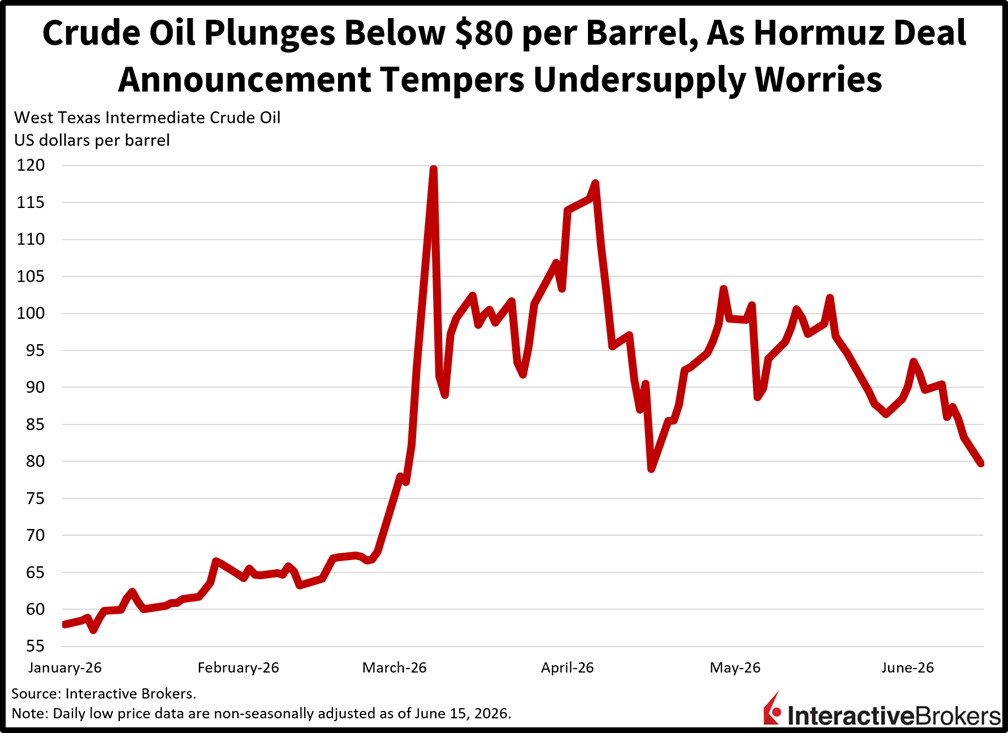

A deal to reopen the Strait of Hormuz is sparking a broad rally on Wall Street to start the week with the Dow Jones and Russell 2000 indices jumping to fresh all-time highs. The positive geopolitical development has sent WTI crude beneath $80 per barrel, its lowest level in two months, as the announcement served to temper undersupply worries. Treasurys are additionally benefiting from the drop in inflation expectations ahead of this week’s Fed meeting, which will feature new Chairman Kevin Warsh’s first presser at the helm. Indeed, the yield curve is descending in bull-steepening fashion led by the monetary policy sensitive shorter tenors while the greenback depreciates as investors price some hawkishness out of the fixed-income complex in response to cratering energy costs. Risk-on sentiments are thriving in equities, non-energy commodities as traders effectively attempt to call an end to the US-Iran military conflict. Elsewhere, volatility protection instruments are seeing lighter premiums as hedging demand drops.

Past performance is not indicative of future results.

