Hotter-than-expected economic figures signaling cyclical momentum are countering valuation concerns that pushed stocks lower in the past several days. Indeed, equities are advancing strongly this session, even as interest rates rise in response to firmer growth projections and data that are quelling slowdown fears. More specifically, ADP reported the fastest pace of private sector hiring in three months, which eased worries about potential labor market deterioration. Additionally, ISM-services beat expectations, a result of robust consumer spending that is improving businesses’ pricing power amidst accelerating inflation as detailed in the same print. Buoyant activity that is strengthening price pressures, furthermore, is sending the yield curve north in bear-steepening fashion led by duration, while the odds of a December Fed rate cut are drifting further south and are at 62%. Anticipation of the awaited economic updates that have been reduced in frequency by the extended government shutdown are also supporting the greenback’s climb. Risk assets are rallying, too, with broad participation across most equity sectors and commodities, excluding the defensive categories in stocks as well as real estate shares and lumber, which are suffering because of pricier mortgages, which correlate with rising long-end borrowing expenses. Volatility protection instruments are being neglected due to the recovery in investor sentiment and lessening hedging demand.

Employers Roll Out the Welcome Mat

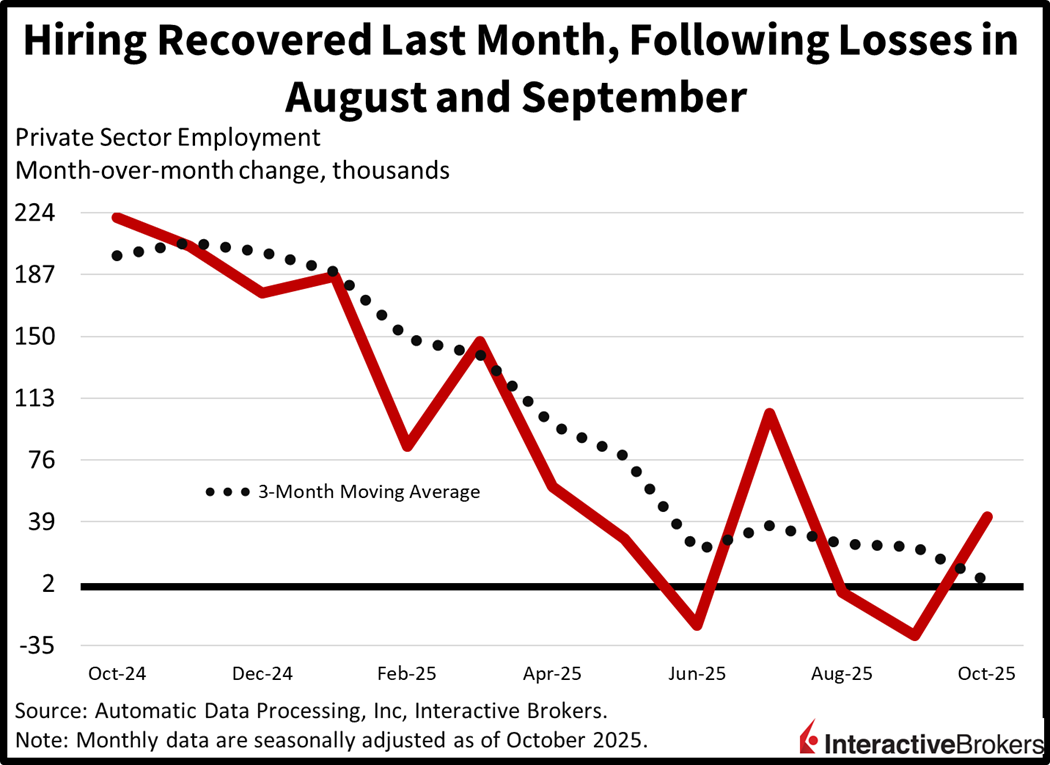

The US private sector added jobs for the first time in three months in October, although the pace of expansion remains well below the momentum experienced earlier this year, according to payroll firm ADP. Immigration restrictiveness, AI adoption and hiring caution in the rate sensitive real estate, goods producing and small business categories are hampering labor conditions. Still, the 42k headline gain beat the projected 25k and recovered from September’s loss of 29k. The following categories and the amount of their staffing changes expanded payrolls:

- Trade/transportation/utilities, 47k

- Education/health services, 25k

- Financial activities, 11k

- Natural resources/mining, 7k

- Construction, 5k

Sectors with contracting headcounts and the scope of the changes included the following:

- Information, 17k,

- Professional/business services, 15k

- Other services, 14k

- Leisure/hospitality, 5k

- Manufacturing, 3k

Establishments with 499 employees or fewer reduced headcounts by 32k, but larger firms countered the weakness, boosting rosters by 74k. Compensation trends were steady, however, as the median year-over-year (y/y) pay hikes remained at 6.7% and 4.5% for job stayers and changers, respectively.

Past performance is not indicative of future results.

ISM Services Gauge Surpasses Expectations

The Institute for Supply Management (ISM) also posted a beat, as accelerating consumer demand bolstered pricing power amongst businesses. The headline reading of 52.4 for the Services Purchasing Managers’ Index (PMI) flew past estimates of 50.8 and improved from September’s 50 print, which is the contraction-expansion threshold. New orders and prices climbed from 50.4 and 69.4 to 56.2 and 70, as heavy transaction volumes supported loftier costs. But the employment score signaled that firms continue shedding headcounts and stands in contrast to ADP, even as the 48.4 result rose from the prior period’s 47.2.

International Roundup

China’s Services Sector Growth Slows

China’s services industry expanded during October at the slowest pace in three months with the sector’s RatingDog China PMI from S&P Global slipping from 52.9 in September to 52.6 but narrowly surpassing the economist consensus estimate of 52.5. While new business grew, the uptick was limited to the domestic market. Export sales, staffing levels and gate prices all descended. Services providers also faced the fastest rate of input inflation in a year with wage pressures and raw materials accounting for much of the trend. Unfilled backorders, meanwhile, declined despite the higher flow of new business with services providers’ efficiency improving. Looking ahead, business confidence was still positive despite declining slightly with some managers expressing concerns about global trade.

Wholesale Prices Fall Again in Europe

Euro area wholesale prices dropped 0.1% month over month (m/m) in September, a slower pace than the 0.4% drop in the preceding month, according to the Producer Price Index. Economists anticipated no change.

Relative to September 2025, the gauge was down 0.2%, which matched the economist consensus estimate and moderated from the 0.6% descent in August. Energy costs fell 0.2% while capital goods were unchanged. