It’s here! After weeks of discussion about the likelihood and magnitude of a rate cut at today’s FOMC meeting, the day is upon us. It is difficult to expect anything other than a 25-basis point cut, even though the market is assigning a slight probability to a larger one. Instead, as we discussed at length yesterday, there is likely to be more drama surrounding the “dot plot”, dissents, and of course, Chair Powell’s discussion afterwards. Do options traders seem at all concerned?

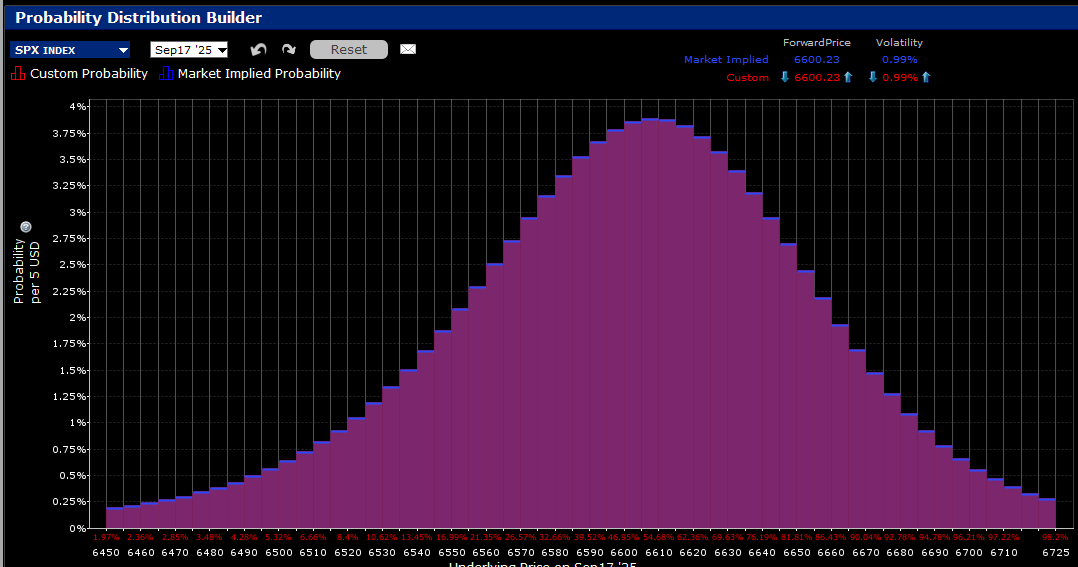

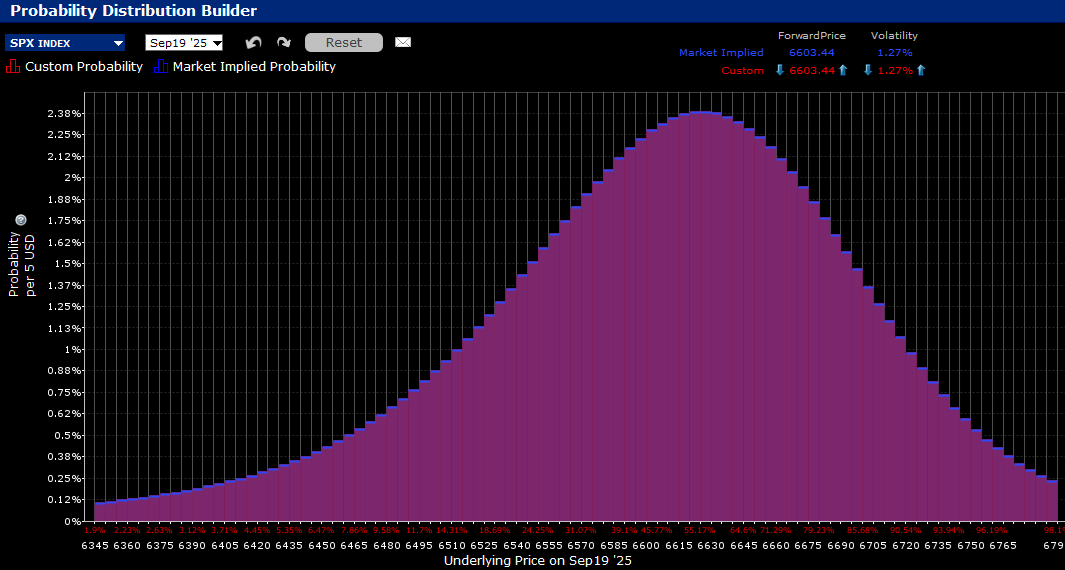

The short answer to that question seems to be, “not really.” For starters, we see the market assigning peak probabilities for S&P 500 (SPX) closes today and Friday above the current level of 6600. This has become typical during the past few months. Heck, if we seem to go up every day, why shouldn’t options probabilities reflect that? Thus, the IBKR Probability Labs shows peak outcomes of 6605-6615 for today and 6620-6625 for Friday.

