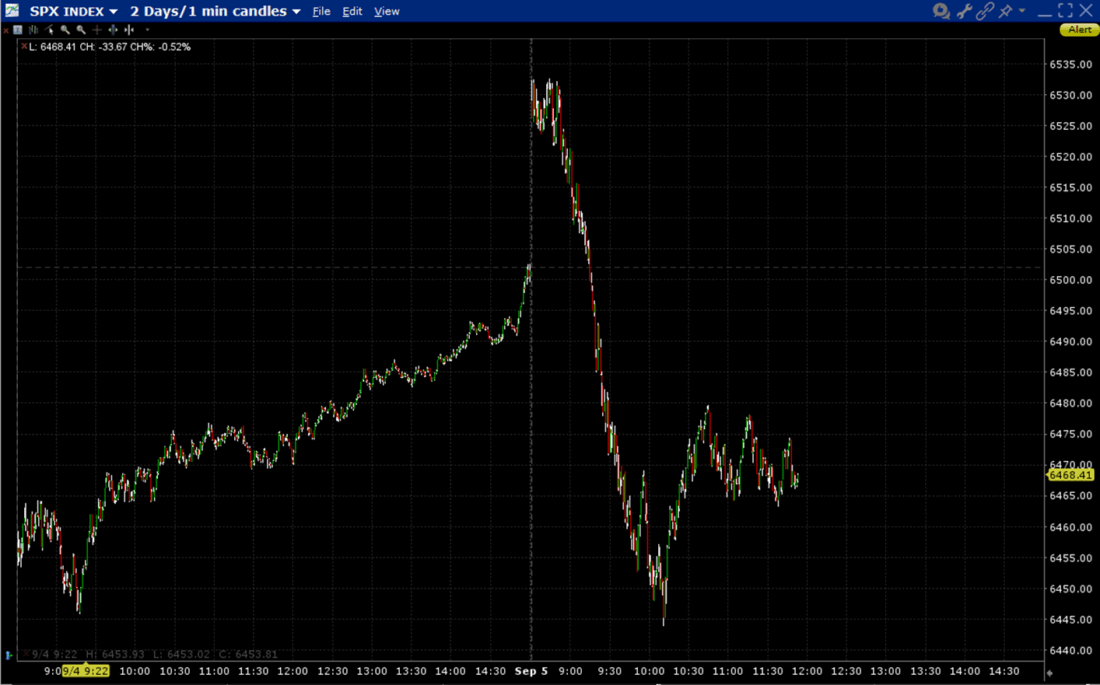

Things turned around rather quickly this morning. I was shuttling between appointments in NYC, and sometime between entering the subway at Wall Street and emerging without delay uptown, major stock indices had staged an abrupt reversal. What changed the mood so quickly?

I have been operating under this premise: the market’s mindset is so relentlessly positive that investors will pick whatever narrative fits their desired outcome of higher prices unless the data makes that impossible. As I put it to someone this morning:

Given the market’s current mentality, all news is good news.

Weaker jobs -> lower rates -> good for stocks

Stronger jobs -> better economy -> good for stocks

I happened to be on live TV when the news broke, and my immediate interpretation was that the report was disappointing, but not distressingly so. My initial premise was that we came into today with a “heads I win, tails I win” attitude, with a weak number reinforcing the likelihood of rate cuts and a strong one allowing investors to focus on a strong economy. Yet I also echoed the concluding paragraph of yesterday’s piece:

Many investors are clearly hoping for rate cuts, but it is important to remember to be careful what we wish for. Data that show a gently decelerating but not dire labor market would suit that goal. Plunging data might bias the Fed to further cuts, but could also raise concerns that the central bank is too far behind the curve. The former extends the “Goldilocks” narrative; the latter raises concerns about stagnation or stagflation. Equity investors should always opt for a better economy.

On first blush, the data seemed “Goldilocks” enough that while there were signs of additional decay under the surface, specifically in some of the specific subsets of employment and in the fact that June was now revised to a monthly loss of jobs, they weren’t initially considered sufficient to create the type of economic concerns that would shift the market’s ebullient mood. Perhaps that reflects one of our ongoing mantras:

Traders react; investors consider

Thus, upon closer consideration, those additional concerns might indeed be sufficient “to create the type of economic concerns that would shift the market’s ebullient mood.” Or perhaps, yesterday’s rally, which seemed to have no apparent cause, was pricing in a favorable result from the jobs report. In other words, this could simply be “buy the rumor, sell the news”.

Another cause of the reversal could be more industry-specific — the gravitational pull of Nvidia (NVDA). The early focus was on Broadcom’s (AVGO) rally on good earnings and a big OpenAI contract, which led to a double-digit percentage rally. But AVGO’s win is somewhat at the expense of the larger NVDA. With NVDA heading lower, and seemingly dragging down MSFT and a few others, we lost that leg of the tech rally.

Thus, around midday EDT we find ourselves with key index benchmarks trading flattish to modestly lower (SPX and INDU ~-0.5%, NDX ~-.25%, RTY +.1%), with SPX bouncing dutifully off yesterday’s lows. Bond yields reflect an increased likelihood for additional rate cuts. The short end of the curve is sharply lower (2-year Treasuries -11 basis points), with the longer end following more or less in a parallel manner (10-year -9bp, 30-year -7.5bp). CME futures went from pricing in a roughly 100% chance of a 25bp cut just before the jobs report to adding a 10% chance for a 50bp cut instead. Just under 3 full cuts for 2025 are also now priced in. Traders on ForecastEx show a similar likelihood for a 50bp cut but are a bit more skeptical overall with only an 88% “Yes” for a 25bp cut in September.

For the rest of the afternoon, I will be keeping a close eye on yesterday’s lows. As noted above, SPX bounced off yesterday’s low (actually, it bounced from a hair below, but it was close enough). A close below that level would constitute an “outside reversal”. That is a very significant pattern for technical analysts, and even non-believers should recognize the psychological about-face that requires taking a stock or a market from fresh highs to prior lows.

On the flip side, never underestimate traders’ ability to ratchet the market higher on Fridays. As we have frequently noted, on most days we have daily expirations (0DTE) in key index and ETF options, but on Fridays, thanks to expiring weekly options, we have “0DTE” in over 600 key stocks and other ETFs as well. As long as MOMO and FOMO (momentum and fear of missing out) remain key motivations, a minor bounce can easily become a full-fledged rally for little apparent reason. Let’s see which way the mood swings later today.

SPX, 2-Days, 1-Minute Candles

Source: Interactive Brokers

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionDisclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account