Client Portal – Trading and Advanced Functions (Cantonese)")

This trading week in the US is short but potentially consequential. This year, Independence Day (July 4th) falls on a Friday, and furthermore, US stock exchanges close at 1PM EDT tomorrow ahead of the three-day weekend. But there are some consequential numbers to be digested before those of us who are not already on vacation scoot away for the holiday. The June Employment report arrives tomorrow at 8:30 EDT.

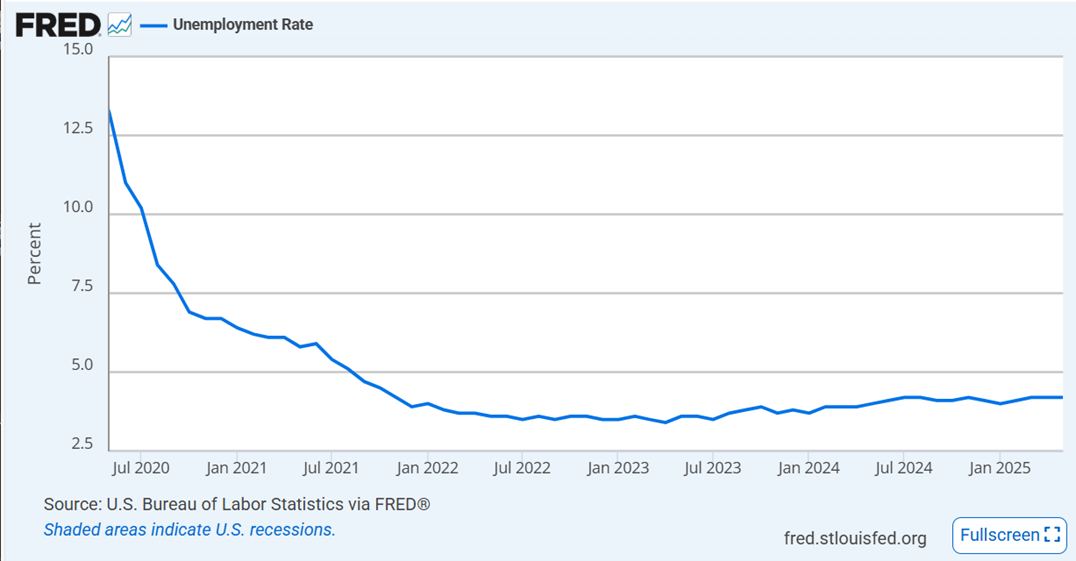

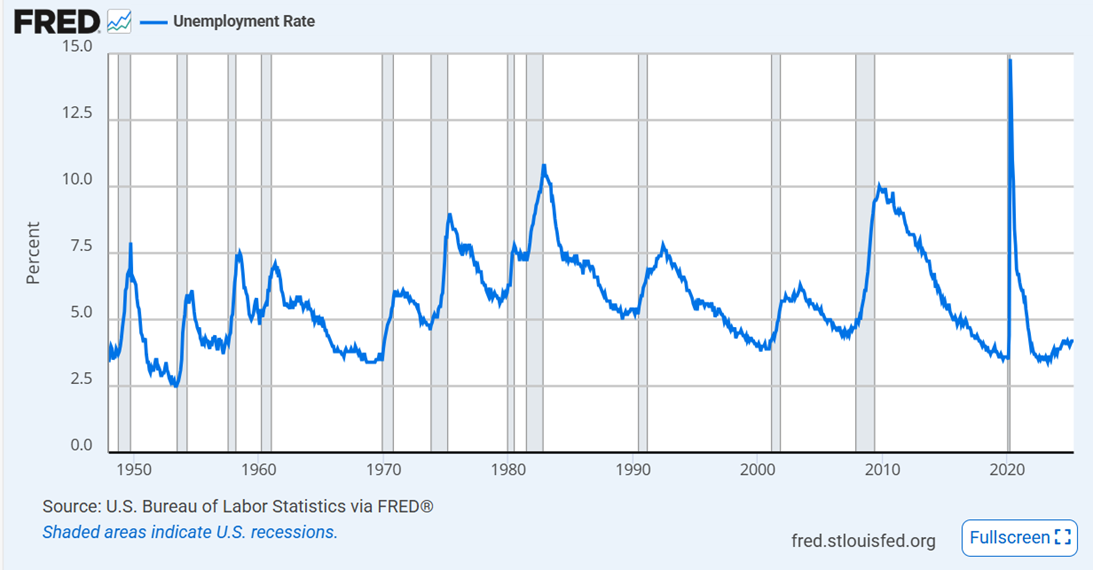

Although the market climate clearly is rather sanguine right now, some investors are at least feigning concern about the condition of the labor economy. Remember, maximum sustainable employment – along with price stability – is half of the Federal Reserve’s dual mandate. The Unemployment Rate has been gently rising over the past several months (as shown by the first chart below), but it remains nearer to historic lows than highs (as shown by the second chart):

Seasonally Adjusted Unemployment Rate, 5-Years, Monthly Data

Source: Unemployment Rate (UNRATE) | FRED | St. Louis Fed

Past performance is not indicative of future results

Seasonally Adjusted Unemployment Rate, Monthly Data Since January 1948

Source: Unemployment Rate (UNRATE) | FRED | St. Louis Fed

Past performance is not indicative of future results

