Originally posted 27 November 2024 – Global central banks ‘cut to the chase’

Key Takeaways

- Despite central banks worldwide beginning a rate-cutting cycle, inconsistent economic data and evolving inflation trends mean investors should prepare for potential market volatility heading into 2025.

- As the US election and evolving geopolitical tensions reshape trade and fiscal policies, markets in the US, Europe, and Asia are adjusting to unique regional challenges and opportunities driven by economic resilience, interest rate shifts, and sector-specific tailwinds.

- Japan’s equity markets present a compelling valuation opportunity, yet sustained growth will require corporate governance reforms and increased returns on equity to capture global investor interest.

- The UK’s expansionary budget may bolster short-term growth but has raised fiscal risks, impacting gilt yields and potentially slowing the pace of future Bank of England rate cuts as inflationary pressures linger.

- Surging central bank gold purchases reflect a pivot towards alternative reserves amidst rising global uncertainty, signalling a sustained demand for gold as a safe-haven asset even as prices remain high.

This blog summarises the key findings of our latest Global Edge: Global Central Banks “Cut to the Chase”.

As we approach 2025, global investors are confronted with a different landscape to twelve months ago. While central bank rate cuts were expected to occur in 2024, the timing and magnitude of what has transpired did not necessarily live up to market expectations. Nevertheless, the rate cutting process has begun for a number of central banks and, in all likelihood, will continue into the new year.

US Fed watch

There is no ‘one size fits all’ dynamic in central bank monetary policy and the US certainly was in no hurry to loosen policy earlier in 2024 when other central banks were cutting. Then, in September 2024 when the US Federal Reserve (Fed) cut interest rates for the first time in over 4 years, it went big, chopping rates by 50bps in one swipe. The Fed had been working under the assumption that the economy and labour market had been cooling faster than they previously thought. A drop in bond yields and US dollar depreciation in September, indicated the market was expecting an accelerated catchup by the Fed. However, resilience in economic data and inflationary pressures have led the market to once again revise its view. The Fed cut by only 25bps in November and Chairman Powell has been sowing the seeds of doubt about scale and pace of further moves.

Obviously, monetary policy remains highly data dependent. Another quarter-point reduction in the Fed Funds rate seems a likely scenario for the December Federal Open Market Committee (FOMC) meeting, data permitting. But this is where things could get very interesting. If the economic/labour market data continues to show signs of not cooling too much, and inflation gets ‘sticky’ around current levels, a reasonable case scenario could involve the Fed taking a pause to reassess things to begin 2025. That doesn’t necessarily mean the rate cut cycle would end. However, the policymakers would have already cut rates by 100 bps in this backdrop, so perhaps Powell & Co. ‘taking stock’ could make sense.

A post-election/post-Fed look at US Treasuries

Regardless of who won the Presidential election, we were expecting US budget deficits to continue rising. In the fiscal year (FY) 2024, the deficit came in at $1.8 trillion, or +8.1% increase higher than FY 2023’s deficit of $1.7 trillion. Higher deficits are funded by higher Treasury issuance, which drives bond yields up. Normally issuance volume is a secondary or tertiary driver of bond yields, with macro and monetary policy drivers being the primary driver. Trump’s US Presidential election win, combined with a ‘red sweep’ with the Republicans controlling both chambers of Congress, paves the way for decisive policy change. This outcome has placed more focus on deficits. Certainly, markets appear to view the red sweep as more pro-growth and inflationary than other outcomes and, thus, bond yields have risen.

Figure 1: US Treasury yields

Source: Bloomberg, as of 8/11/2024. Historical performance is not an indication of future performance and any investments may go down in value.

We believe market focus will shift back towards macro-economic data and the Fed. Instead of focusing on how high the UST 10-Year yield may be headed, the more pertinent question is whether it can go back down to its mid-September levels. Unless the labour market data collapses, the answer would be no, with yields more than likely remaining elevated in the months ahead.

Japan’s elusive rate hikes

The Bank of Japan had been slow rolling its pace of interest rate hikes while it waited for US election results. Knowing the chemistry between the country’s leaders appears be an important factor in determining the course of the Japanese economy.

The yen has stabilised after the carry trade blew up in late July and early August. That happened when the market came to the sudden conclusion that the Fed would aggressively cut rates while the Japanese central bank would seemingly do the opposite, an occurrence that sent traders panicking out of their short yen positions. The sudden rush into yen sent the forex pair from Y162 before the comeuppance to levels below Y141 by mid-September. As we write, the exchange rate is Y153, owing to the market’s repricing of the Fed’s 2025 path to something more benign than previous intimations.

