Originally Posted 28 November 2025 – What’s Hot: A fragile peace plan, a firm defence cycle

Key Takeaways

- The 28-point “Miami draft” is morphing into a 19-point framework, but core issues on territory and security guarantees remain unresolved and the war continues unabated.

- Whether or not a deal is signed, Europe’s defence budgets, procurement policies and industrial strategy point to a structurally higher, decade-long defence cycle.

- Rising backlog-to-sales ratios and accelerating revenues across the WisdomTree Europe Defence UCITS Index constituents underpin the investment case for WDEF as a targeted way to express this theme.

A ceasefire in Ukraine should be the moment markets breathe a sigh of relief. Instead, the way the latest peace blueprint is evolving risks more uncertainty for Ukraine’s security. Crucially, whether we end up with a deal or not, the rebuild of Europe’s defence industrial base is a decade long project. The Q3 results and expanding order backlogs provide further evidence of this multi-year investment cycle.

From a 28-point “wish-list” to a 19-point framework

US officials are pushing Ukraine to accept a 28-point plan reportedly drafted by the US special enjoy Steve Witkoff with heavy Russian input – a document that, in places, has read more like a Kremlin wish list than a balanced settlement.

Among the most contentious ideas in that original framework:

- Ukraine surrendering not only occupied territory but also parts of Donetsk it still controls

- A constitutional ban on NATO membership

- A hard cap on Ukraine’s armed forces in peacetime

The plan looks to be evolving. Negotiators are working from the original 28-point plan towards a slimmer framework 19-point framework with a higher ceiling on Ukraine’s peacetime forces (around 800k rather than the original 600k) and some softening of the most maximalist demands.

The latest sequence of events underlies how fluid and fragile the process remains. Over the weekend 22-23 November 2025, senior US and Ukrainian officials met in Geneva to work through the terms. President Zelenskyy described the plan as “potentially workable” but stressed that key points on territory and security guarantees remain unresolved.

Moscow Keeps its Options open

Moscow, for its part, is keeping its options open. Kremlin advisor Yuri Ushakov has confirmed that Witkoff is due in Moscow next week, even as he insists Russia has not officially received the US proposal and that there has been no detailed point by point negotiating roundtable yet. Russian officials say they have seen the text via back channels and regard parts of it as acceptable, but they are still ruling out major concessions on territory or long-term force posture.

On the ground, the war has not paused for diplomacy. Russia continues to launch drone and missile attacks against Ukrainian cities and infrastructure, while Ukraine strikes back at targets supporting the Russian war machine, including facilities linked to missile production. The recent intensification of aerial bombardment underscores that neither side is acting as if a ceasefire is imminent.

No major “peace dividend”, even if deal happens

There are two uncomfortable possibilities here:

1. A lopsided deal goes through. Ukraine is pushed into a half-surrender that leaves large territories under Russian control and its future security arrangements remain ambiguous.

2. No deal is signed. The war continues, perhaps at a lower tempo or along a frozen line, while Russia rebuilds and probes elsewhere.

In both cases, the implications for European defence spending are broadly the same. Trust in Russia is permanently broken. Even a paper peace deal is unlikely to trigger a renewed wave of European energy imports or foreign direct investment into Russia. Few governments want to rebuild the revenue stream that funds Putin’s war machine.

Europe cannot rely on US policy stability. Trump’s oscillation since returning to the White House has hammered home that Europe needs a larger autonomous defence base, regardless of which way Washington leans.

Multi-year European commitments now envisage total defence envelopes of 5% of GDP with roughly 3.5% earmarked for core defence spending. Current procurement growth assumptions in the sector are built around European defence budgets rising towards these levels by the mid-2030s. So even in a best-case ceasefire scenario, the classic “peace-dividend” is not the base case for Europe this time.

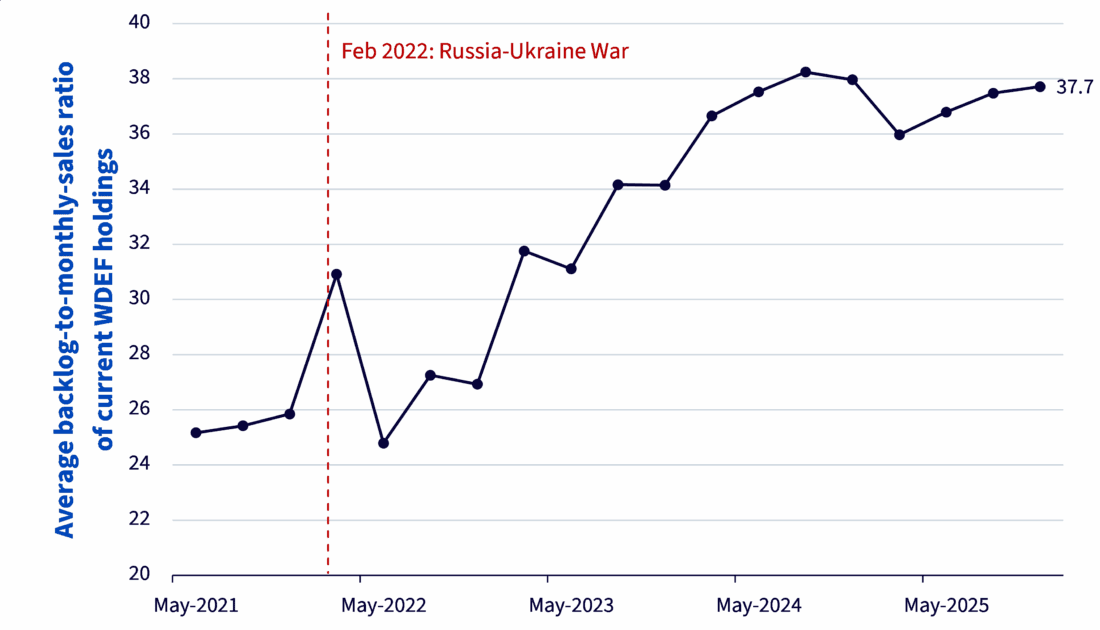

Q3 earnings season: Backlogs tell a very different story

Markets trade narrative, companies trade orders. The WisdomTree Europe Defence UCITS Index’s (Ticker: WTEUDEFN Index) simple average ratio of backlog to monthly sales climbed to 37.7x in November, from around 25x before Russia-Ukraine War. More importantly the average ratio of backlog to monthly sales has crossed the 59.9x mark, for the five largest holdings of WTEUDEFN as of 21 November 2025. European defence companies such as Rheinmetall, BAE systems and Thales are consistently booking more than they are shipping. Kongsberg’s defence business has been delivering a higher backlog to monthly sales ratio. Q3 earnings season confirms that backlogs continue to expand in a world where NATO stockpiles are being replenished and capacity expanded.

Figure 1: Average backlog-to-monthly-sales ratio of holdings in the WisdomTree Europe Defence UCITS Index

Source: WisdomTree, Bloomberg. For each holding, backlog to monthly sales ratio calculated as Order Backlog Value / (Trailing 12M Net Sales/12). Data as of 21 November 2025. All holdings in the WisdomTree Europe Defence UCITS Index with available data are included in the calculation. You cannot invest directly in an index. Past performance is not an indicative of future Results and any investments may go down in value.

Revenues are already inflecting. The 12-month weighted average defence revenues across the European peer group represented in the WisdomTree Europe Defence UCITS Index (Ticker: WTEUDEFN Index) are trending steadily higher since early 2024, with Rheinmetall again showing the steepest slope as ammunition and land-systems demand gains momentum.

Figure 2: Weighted average year-over-year sales growth of the WisdomTree Europe Defence UCITS Index

Source: WisdomTree, Bloomberg. Year-over-year sales based on the latest twelve months (LTM) vs prior LTM as of 21 November 2025. Holding weights are fixed as of 21 November 2025. All holdings in the WisdomTree Europe Defence UCITS Index with available data are included in the calculation. You cannot invest directly in an index. Past performance is not an indicative of future Results and any investments may go down in value.

Pulling it together, the case for staying constructive on European defence does not depend on whether we end up with a 19-point deal, a reworked framework or no agreement at all.

- Security architecture has structurally shifted. A continent that has seen full-scale conventional war on its borders is unlikely to go back to 2% of GDP defence spending. The new floor is much higher. The political floor for budgets is now structurally higher.

- Industrial policy is lining up behind the sector. EU initiatives to lift the share of intra -European procurement from 35% pre-Ukraine to 50% by 2030 and 60% by 2035 directly support local primes and subsystem suppliers.

- Order books are turning policy into cashflows. Q3 earnings season delivered higher order backlogs, rising revenue run rates and longer visibility that continue to show backlogs building, locking in a multi-year delivery pipeline that will take the rest of the decade to work through.

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Alternative Investments

Alternative investments can be highly illiquid, are speculative and may not be suitable for all investors. Investing in Alternative investments is only intended for experienced and sophisticated investors who have a high risk tolerance. Investors should carefully review and consider potential risks before investing. Significant risks may include but are not limited to the loss of all or a portion of an investment due to leverage; lack of liquidity; volatility of returns; restrictions on transferring of interests in a fund; lower diversification; complex tax structures; reduced regulation and higher fees.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account