Excitement about AI alongside easing tensions in the Middle East had stocks cautiously climbing for the second consecutive day before valuation concerns and elevated yields motivated bears to spark a severe intraday reversal selloff in U-turn fashion. Indeed, equities are now well off their highs this session, but in a much more dramatic panic than yesterday, when bulls failed to hold strong benchmark gains north of 1% into the close. Part of this Tuesday’s hysteria stems from investors waiting for key CPI and PPI inflation reports in the next two days, which are expected to increase at their fastest annualized figures in over three years on the back of the surge in fuel costs driven by the ongoing Strait of Hormuz closure. The prints are likely to also reflect that heavier gasoline charges are increasingly spreading to the overall economy while supporting the outlook for rate hikes. Today’s data, meanwhile, wasn’t high impact, although a deceleration in ADP weekly hiring coincided with an unexpected decline in small business optimism as well as a beat on existing home sales. Turning to trading, all sectors minus energy were in the green prior to tech unexpectedly tanking approximately 30 minutes after the opening bell, and now 9 of the 11 major categories are rising. Geopolitical relief has fixed income catching bids, as a 3.6% drop on WTI crude oil has rates and the greenback sinking, which is lightening financial conditions. Elsewhere, commodities are mixed.

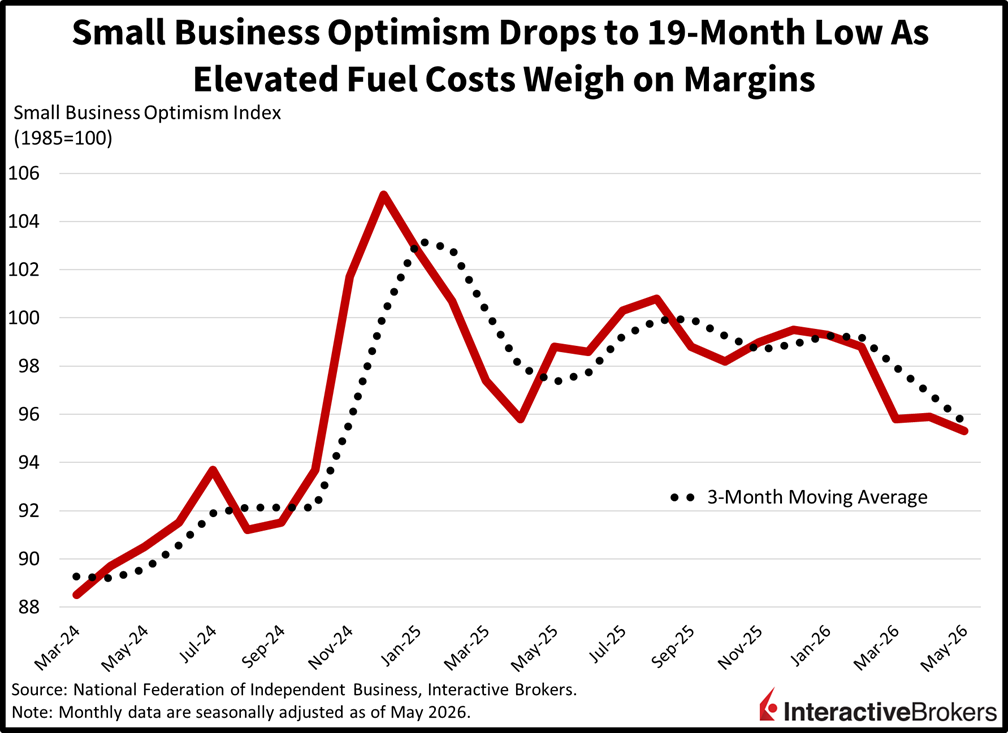

Energy Inflation Dings Small Business Sentiment

Elevated energy charges weighed on small business optimism last month, as firms had trouble sustaining margins against the backdrop of cautious shoppers. The National Federation of Independent Business’s (NFIB) headline figure of 95.3 marked a 19-month low and arrived beneath the median estimate of 96 and April’s 95.9. The following sections weighed on the result:

- Reductions in hiring plans and job openings

- Declining capital expenditure intentions

- Declining inventory levels

- A weaker economic outlook, including softer sales expectations

But earnings improved, as did projected credit conditions and future inventory growth.