There is still plenty of room for an upside valuation rerating for Japanese stocks, if for no other reason than the US stock market’s relentless rise could drag other developed markets along with it. But for a sustainable move, Japan’s aggregate Return on Equity (ROE) will need to improve. At 9.0%, it is languishing compared to US’s 17.8% . The efforts by the Tokyo Stock Exchange to motivate corporations to boost profitability may help.

China: waiting for the bazooka

China’s most recent stimulus package called for a CNY10 trillion ($1.4tn) package of debt swaps to aid local governments. It was useful, but a very narrow form of stimulus and the market was expecting more. Faced with a threat of 60% tariffs from the US, China needs a bazooka and this policy announcement is insufficient. China may be keeping dry powder aside for when it has clarity about trade restrictions under the new administration in 2025.

A series of other stimulus announcements had been made earlier in the year, including initiatives to reduce the down payment requirements on second home purchases, along with general mortgage rate reductions. Critically, the People’s Bank of China (PBoC) also cut banks’ required reserve ratios, an oft-used tactic that we have seen the central bank employ during the country’s bear markets over the course of our careers.

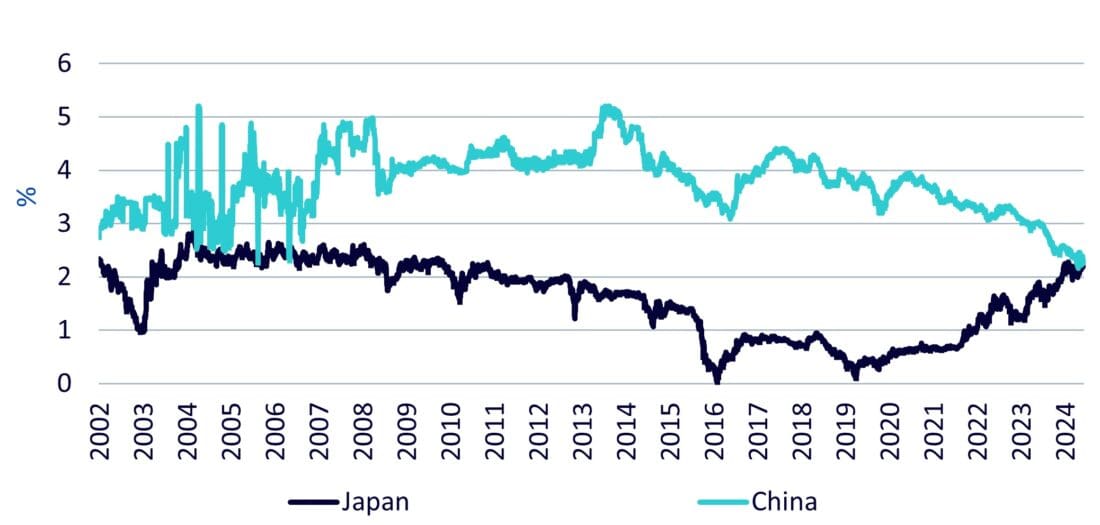

We do not believe the sheer scale of the collapse in the country’s cost of capital is studied enough or fully appreciated in macro circles. As we write, China’s long bond yield has dumped to 2.26% from levels north of 4% during COVID-19. For context, 2.26% is equal to Japan’s 30-year bond quote. This is a new ballgame. With bond yields this low, Chinese equities should get a second look.

Figure 2: 30-year government bond yields

Source: Refinitiv, as of 11/11/2024. Historical performance is not an indication of future performance and any investments may go down in value.

Europe—going soft on soft landing

The European Central Bank (ECB) has taken note of the weak recovery of the euro area. It appears to be rushing towards a neutral rate as concerns about economic growth trump inflation fighting. The ECB’s bank lending survey showed some tentative improvements in the lending environment. Banks did not tighten credit standards for the first time in two years and demand for borrowing is cautiously improving, especially for households. Yet monetary policy can be a weak tool to manage an economy’s business cycle especially one with diverse growth trajectories as the euro area. A weaker euro area could tip the balance towards a slightly softer stance by the ECB, a weaker euro versus the US dollar argues against that. Owing to which the ECB is likely to lower the deposit rate three more times by 25 bps each, in the coming months to reach a trough of 2.5% by March 2025.

The prospect of trade protectionism is also weighing on the outlook for the European economy and Trump’s win is putting that risk into focus.

Trump’s win in the US arguably accelerated the collapse of Germany’s fragile coalition. After Chancellor Olaf Scholz dismissed Finance Minister Lindner, who is also chairman of the liberal Free Democratic Party (FDP), the coalition is in tatters. Snap elections are likely to be called in mid-January, which will probably take place in March. The snap elections can pave the way for a new start in Germany. This should result in a raft of reforms that will strengthen supply and demand with more room for public investment, lowering of business taxes, trimming of welfare and pension benefits alongside a reasonable immigration policy.

