Stocks cautiously extended their recovery yesterday as a slew of weaker-than-expected economic data prints weigh on Treasury yields, serving to dial up slowdown risks while offering breathing room on valuations. The top disappointer happened to be consumer confidence, whose headline result dropped to a 4-year low and the expectations subindex plunged to its weakest level in 12 years. Households reported mounting anxiety related to price pressures, job security, tariff uncertainty, high borrowing costs and market volatility. Meanwhile, transactions for new homes barely recovered last month, despite a significant drop in mortgage rates. Furthermore, looser financial conditions failed to propel manufacturing activity in the Fed’s Richmond District as elevated charges hampered purchasing volumes.

Consumer Confidence Hits 49-Month Low

Folks feel the worst about their personal economic conditions in 49 months as households manage a plethora of headwinds and uncertainties. The Conference Board’s Consumer Confidence Index fell for the fourth consecutive month to 92.9 in March, beneath the median estimate of 94 and February’s 100.1. The expectations component was the greatest drag, falling to 65.2 from 74.8, the lowest in 12 years and well below the 80-point level that the organization considers a leading indicator of recession. The gauge for present situations offered a much more modest decline, softening to 134.5 from 138.1. Broad-based weakness existed within the report, but price pressures, job security, tariff uncertainty, elevated borrowing costs and stock market volatility were referenced as top issues.

Past performance is not indicative of future results

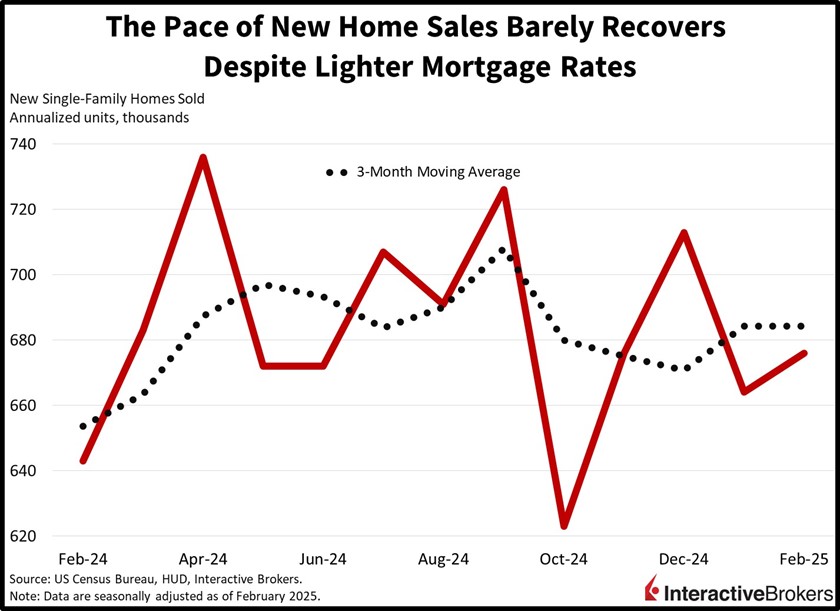

Real Estate Closings Disappoint

A sharp drop in mortgage rates did little to motivate closings of new homes last month, with transactions barely recovering. The 676,000 seasonally adjusted annualized units (SAAU) reported in February came in slightly below the projected 680,000 but above January’s pace of 664,000. Overall, the month-over-month (m/m) growth of 1.8% was driven by bifurcated regional performance. The Midwest and South saw m/m increases of 20.6% and 6.6% while the Northeast and West weighed on results, dropping 21.4% and 13.6%. Inventories as gauged by the ratio of houses for sale to houses sold declined marginally from 9 months to 8.9. Prices also softened modestly, as the median and average levels shifted from $427,400 and $507,900 to $414,500 and $487,100.

Past performance is not indicative of future results

Fed District Reports Manufacturing Slowdown

Manufacturing conditions contracted this month in the Federal Reserve’s 5th district, according to the Richmond branch’s gauge of goods producing activities. The headline result of -4 arrived below the expected 8 and February’s 6, as capital expenditures, employment, orders and shipments weighed on results. Moreover, input costs and selling prices accelerated amidst rising expectations of continued inflationary pressures. Overall, however, survey respondents were optimistic about future momentum in the sector, expressing anticipations of stronger ordering and hiring in the coming quarters.

Interest Rate Dip Supports Equities

Equities are rising cautiously as dismal data push borrowing costs south, offering breathing room to valuations. Most major, domestic stock benchmarks are gaining with the Nasdaq 100, S&P 500 and Dow Jones Industrial indices up 0.5%, 0.2% and 0.2%, but the Russell 2000 gauge is losing 0.2%. Sectoral participation is varied, as traders do some shopping in the communication services, financials and technology segments, pushing those areas up 1.1%, 0.5% and 0.4%. Meanwhile, folks are trimming from the defensive utilities, consumer staples and healthcare components; they are lower by 1.8%, 0.7% and 0.3%. Also, a lack of momentum on new home sales is motivating selling pressure in real estate, as that industry loses 0.6% on the session. Yields and the greenback are falling on weaker US economic prospects. The 2- and 10- year Treasury maturities are changing hands at 4.01% and 4.31%, 3 basis points (bps) lighter on both fronts. The Dollar Index is decreasing by 25 bps as the US currency depreciates relative to all of its major counterparts, including the euro, pound sterling, franc, yen, yuan, loonie and Aussie tender. Commodities are mixed. Copper, silver and gold are up 2.3%, 1.9% and 0.5%, but lumber is down 0.4% and crude oil is near its flatline. Lumber is losing ground on signs that softening mortgage rates are not producing much activity in the real estate sector.

Confusion Abounds

Yesterday’s news of robust activity from S&P Global offered a stark difference to today’s sentiment data published by the Conference Board. The conflicting figures arrive at a time of confusion for consumers, corporates, government agencies and investors alike, with countering opinions on whether growth will ramp up, decelerate or fall into contraction. For now, however, the economic calendar has been generating more negative surprises than positive ones and the rest of the week offers additional clues on the transition taking place. Finally, I’ll be watching this Friday’s Personal Income and Outlays report closely to analyze the characteristics of the expected consumer spending recovery last month. Retail sales suggested a weak comeback but that print is strongly influenced by goods while the upcoming one is heavily driven by services, which comprise roughly 70% of the US economy.

International Roundup

Trade Picks Up in Asia

Hong Kong’s global trading in February soared past expectations with stronger-than-anticipated exports to China and other Asian countries. However, Hong Kong experienced a HK$36.3 billion trade deficit, according to the Census and Statistics Department. The value of exports grew 15.4% year over year (y/y), exceeding the analyst estimate of 1.7% and up considerably from January’s 0.1% growth. Exports to the US rose slightly and shipments to Europe contracted. The weakness among the two destinations was more than offset by strong demand from other Asian countries with Vietnam volume increasing 114.2% followed by Taiwan, with a 73% boost. Among products, the electrical machinery, apparatus and appliances, and electrical parts category registered the largest increases. Also in February, imports climbed 11.8% y/y compared to 0.5% in the first month of 2025 and the consensus forecast of 0.7%.

Politics Ding South Korea Consumer Confidence

Consumer confidence in South Korea sank last month as the country’s residents turned their attention to the Constitution Court reinstating impeached prime minister Han Duck-soo as acting president. For March, the consumer sentiment gauge fell from 95.2 in February to 93.4. Consumers anticipate a 2.7% inflation rate, unchanged from the last print.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

")

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account