The combination of modestly higher unemployment yet at a historically low level must offer some difficulty for the FOMC. When must they consider that we have moved far enough away from their goal before they need to adjust monetary policy?

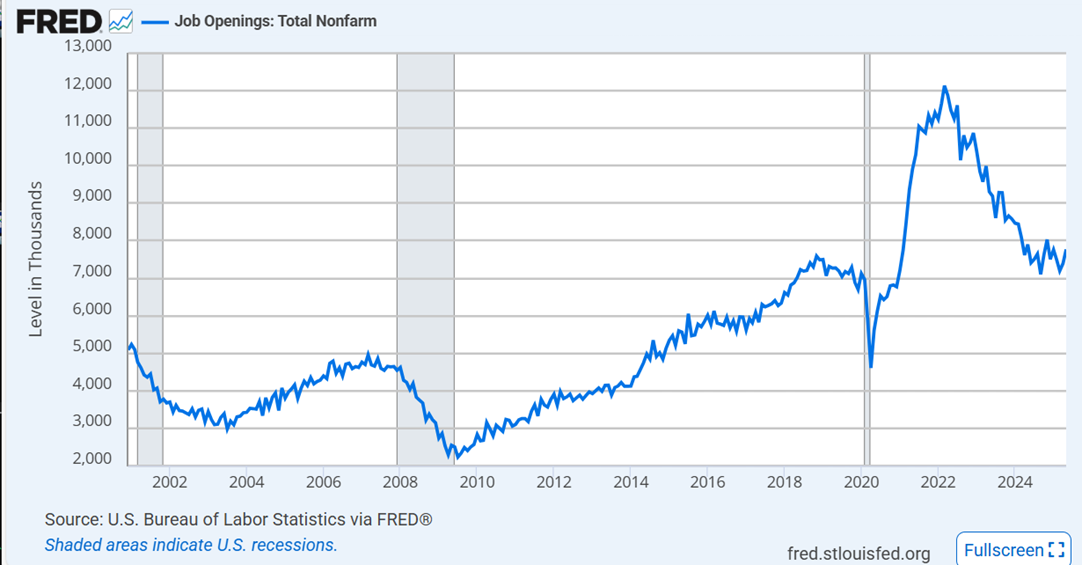

Over the past two days, we have received somewhat conflicting reports about labor. Yesterday, we learned that JOLTS job openings unexpectedly rose to 7.769 million, well ahead of the 7.3 million consensus estimate and last month’s revised 7.395 million. A longer term chart shows that the decline from the post-Covid peak in openings seems to have taken a modest pause, albeit above levels that prevailed prior to the pandemic:

JOLTS Jobs Openings, Monthly Data Since December 2000

Source: Job Openings: Total Nonfarm (JTSJOL) | FRED | St. Louis Fed

Past performance is not indicative of future results

This morning, however, the ADP Employment Change for June was a bit of a shock. It showed a decline of -33,000, far below the 98k gain that was expected and last month’s adjusted +29k. We saw futures dip briefly, though stocks recovered after a combination of Tesla’s (TSLA) worse-than-expected sales report (no, that is not typo – the stock rallied +4%) and reports of a trade deal with Vietnam. A big decline on ADP was never really in the cards anyway – the market understands that it is at best an imperfect harbinger of the Nonfarm Payrolls data – though that was the first monthly decline since March 2023’s -53k reading.