Despite the three-party coalition government experiencing tensions over a stagnant economy, Germany’s DAX Index has continued to outperform broader European peers by 9.2% in 2024 . The strong performance can be attributed to specific tailwinds in artificial Intelligence (AI) and cloud computing, beneficiaries from the electrification theme and financials.

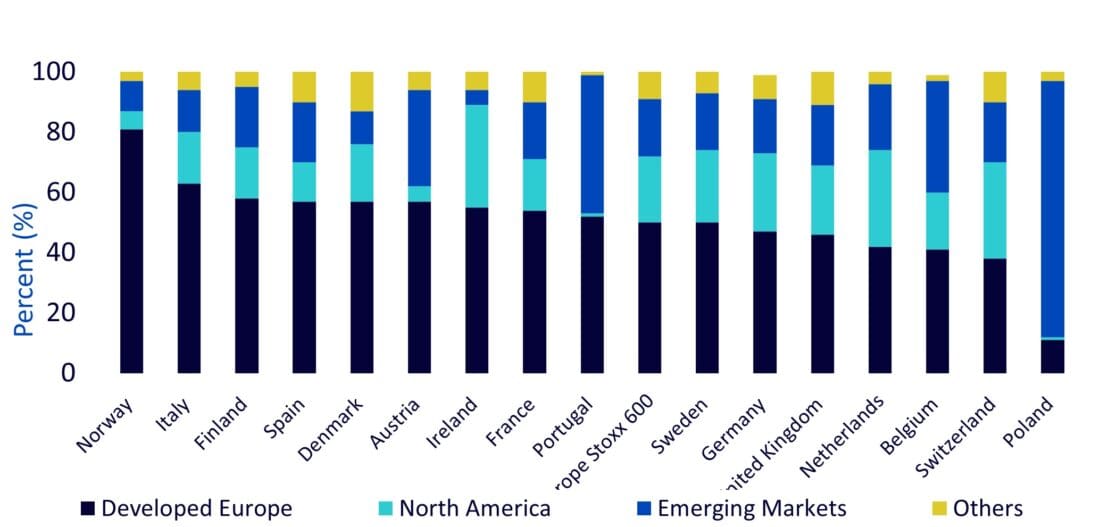

Figure 3: Revenue exposure by country – Eurostoxx 600 Index

Source: Bloomberg, Factset, WisdomTree as of 30 June 2024. Historical performance is not an indication of future performance and any investments may go down in value.

UK budget provides largest loosening in decades

Chancellor Rachel Reeves’ 2024 budget struck a delicate balance between stimulating growth and maintaining fiscal credibility. While expansionary measures initially offered a temporary boost to markets, new borrowing projections triggered a sharp rise in 10-year gilt yields, which reached their highest level in a year of 4.47% . The increase in spending announced in the budget caused the Office for Budget Responsibility (OBR) to double its forecast of annual growth in real government spending over the next two years. By front loading spending while increasing tax revenue gradually, the government will provide a significant boost to growth in 2025 and add to inflationary pressure. However, as National Insurance tax bills rise, companies are likely to feel the pressure, slowing hiring, investment and dampening economic growth. The Bank of England’s (BOE’s) rate path has become more complicated, and we could see it ending its cutting cycle after just three more cuts at 4.25% in Q2 2025.

The new era of central bank gold buying continues

Central banks have become big buyers of gold in recent years. In 2022 and 2023, central banks bought the equivalent of 29% of mined gold in those years. The watershed moment came in 2022 when the Russia-Ukraine war started and G7 countries ‘weaponised’ their currencies which left a bitter taste in many central banks’ mouths. Instead of accumulating these traditional fiat reserve currencies they now look to gold. The lack of viable alternative currencies outside of the G7 favour gold as a pseudo currency that has no central bank controlling its supply or status as legal tender.

Central bank or ‘official sector’ gold buying in 2022 was at a record high and more than double the average between 2012 and 2021 . Central bank purchases in 2023 declined by only a fraction and remained more than double the average between 2012 and 2021. The first half of 2024, saw the largest H1 central bank gold buying on record. Buying in Q3 2024, cooled, but mainly as a result of China not reporting any purchases. It’s debatable whether China has actually stopped buying or is just not reporting its purchases. Outside of China, central bank gold buying is broad and surveys of central banks point to continued strong demand.

The full Global Edge can be found here.

1. Source: Refinitiv, November 2024.

2. Difference in price returns of DAX Index versus EuroStoxx600 Index from 31 December 2023 to 11 November 2024 Bloomberg.

3. Bloomberg as of 31 October 2024.

4. WisdomTree calculations based on World Gold Council data, November 2024.

5. A fiat currency is a government-issued currency that is not backed by a physical commodity, like gold.

6. WisdomTree calculations based on World Gold Council data, November 2024.

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Bonds

As with all investments, your capital is at risk.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account