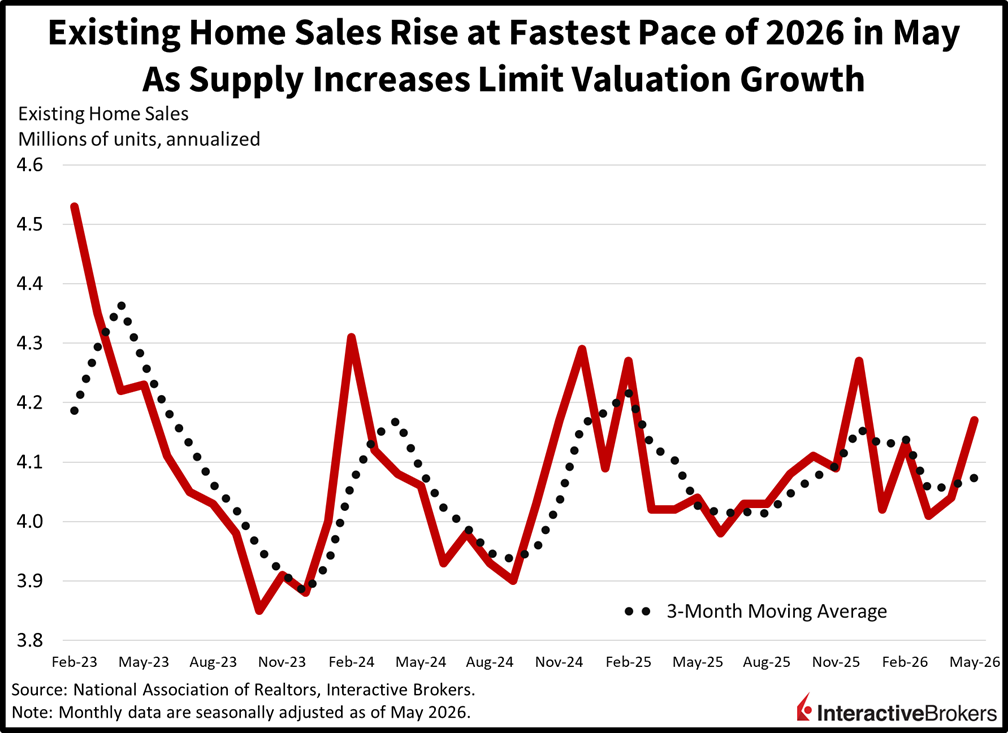

Nevertheless, Home Sales Strengthen

Existing home sales in May rose for the second consecutive month, hitting the fastest acceleration of 2026. The 4.17 million seasonally adjusted annualized units (SAAU) climbed 3.2% month over month (m/m) and arrived ahead of the 4.07 million projection and 4.04 million in April. The single-family segment drove the gains with a 3.5% m/m climb, offsetting the flat performance in the cooperative/condominium category. Across regions, the Midwest, South and Northeast advanced by 6.4%, 3.2% and 2.2% m/m while the West was unchanged. Inventories grew 3.3% m/m, as more prospective sellers listed their properties, effectively limiting the growth in median closing prices to a 1.3% year-over-year (y/y) expansion to $429,300.

Business Hiring Slowed Modestly at End of May

Private sector hiring eased slightly toward the end of last month, marking the third consecutive week of deceleration in employment additions. Businesses added an average of 29k employees in each of the four weeks during the period that ended May 23, which was weaker than the 30.5k from the prior print, according to ADP. Still, a monthly run rate of 126k isn’t too shabby.