IBKR Probability Lab for SPX Options Expiring September 17, 2025

Past performance is not indicative of future results. Source: Interactive Brokers

IBKR Probability Lab for SPX Options Expiring September 19, 2025

Past performance is not indicative of future results. Source: Interactive Brokers

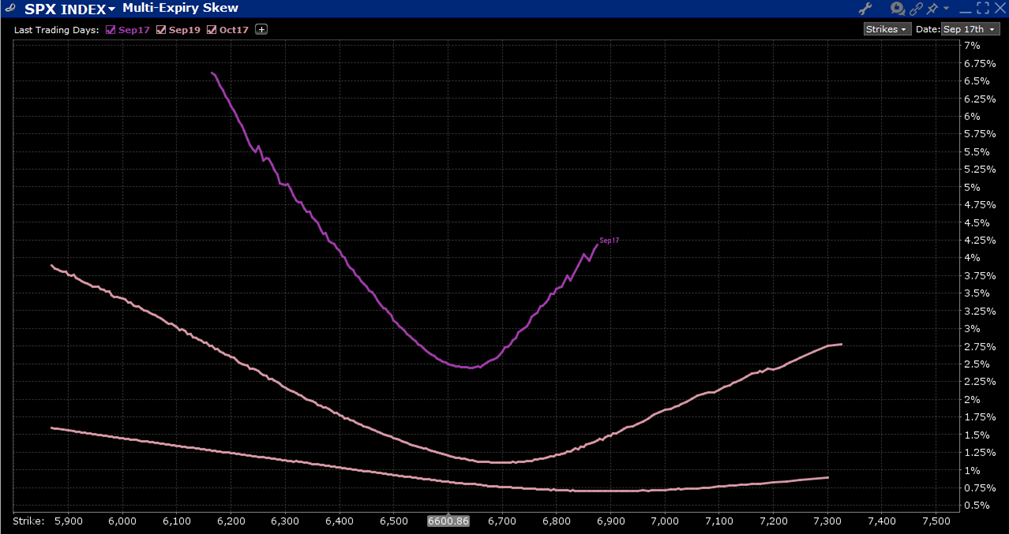

Even though the market is biased to expect an up move, there is nonetheless a fair amount of volatility priced into near-term options. We see a steep skew with a downside bias in options expiring today and something similar, though with less magnitude, for options expiring Friday. At-money options for today are implying a 2.5% intraday move, while those expiring Friday imply 1.2% daily moves between now and the end of the week. These compare with a 0.8% daily volatility priced into monthly options expiring in October.

Skews for SPX Options Expiring September 17th (top), September 19th (middle), October 17th, 2025 (bottom)

Past performance is not indicative of future results.