In theory, we might expect some market concern ahead of a number that could have a major influence on monetary policy. In practice, not really.

Consensus expectations are for an Unemployment Rate of 4.3%, up from last month’s 4.2%.

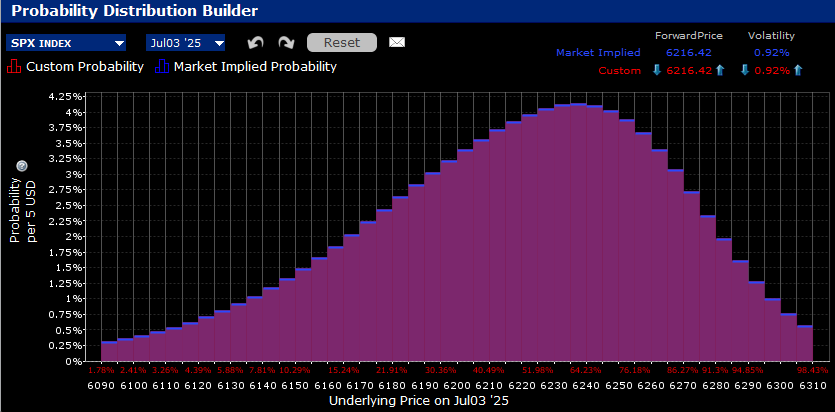

Perhaps the solid consensus is what is leading options expiring tomorrow on the S&P 500 (SPX) to show a pronounced upward bias. (Heck, that’s what we’ve seen for weeks, so why stop now?) The IBKR Probability Lab shows a peak outcome of 6235-6240, above the current 6217 level:

IBKR Probability Lab for SPX Options Expiring July 3rd, 2025

Source: Interactive Brokers

Past performance is not indicative of future results

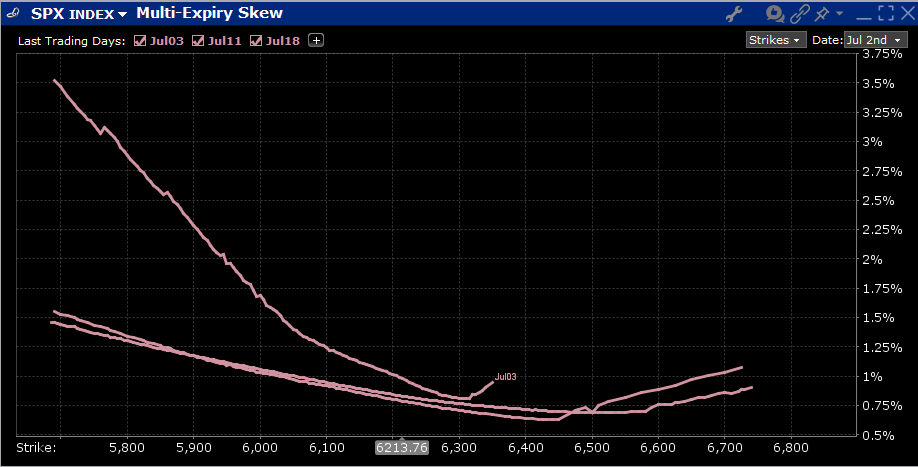

That said, there is indeed a pronounced downside skew for SPX options expiring tomorrow, something that is quite modest for options expiring next week and the week thereafter:

Skews for SPX Options Expiring July 3rd (top), July 11th (middle), July 18th (bottom)

Source: Interactive Brokers

Past performance is not indicative of future results

Finally, we’d like to take a look at the Cboe Volatility Index (VIX) and it’s 9-day counterpart VIX9D. Neither is showing much concern either about events in the near-term, such as the Employment Report, the expiration of the tariff moratoria, or the mid-month arrival of earnings season. It is likely that VIX9D is somewhat depressed by the fact that we are “missing” one-and-a-half trading days during its calculation, but it nonetheless shows a general lack of demand for hedging protection. We’ll know tomorrow if that proved appropriate.

6-Months, VIX9D (red/green daily candles), VIX (blue line)

Source: Interactive Brokers

Past performance is not indicative of future results

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. For information on the uses and risks of options read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD). Multiple leg strategies, including spreads, will incur multiple transaction costs.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account