In-Line CPI Would Still Be in Nosebleeds

The potential for tomorrow’s Consumer Price Index (CPI) to relieve market participants is complicated because an in-line print would be too far into the nosebleeds. Indeed, the 4.2% median estimate would be the highest figure since April 2023, or a 37-month high, although decelerating rents and slow gains in housing valuations are expected to keep the core number closer to 3% at 2.9%, the loftiest since last September. These elevated inflation statistics have investors wondering how new Fed Chair Kevin Warsh will react as he gears up for his first meeting at the helm of the central bank next week. Fixed-income watchers are highly attentive to the former hawk, as the funds curve carries a 69% chance of at least a 25-basis point lift this year. The base case of a hike offers an interesting déjà vu as we progress through 2026, with President Trump wanting cuts rather than increases while his nominee has his hands tied by a Treasury complex that is yelling tighter not looser.

International Roundup

China Trade Surplus Exceeds Expectations

China’s trade surplus climbed from $84.8 billion in April to $105.4 billion last month, easily exceeding the $92.1 billion economist consensus estimate. Exports jumped 19.4% y/y, surpassing the 15% economist consensus estimate and April’s 15.1% expansion. Meanwhile, imports climbed 27.4% compared to the forecast for 25% growth and April’s 25.3% ascent. Strong shipments of artificial intelligence products to foreign markets and a 35% jump in goods shipped to the US were tailwinds for the country’s trade balance. Higher prices for hydrocarbon fuels, furthermore, have stoked global purchases of the country’s renewable energy products.

Oil Exports and US Trade Boost Canada’s Goods Trade Surplus

Exports of cars to the US and stronger shipments of oil to foreign markets helped Canada’s April trade surplus climb from C$1.78 billion in the preceding month to C$2.72 billion, according to Statistics Canada. It was the strongest surplus since January of last year and north of the C$2.5 billion level anticipated by economists. Products shipped beyond the country’s borders totaled C$75.16 billion, up from C$73.98 billion in March. Meanwhile, a total of C$72.44 billion of products flowed into the country compared to C$72.23 billion in the third month of the year.

Foreign markets snatched up a smaller amount of gold, but higher energy prices inflated the value of Canada’s energy exports, including oil and refined products. Also in April, the US increased its purchases of Canadian products by 4.8% but experienced only a 1.6% lift in the value of items transported across its northern border.

Heatwave Reverses UK Retail Sales

After dropping 3% y/y in April, UK retail sales were up 3.7% in May with a heatwave causing shoppers to splurge on outdoor equipment and summer goods, according to the BRC Retail Sales Monitor. Transactions exceeded expectations for a slower 0.8% ascent and the 12-month average growth of 2%. Food and non-food sales were 3.9% and 3.5% higher than in the year-ago period and blew past the 12-month average y/y expansion rates of 3.5% and 0.7%. Non-food online sales were 10.6% stronger than in May 2025, but brick and mortar stores experienced a 0.4% decline. The disparity is underscored by ecommerce representing 38% of non-food sales, a 2 percentage point gain from the year-ago period. The British Retail Consortium (BRC) says sales of summer clothing and footwear turned positive last month while air conditioners and fans experienced strong demand. Rather than brave record-high temperatures, consumers shopped online from the comfort of their homes. Also during the month, a bank holiday supported sales of food and barbecues.

South Korea Revises GDP Higher

South Korea has revised its first-quarter gross domestic product growth rate from its April estimate of 1.7% to 1.8% on a quarter-over-quarter basis. It also updated its annualized growth estimate from 3.6% to 3.8%.

Australia Consumer Confidence Weakens

Australian consumers have become less confident with the Westpac-Melbourne Institute survey for June showing a 2.9% decline, or a descent from 83 to 80.6. A reading of 100 implies that numbers of pessimists and optimists are equal. The size of the gap between a number below the threshold indicates the extent to which the number of consumers with negative economic views outweighs the number of upbeat shoppers. Rising borrowing costs and higher energy stickers were the primary culprits of the survey’s decline.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account