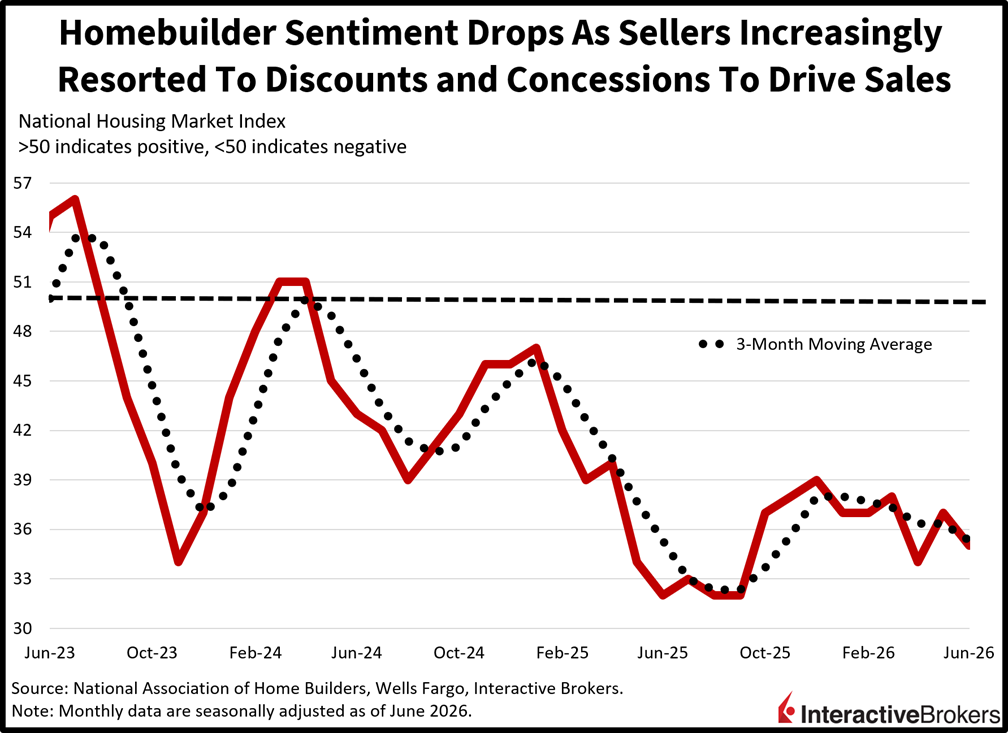

Homebuilder Sentiment Falls Below Expectations

Construction firms are increasingly resorting to discounts and concessions to drive closings as homebuilder sentiment fell last month against the backdrop of worsening affordability conditions. The Wells Fargo/NAHB June headline figure of 35 arrived beneath the median estimate of 36 and May’s 37, as elevated mortgage rates and lofty valuations weighed on confidence. The sub-index of single-family sales in the present sank from 40 to 38, while the outlook for the next six months and the traffic of prospective buyers remained flat at 45 and 25. The regions were bifurcated, with the Northeast expanding from 44 to 50, the South declining from 36 to 29, and the Midwest and West staying unchanged at 45 and 27. Overall, 35% of builders cut prices compared to 32% from the prior period, although the average reduction stayed at 6%. Additionally, the use of incentives rose to 62% from 61%.

Past performance is not indicative of future results.