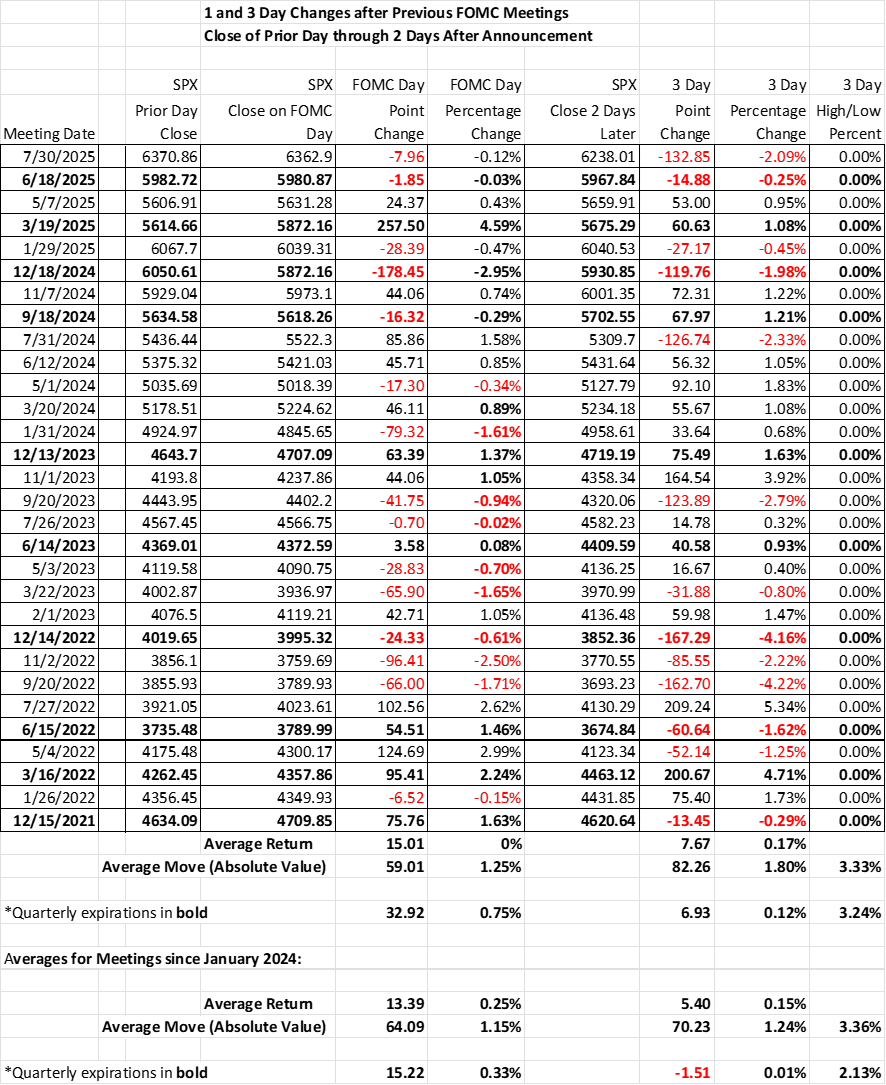

Using recent history as a guide, it appears as though options expiring today have relatively high implied volatilities, but relatively low for the three-day period that follows the meeting. The table below shows the 1- and 3-day moves that followed FOMC meetings since December 2021. Bearing in mind that volatility recognizes moves in either direction, we see that the average move on FOMC day is 1.25% over that period. That of course is well below the 2.5% priced into today’s expiration. However, we see an average move of 1.8% on a directional basis and a 3.33% move on a high/low basis. over the rest of the week – well above the 1.2% priced into Friday’s expiration.

We broke out the corresponding values for weeks when the FOMC decision coincided with a quarterly expiration – as is the case this week – and saw little difference between those averages and the broader averages. Interestingly, the average of directional moves on FOMC day is basically zero. It’s been roughly a coin flip as to whether the post-Fed move is up or down.

Past performance is not indicative of future results. Source: Interactive Brokers

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Options (with multiple legs)

Options involve risk and are not suitable for all investors. For information on the uses and risks of options read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD). Multiple leg strategies, including spreads, will incur multiple transaction costs.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account