Originally Posted 21 October 2025 – AI infrastructure at the core: WisdomTree’s AI strategy September 2025 rebalance

Key Takeaways

- WTAI’s infrastructure tilt and higher semiconductor weight are the main differentiators and performance drivers.

- Demand signals are durable: hyperscalers are scaling capacity and large, multi-year deals are in place across compute and networking.

- Diversified semiconductor exposure (GPUs, interconnect and memory) reduces single-point risk and captures rotating bottlenecks.

- The September rebalance pushes further into AI infrastructure.

- Related Products WisdomTree Artificial Intelligence UCITS ETF – USD Acc Find out more

Performance overview and positioning

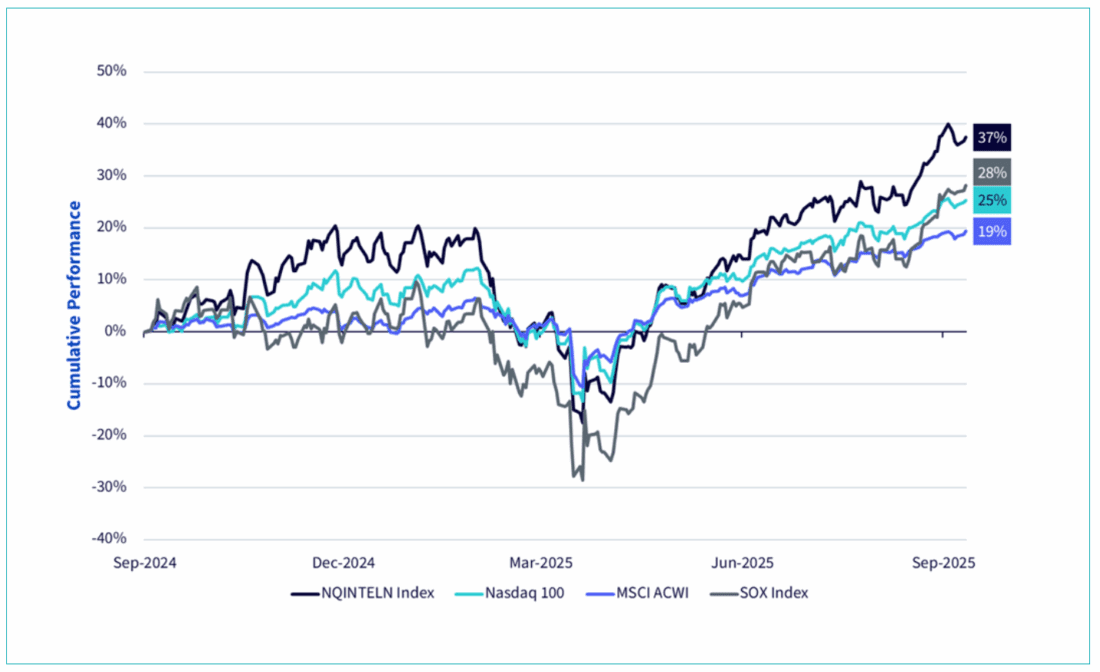

Headlines through 2025 increasingly focused on the infrastructure behind artificial intelligence (AI). Within that backdrop, WisdomTree Artificial Intelligence UCITS ETF (WTAI) saw a volatile start and a stronger rebound year-to-date. The late-January “DeepSeek shock” weighed on AI hardware exposures, then markets spent spring and summer reassessing deployment and growth. Since the September 2024 index enhancement, WTAI has outpaced major technology benchmarks over the 1-year period, driven by its overweight to the AI infrastructure layer. This same tilt also explains the relative softness when semiconductor stocks came under pressure in January and April, as well as the stronger rebound as the sector recovered.

Figure 1: Cumulative Performance since WTAI’s index enhancement in Sep 2024

Source: WisdomTree, Bloomberg. From 23 September 2024 to 30 September 2025. NQINTELN index denotes Nasdaq CTA Artificial Intelligence Index (NTR) tracked by WisdomTree Artificial Intelligence UCITS ETF. SOX Index denotes PHLX Semiconductor Sector Index. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

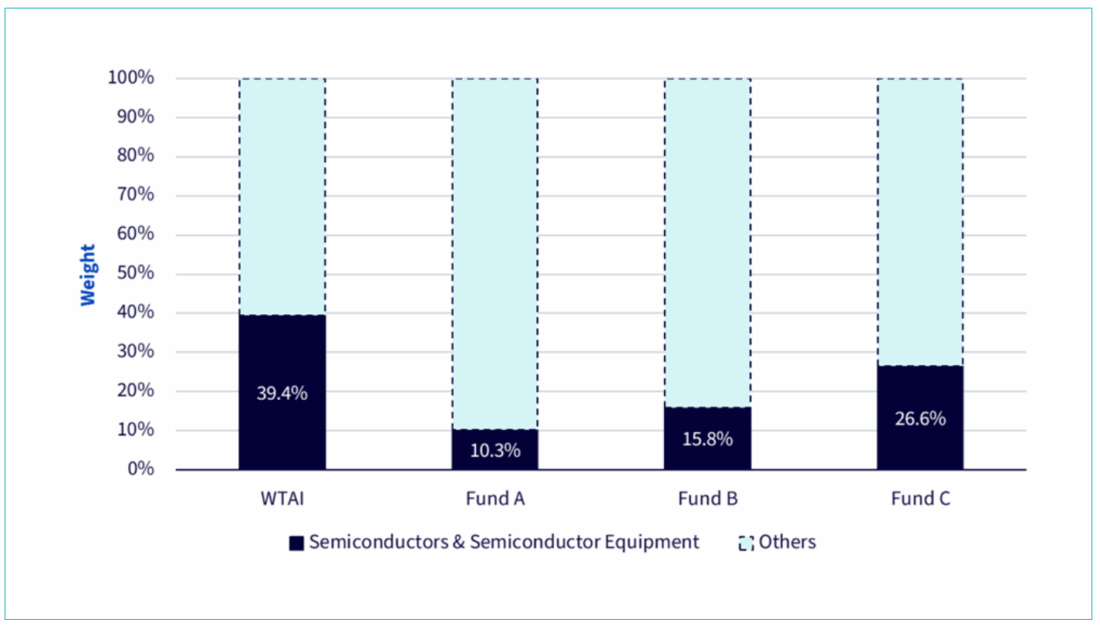

Semiconductors led the recovery. Compared with major AI themed peers, WTAI carries the highest weight in semiconductors (figure 2a). Semiconductor companies account for around 40% of the portfolio. This overweight provides more diversified semiconductor exposure, allowing the portfolio to capture opportunities not only in graphics processing units (GPUs) but also in memory and connectivity. In performance attribution, this group added approximately 20% over September 2024–September 2025 (figure 2b). That positioning hurt in January, creating around a 9% drag on returns during the period from September 2024 to early April 2025 when Trump’s ‘Liberation Day’ was announced. It set up outsized upside once demand signals and policy support firmed, adding approximately 35% from early April to end-September 2025. As adoption spreads beyond a few hyperscalers, earnings torque redistributes to chips, memory, interconnect and the tools that make them.

Figure 2a: Semiconductors exposure comparison: WTAI vs Major European AI ETFs

Source: WisdomTree, Bloomberg. As of 25 September 2025. Semiconductor exposure is represented by weights allocated in GICS industry group “Semiconductors & Semiconductor Equipment”. Fund A, B, C are the AI Themed ETFs domiciled in Europe (AUM > $500m, as of 30/09/2025). GICS is the Global Industry Classification Standard. GICS Industry Group represents second level classification in the Global Industry Classification Standard (GICS) hierarchy. Historical performance is not an indication of future performance and any investments may go down in value.

Figure 2b: WTAI Performance Attribution from Semiconductors

Source: WisdomTree, Bloomberg. As of 30 September 2025. Semiconductor exposure is represented by weights allocated in GICS industry group “Semiconductors & Semiconductor Equipment”. CTR denotes contribution to the portfolio’s return. Historical performance is not an indication of future performance and any investments may go down in value.

Semiconductor tailwinds: demand and supply

Demand stayed resilient and more visible. Hyperscaler capex kept rising, with combined quarterly spending by Amazon, Alphabet, Microsoft and Meta more than tripling since 2019 and approaching $100 billion in Q3 2025e (figure 3), alongside faster campus plans through the summer. The Stargate programme, anchored by OpenAI, Oracle and SoftBank, added new US sites, taking planned capacity toward the high single-digit gigawatt range. In parallel, OpenAI and NVIDIA set a plan to deploy 10GW of NVIDIA systems for OpenAI’s next-gen models. Meta also signed a multi-billion-dollar AI cloud agreement with CoreWeave. These commitments are translating into orders for accelerators, HBM and interconnect. These are the areas that WTAI overweights and they reinforce the case for the tilt.

Figure 3: Hyperscalers’ capex since Q2 2019

Source: WisdomTree, Bloomberg. As of 30 September 2025. Figures for Q3 2025 are averages of analysts’ estimates available on Bloomberg. Historical performance is not an indication of future performance and any investments may go down in value.

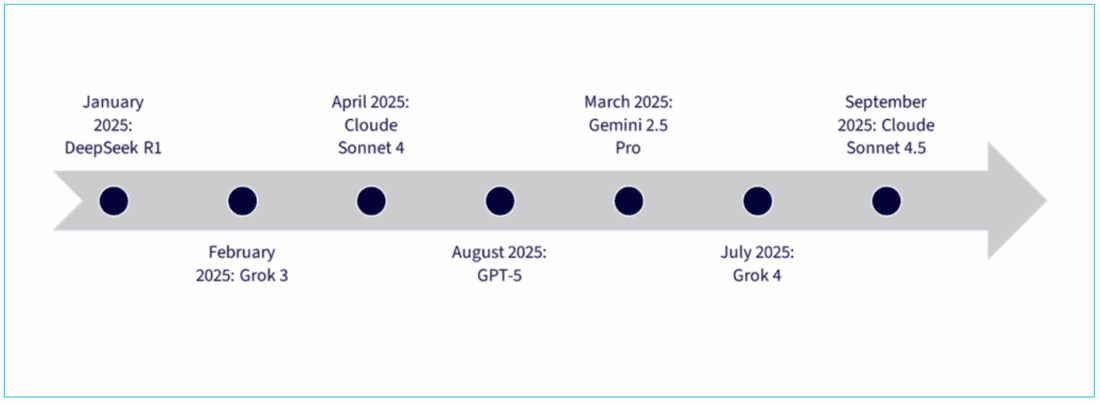

Model competition reinforced the pull on infrastructure. With OpenAI’s GPT-5, Google’s Gemini 2.5 Pro, xAI’s Grok 4 and Anthropic’s Claude Sonnet 4.5, more capable models and broader enterprise workflows pull through bandwidth, memory and interconnect higher in the stack. That is why application-specific integrated circuits (ASICs) for networking, fabric switches, and high-bandwidth memory (HBM) suppliers have featured prominently in recent months.

Figure 4: Major AI models released from Jan 2025 to Sep 2025.

Source: Alphabet, DeepSeek, OpenAI, Anthropic, xAI.

More importantly, semiconductors were not just NVIDIA. Within WTAI, Astera Labs is a useful bellwether for AI interconnects. After a January sell-off due to the ‘DeepSeek shock’, Astera Labs beat Q2 expectations and rallied into September, consistent with growing demand for links in denser clusters. Broadcom pushed Ethernet AI fabrics with next-gen Tomahawk 6 switches, and SK Hynix extended leadership in HBM3E while preparing HBM4. These examples show WTAI’s diversified semiconductor exposure spans GPUs, interconnect and memory, positioning the portfolio to benefit as spend and bottlenecks shift across the stack.

Supply conditions improved into Q3. Export-control noise proved less disruptive than feared in Q1, and industrial policy helped de-risk the chain. The US government finalised funding under the Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act for Intel to expand domestic manufacturing and advanced packaging — a clear indication that both semiconductor foundry capacity and packaging remain strategically important. That backdrop supported a rally across wafer-fab equipment and improved visibility on leading-edge logic ramps. These demand and supply tailwinds underpin our conviction in the overweight to semiconductors and AI infrastructure.

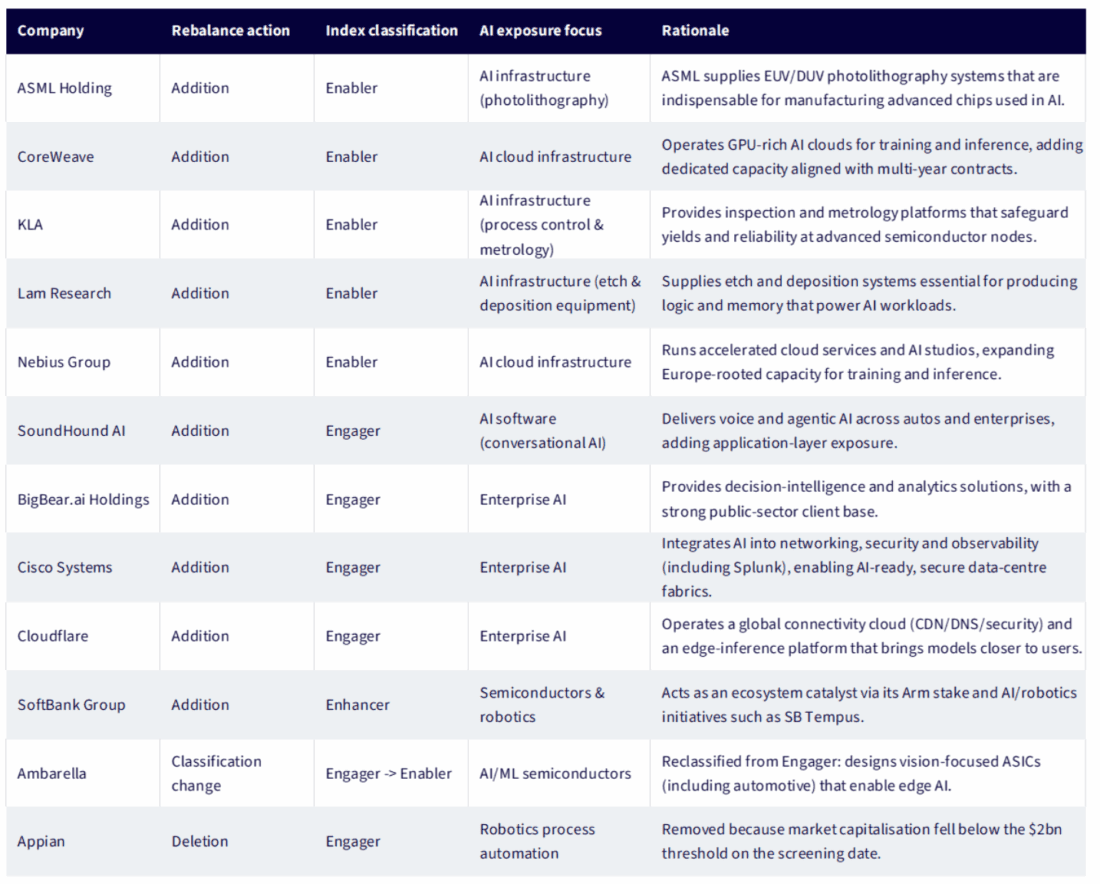

What changed in September: new entrants and why they fit

AI cloud infrastructure (Enablers): CoreWeave and Nebius operate AI infrastructure for training and inference. CoreWeave’s March IPO made it index-eligible, and its recent OpenAI contract brings 2025 deal value above $22 billion1, directly tied to Stargate’s multi-gigawatt build-out. Nebius adds a Europe-rooted platform that has recently disclosed a multi-year capacity agreement with Microsoft and new capital plans to expand clusters. Both are classic Enablers, providing the foundational computing power that Engagers depend on. Their inclusion increases WTAI’s exposure to dedicated AI cloud providers, which are central to today’s capital expenditure cycle.

The chip-making toolkit (Enablers): ASML, KLA and Lam Research extend our exposure deeper into the wafer-fab equipment stack that turns demand into silicon. ASML’s extreme ultraviolet lithography (EUV) is essential for leading-edge logic and is increasingly used in advanced DRAM. KLA’s inspection and metrology safeguard yields as geometries shrink. Lam’s etch and deposition systems form and stack device structures used across AI accelerators and HBM. As Enablers, these names benefit as foundries and memory makers push node and packaging roadmaps, an essential complement to WTAI’s existing semiconductor exposure.

Delivery and observability layer (Engagers): Cloudflare, Cisco and BigBear.ai help end-users engage with AI applications by ensuring they are fast, secure and actionable. Cloudflare provides content delivery, domain name system (DNS) and security services that ensure AI-enabled applications remain fast, reliable and available at the network edge. Cisco brings AI-ready networking and cybersecurity, plus Splunk observability, to operate and safeguard AI workloads across data centres and public cloud. BigBear.ai delivers decision-intelligence software, especially for public-sector clients, that turns heterogeneous data into operational recommendations. They translate raw compute into reliable, secure and observable user experiences.

Ecosystem catalyst (Enhancers): Through ARM Holdings, Robotics and SB Tempus, SoftBank enhances the AI ecosystem rather than selling end products. It acts as a catalyst for capital and partnerships, scaling enabling technologies (compute IP, automation) and accelerating adoption across various use cases.

Full details of additions and classification changes are summarised in the table below.

Table 1: WTAI September 2025 Rebalance: Additions, Deletions and Classification Changes

Source: WisdomTree, CTA, Nasdaq.

Conclusion

Since the September 2024 index enhancement, WTAI’s results have been driven by what matters most in this cycle: the build-out of AI infrastructure. The early-year drawdown gave way to a semiconductor-led rebound and the September rebalance strengthened that positioning with additions across AI infrastructure and semiconductor manufacturing. With hyperscaler capex and multi-year contracts pointing to multi-gigawatt capacity, a diversified semiconductor segment, GPUs, HBM, interconnect and equipment, remains central. WTAI has a higher semi-weight versus European AI peers and a strong contribution from this segment. On balance, the focus on the build-side of AI should continue to differentiate WTAI while keeping selective exposure to application delivery.

1Source: CoreWeave, as of 25 September 2025.

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account