Client Portal – Trading and Advanced Functions (Cantonese)")

At a Glance

- A weakening U.S. dollar could result in decreased American demand for European goods

- From January to June, the euro experienced a 15% increase against the dollar, climbing from 102 to 117

The euro’s notable appreciation against the U.S. dollar since the start of 2025 – jumping from 102 in early January to 117 by late June, an almost 15% gain – signals more than typical currency market shifts. This upward movement reflects growing market worries about the U.S. fiscal situation and a reduction in long U.S. dollar positions. Moody’s recent credit rating downgrade, a looming debt ceiling deadline and a weak 20-year auction on May 21 have further underscored these issues. What risk factors result for Europe from the recent surge in the Euro?

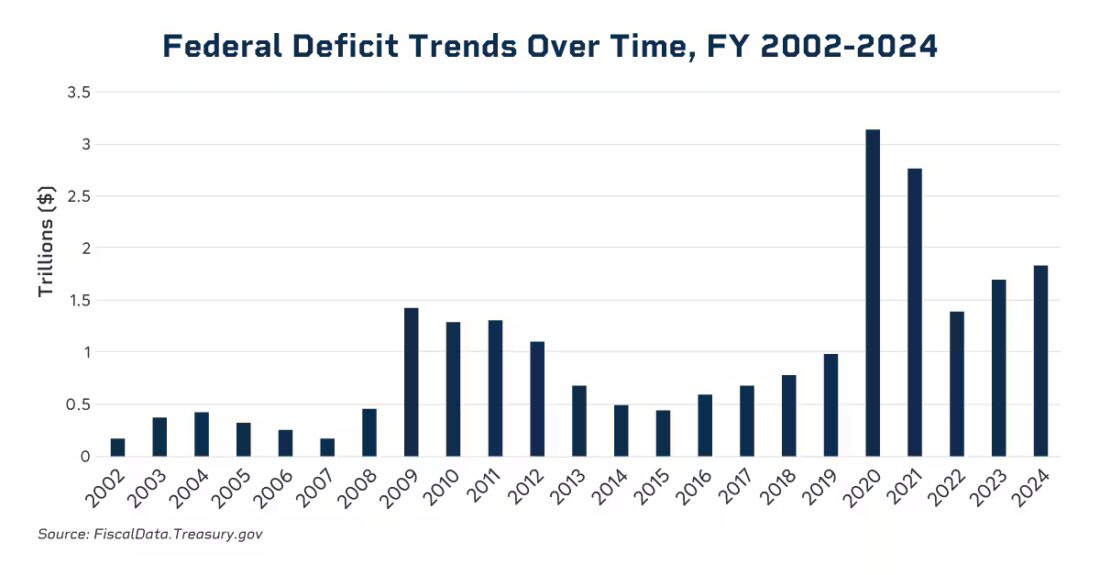

Current U.S. Fiscal Landscape

The U.S. federal deficit has more than doubled from $980 billion in 2019 to nearly $1.9 trillion in 2024 and is projected to remain at this level in 2025, with some forecasts suggesting it could reach $2.75 trillion. With the national debt at $36.2 trillion (124% of GDP), there are growing concerns about a potential “debt spiral” fueled by rising debt service costs and yields, potentially leading to increased borrowing at higher rates. Though an immediate bond market crisis is unlikely, the risk is growing.

The lack of progress on reducing the deficit, combined with the possibility of additional spending, deepens concerns about the long-term financial stability of the U.S. This situation risks weakening the dollar and exacerbating global market anxieties. Past performance is not indicative of future results.

How Does U.S. Fiscal Stability Impact Europe?

1. Appreciation of the Euro

A persistently strong euro could make European products too expensive for the U.S. market, which could be a problem as the U.S. is one of Europe’s biggest customers. The U.S. also runs a $200 billion trade deficit with the eurozone for goods. A weakening U.S. dollar could result in decreased American demand for European goods such as German automobiles, French wines and Italian machinery. This decline in demand could significantly impact eurozone exporters, particularly smaller businesses that are already facing heightened global competition. This could lead to reduced export earnings, job cuts and slower economic expansion in the eurozone, particularly for countries reliant on U.S. trade.

2. Escalating Borrowing Costs

Global financial markets are tightly linked, with the 10-year bond yields of both the U.S. and Germany generally moving in parallel. The recent surge in U.S. yields in May was mirrored by a rise in German rates, which serve as the European benchmark. Increased borrowing costs across the eurozone could impede investment, hinder business growth and restrain economic progress. This could pose a significant economic headwind to the region.

The one piece of good news is that inflation in the eurozone has already moved below the European Central Bank’s 2% target. Although this is a relief considering the stagflation potential of persistent elevated energy costs, it has some analysts believing that it could be a sign that the economy is already slowing.

While the potential impacts of rising debt are still to be determined, it is likely that if the U.S. keeps piling on debt the fallout could ripple through Europe’s markets, from trade balances to bond yields. Add in the uncertainty of tariffs and a potential global slowdown, and it’s not a big surprise that the euro has displayed buoyancy.

—

Originally Posted on July 8, 2025 – How Rising U.S. Debt Impacts European Markets

Disclosure: CME Group

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Bonds

As with all investments, your capital is at risk.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. For information on the uses and risks of options read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD). Multiple leg strategies, including spreads, will incur multiple transaction costs.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account