fastest rate of increase since July, reviving fears of spiking cost forces as the numbers are from before the war started. The February Producer Price Index (PPI) jumped 0.7% month over month (m/m) and 3.4% year over year (y/y), much higher than the 0.3% and 2.9% expected and January’s 0.5% and 2.9%. The annualized figure marked a 12-month high, worrying investors that its more widely cited cousin, the CPI, will also be above 3% in a month or two, which would hamper the Fed’s ability to reduce rates. This report, meanwhile, featured broad-based m/m increases across categories as follows:

- Food, 2.4%

- Energy, 2.3%

- Other services, 0.6%

- Transportation/warehousing services, 0.5%

- Trade services, 0.4%

No major component saw a decrease.

Past performance is not indicative of future results.

March PPI Going to 4-Handle, CPI to 3

With WTI oil’s price approaching $100 again and only 13 days remaining in the month, March’s PPI and CPI results, to be released in April, are poised to carry 3- and 4-handles. Those levels would warrant hikes by the Federal Reserve and could totally turn 2026’s reacceleration playbook upside down. Starting in January, the Dow Jones Industrial and Russell 2000 indices rallied strongly and outperformed significantly in anticipation of an uptick in growth paired with several rate cuts from the US central bank this year, but this surge in energy costs is persisting for too long, and it may derail consumer spending across lower, middle and upper income households via burdensome inflation and a cap on equity valuation expansion due to heavy yields. Additionally, those headwinds, if sustained, are likely to offset the expected buoyancy stemming from larger tax refunds, milder regulations and investment incentive measures, including 100% depreciation on capital expenditures. Still, the Trump administration is confident that some semblance of Middle East peace is just around the corner; however, Wall Street is growing increasingly worried that this standoff could drive an earnings recession, similar to how the crude oil spikes of 2008 and 2022 adversely affected markets.

International Roundup

Japan Reverses Trade Deficit

Japan produced a 57.3 billion yen trade surplus in February, a strong improvement from the 1.16 billion yen deficit in January but a much weaker showing than in the year-ago period, according to the Ministry of Finance. Indeed, the surplus was down 89.8% from February 2025 when the value of items shipped abroad exceeded imports by 559.2 billion yen. The y/y weakness was driven by exports growing only 4.2%, which underperformed the economist consensus estimate for a 1.6% jump and January’s 16.8% growth. Meanwhile, imports expanded by 10.2%, which while below the 11.5% economist consensus estimate, was an acceleration from the 2.6% contraction in January. Exports to the US sank 8% with the value of car shipments tanking 14.8% in the aftermath of the US implementing tariffs on Japanese products. Demand from China also weakened with shipments to the country down 10.9% y/y, largely a result of the Lunar New Year holiday occurring in February of this year. On a positive note, EU purchases of Japanese products ascended by 14%. Demand was strong for cars and equipment for construction and mining.

Hong Kong’s Unemployment Rate Falls

Hong Kong’s unemployment rate, which was 3.9% in the November through January time frame, fell to 3.8% during the three-month period ended in February, according to the special administrative district’s Census and Statistics Department. The most significant declines in unemployment occurred in the retail category, the accommodation services industry and the foundation and superstructure sector. More broadly, the total number of employed individuals sank by 2,900, but the labor force also contracted, resulting in the lower unemployment rate.

South Korea Payroll Expansion Continues

South Korea’s ranks of the employed grew by 234,000 last month, according to the Ministry of Data and Statistics. Last month saw the largest expansion of active workers in five months.

The following sectors and the extent of their changes expanded the most:

- Health and social welfare services, 288,000 jobs

- Transportation and warehousing, 81,000,

- Arts, sports, and leisure-related services, 70,000

Canada Policymakers Hold Key Rate

Bank of Canada (BOC) policymakers agreed this morning to hold the central bank’s key overnight rate at 2.5% and its deposit rate at 2.2%. When announcing the decision, the BOC acknowledged that the labor market is sustaining elevated unemployment with a rate of 6.8% and that relatively few businesses say they plan to hire more workers. The BOC also anticipates that gross domestic product growth stalled in the fourth quarter and will only reach 1.1% this year. At the same time, the outlook is highly unclear due to “unpredictable US trade policies and geopolitical risks.”

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account