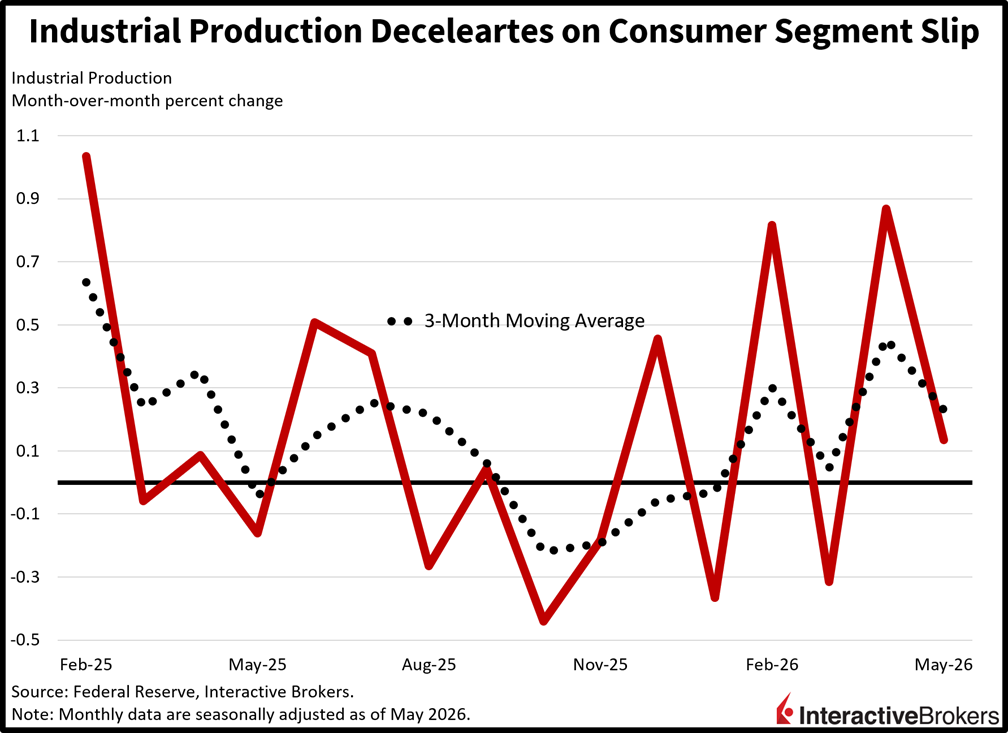

Consumer Weakness Weighs on Factory Activity

Industrial production decelerated in May as a retreat in consumer items weighed on overall performance. The headline figure grew just 0.1% month over month (m/m), thanks to the mining sector expanding 1.3% m/m while utilities declined 0.4% and manufacturing was flat. The result arrived beneath the 0.3% median estimate and the 0.9% recorded in April. Despite household goods contracting 0.5%, there were broad-based gains across the other major market groups. Indeed, construction, business equipment and materials expanded 1.1%, 0.6% and 0.3% m/m.

Past performance is not indicative of future results.

Outlook Buoyant as War Risk Diminshes

The outlook for economic growth and corporate earnings is increasingly buoyant now that risk from the war has diminished. Investors are responding by piling into stocks in offensive sectors to position for an expected acceleration in positive performance. Bonds are also catching bids, as inflation is heading back to a 3-handle in next month’s report if this drop in crude holds, which is quelling the fears of fixed-income watchers that were nervous of a move higher towards 5. The resulting loosening in financial conditions occurs at a time when animal spirits are thriving, and that combination is a stellar one for equities today.

International Roundup

Euro Area Reports Global Trade Deficit

The euro area’s imports exceeded exports €1.0 bn in April, which was a reversal from the €4.9 billion March surplus and driven primarily by energy costs shipped into the region, according to Eurostat. It was only the second monthly trade deficit since May 2023 and much worse than the economist consensus estimate for a €7.8 billion surplus. Imports jumped 9.3% year over year (y/y) while exports were up only 5%.

Energy was the largest contributor to the imbalance with value of the commodities imported exceeding exports by €28.8 billion, a result of higher oil costs following the US attack on Iran and the resulting close of the Strait of Hormuz. Raw material exports, furthermore, were €3 billion below imports. The other manufactured goods group, furthermore, experienced a €400 million trade deficit. The strongest trade surpluses occurred in the chemicals and related products groups and the machineries and vehicles category where the value of items shipped to foreign lands exceeded imports by €28.3 billion and €6.8 billion.

While Industrial Production Is Mixed

Industrial production in the euro area climbed 0.1% m/m and 0.3% y/y, according to a preliminary estimate from Eurostat. The monthly pace slowed from 0.4% but still surpassed the economist consensus estimate of 0.2% while the y/y print was an improvement from the 2.8% descent in March.

Output of intermediate goods, durable consumer goods and non-durable consumer goods climbed 0.8%, 1% and 1.7% m/m while production of energy and capital goods sank 0.4% and 0.5%.

Japan Service Industry Gauge Strengthens

Japan’s Tertiary Industry Index, which measures activity in the country’s services sector, climbed 1.3% m/m in April, a reversal from the 0.2% slip in the preceding month, according to the Ministry of Economy, Trade and Industry. It also climbed 2.2% y/y. The portion of the gauge focused on personal services was up 1.2% m/m and 1.7% y/y while the businesses sector version was 1% and 2.5% higher m/m and y/y. Finance and insurance led the gains, ascending by 3.2% and 10.8% m/m and y/y. Other categories with gains and the extent of their m/m growth were as follows:

- Wholesale trade, 2.6%

- Information and communications, 2%

- Living and amusement-related services, 1.7%

- Retail trade, 1.4%

- Medical, health care and welfare, 0.5%

- Business-related services, 0.5%

- Real estate, 0.4%

Electricity, gas, heat supply and water was the only classification that contracted. It posted a 0.5% m/m decline.

Singapore Payrolls Expanded in First Quarter

Singapore just recorded its 18th consecutive quarter of payroll expansion with employers adding 9,400 workers during the first three months of 2026. While employment growth of non-residents slowed, resident hires accelerated to 5,400 from 3,100 in the final quarter of 2025. Meanwhile, the country’s unemployment rate was unchanged at 2%, a stronger showing then the economist consensus estimate for an increase to 2.1%.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account