Originally posted, 3 July 2025 – How equity factors dampened the April tariff tantrum

- Reduced Drawdowns: The Russell 1000 Comprehensive Factor Index cut peak drawdown by 29% versus the benchmark during April’s tariff volatility.

- Superior Risk Efficiency: Multifactor allocation reduced peak volatility by 13.8 percentage points, outperforming both equal-weighted and market-cap weighted strategies.

- Factor-Driven Stock Selection: Companies with strong factor scores like BJ’s Wholesale were significantly overweighted, while poor scorers like Tesla and Boeing were excluded or underweighted.

In a year of equity market volatility, factors have provided an oasis of relative stability. After a secular rise in equity prices in 2023 and 2024, extended valuations and high concentration laid the groundwork for factors to stabilise market excesses. The results thus far in 2025 have been attenuated downdraws without sacrifice of long-term growth potential.

The Russell 1000 Comprehensive Factor Index operates with an even tilt to each of the “big five” factors (Quality, Value, Momentum, Low Volatility and (small) Size). In this insight, we show how targeting these independent drivers of return reduced total drawdown by 29% versus the benchmark. We also give three examples of how a multifactor approach informs index constituent weightings.

Factors rethink vol exposure

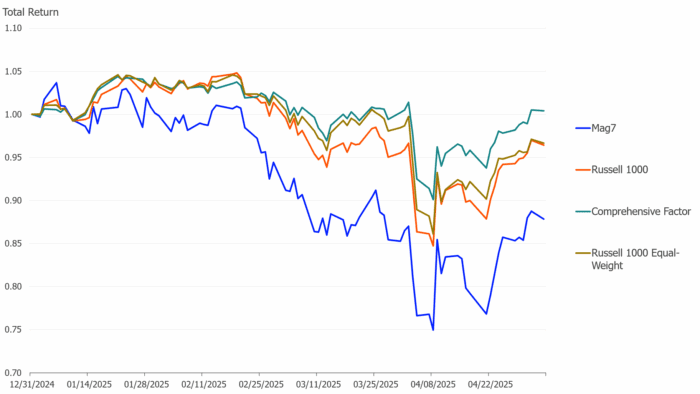

Raw performance lends an excellent case study for how factors can diversify equity returns away from an index with a concentrated “Magnificent 7” risk profile. Whereas the Russell 1000 Index has experienced a peak drawdown of 19.15% so far this year, the Russell 1000 Comprehensive Factor Index dampened the blow to a pullback of only 13.70%. The peak outperformance of the factor index was achieved on April 4th at a walloping 614 basis points, a large contributor to which was the downweighting of the Mag 7 names by 29 points at the start of 2025.

Factor Outperformance 2025

In the context of risk efficiency, the factor-driven narrative becomes even more compelling. The figure below depicts the rolling 15-day annualized risk thus far in 2025 for the Comprehensive Factor Index and other mainline equity exposures in the large cap ecosystem. It’s striking that the factor index was both the best-performing and least volatile of the indices highlighted, downgrading what was a period of extreme distress for many investors to mere discomfort.

Rolling 15-Day Volatilities

Measured by 15-day rolling historic volatility, the Comprehensive Factor Index reduced peak risk by 13.8 percentage points versus the Russell 1000 benchmark. Moreover, allocating equally to factors achieved 3.5 times the volatility reduction when compared with allocating equally to stocks, In other words, factors can offer a more informed way to diversify equity risk than equal-weighted strategies. Indeed, so effective were factors at softening the April 2025 tariff shock that peak volatility for the factor index was only marginally higher than the average volatility for Mag 7 names (45.3% versus 42.1%–see the bar chart below).

2025 Volatility Comparison by Index

Method to the (lack of) madness

Performance characteristics aside, how does a multifactor strategy determine its stock selection? The Russell 1000 Comprehensive Factor Index looks for companies that exhibit all five factor exposures simultaneously, identifying them as key model overweights for a semi-annual rebalance.

The key advantage of this approach is that instead of making bets in five different directions—which tend to wash out and self-neutralise—the model finds instances where these factors are already in alignment. In effect, the percentile rank of exposure to each of the five factors is a direct multiplier to market cap weighting. Companies with higher scores receive a higher multiplier, while companies with lower scores see reduced allocations.

To break through the abstraction, three examples bring the operation of this Index to life. First we show why a well-known Magnificent 7 company (Tesla) was eliminated from the factor index; second, we explain why a consumer staples company (BJ’s Wholesale Club) received one of the model’s highest overweights; and third, we show why aerospace giant Boeing was nearly excluded due to its poor factor scores.

- Tesla Motors (TSLA): Though it’s a high-profile stock, the leading electric automotive manufacturer is a prime instance of a Mag 7 company that was eliminated from the multifactor portfolio because of its low compound factor score: Tesla is the 17th worst scoring company in the entire Russell 1000 benchmark. This is primarily due to the company’s Low Volatility and Size factor scores (which are in the bottom 2nd and 1st percentiles, respectively). However, with Tesla’s stock price down 30.1% year-to-date (as at the end of April), the company’s Momentum and Value scores (which are in the bottom quartile and quintile, respectively) had an additional negative impact on its ranking.

- BJ’s Wholesale Club (BJ): At around $15 billion in market capitalisation, this consumer staples company is overweighted 18 times by the Comprehensive Factor methodology. As the 13th highest scoring company overall, it achieves an 82nd percentile rank in Quality and 77th percentile rank in Value. Driven by consumers looking to extend their purchasing power, the stock is up 31.6% year-to-date (at the end of April) and its Momentum score also lies half a standard deviation above the mean.

- Boeing (BA): The embattled aerospace giant sees its benchmark weight reduced by 99% in the multifactor model after it was ranked in the bottom 4% overall. Boeing’s highest factor exposure is a 35th percentile score for Quality, but it performs worse on other factors, reducing its overall score. For instance, the company scores half a standard deviation below the mean in Value, 0.9 standard deviations below the mean on Volatility and it is in the bottom 2% for Momentum. Combined, these metrics are an example of a multi-factor index removing a company with poor exposure to the fundamental drivers of return.

Systematic, data driven

These case example companies help vivify what high and low factor scoring companies look like during a period of elevated market stress. By taking a systematic approach to these historical drivers of excess return, the Comprehensive Factor Index delivered marked improvements to performance and risk efficiency.

[1] Determined by Z-Score and configured to percentile rank by the gaussian error function.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from LSEG and is being posted with its permission. The views expressed in this material are solely those of the author and/or LSEG and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. For information on the uses and risks of options read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD). Multiple leg strategies, including spreads, will incur multiple transaction costs.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account