Originally Posted 2 December 2025 – Global smaller companies: primed to outgrow the giants in 2026

From underdogs to potential frontrunners: Portfolio Manager Nick Sheridan explores why he believes small caps are ready for a resurgence in 2026.

Key takeaways:

- Global small caps are primed for a potential re-rating in 2026 should economic conditions improve, and earnings momentum strengthen.

- AI integration, economic recovery, and M&A activity represent potentially strong tailwinds for small caps, offering strong growth prospects, should these trends continue.

- Geopolitical stabilisation and supportive fiscal policies enhance the prospects for small caps. The environment favours selective positioning and diversified exposure as inefficiencies create opportunities, but demand caution.

Global small caps have struggled to match large caps since 2022, a decline driven by macroeconomic (macro) shocks: surging inflation, aggressive interest rate hikes, geopolitical conflicts, energy market volatility, and prolonged inventory adjustments post-COVID. This has prompted investors to de-risk their portfolios, which has led valuations to move from trading at a premium, relative to large caps, to a meaningful discount today.

However, conditions are reversing. Inflation is at more moderate levels, conflicts are easing, energy prices have stabilised, and central banks are re-setting monetary policy, with more interest rates cuts expected. Destocking of inventories is largely complete, improving supply chain dynamics. As these changes are yet to be reflected in prices for small cap stocks, partly due to relatively anaemic earnings growth –this leaves global small caps primed for a potential re-rating, should economic confidence and earnings momentum strengthen into 2026.

The stage is set for small cap resurgenceEmpty heading

There are several key themes that we expect to shape the prospects for global small caps in 2026:

1) Economic recovery: Small caps are well positioned to benefit from broadening global economic growth. Lower interest rates, improving sentiment and spending initiatives help to support stronger demand.

2) AI integration: While small caps are not going to compete with big tech firms in building the next dominant large language model (LLM), the scale of labour intensity means that adopting AI-driven efficiencies can help smaller companies to deliver significant growth opportunities.

3) M&A acceleration: Lower borrowing costs and growing confidence are favourable conditions for mergers and acquisition (M&A) activity. This is an area where small caps are likely to be a significant beneficiary, both as acquisition/merger targets, and through financials that thrive on increased deal activity.

4) Geopolitical stabilisation: A de-escalation in global conflicts in places like Ukraine opens the door to significant infrastructure and industrial spending to help the rebuilding process – areas where small caps have strong representation. Peace also helps to build confidence, encouraging risk appetite among investors and consumer activity, and improving the prospects for lower energy prices.

Risks and opportunities for global small capsEmpty heading

The current macroeconomic backdrop is something we look at from a glass half full perspective for small cap stocks. On the positive side, we see a supportive US policy backdrop ahead of midterm elections helping to broaden economic growth beyond big-tech AI spending. In Europe, Germany’s fiscal stimulus and debt brake release offer a strong catalyst for recovery, while Southern Europe continues to deliver solid growth. In the UK, a three-year suspension in stamp duty on new stock market listings following a company’s initial public offering (IPO) should hopefully encourage growth and liquidity in the small-cap space. We see these factors as helpful tailwinds in narrowing the valuation gap between small and large caps.

However, risks remain. While AI-related spending is likely to continue, its concentration among mega-cap tech and private giants underscores the challenge for smaller firms to capture meaningful upside. Overall, the environment favours selective positioning and diversified exposure, as inefficiencies create opportunities but demand caution.

Growth potential at a lower priceEmpty heading

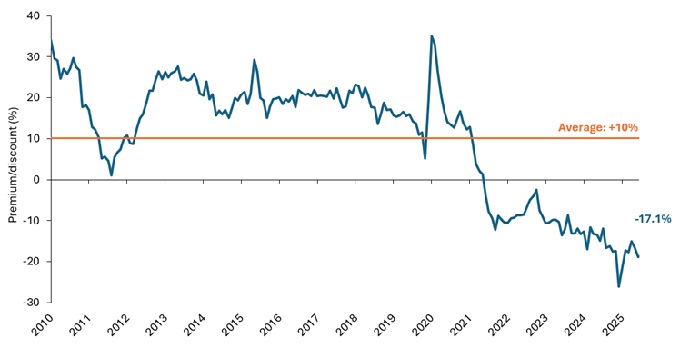

Overall, 2026 looks promising for small caps as macro tailwinds, technological adoption, and strategic activity converge to narrow the valuation gap with large caps (Exhibit 1). We are big believers over the long term that smaller companies can deliver strong operational performance. This is not currently reflected in their valuations. Should conditions align favourably, the smaller cap space could deliver strong growth prospects for investors.

Exhibit 1: Global small cap valuations remain attractive relative to large caps

Source: Bloomberg, Janus Henderson Investors Analysis, at 12 November 2025.

Indices used: MSCI World Small Cap, MSCI World. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns.

Disclosure: Janus Henderson

The opinions and views expressed are as of the date published and are subject to change without notice. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes and are not an indication of trading intent. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Janus Henderson and is being posted with its permission. The views expressed in this material are solely those of the author and/or Janus Henderson and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account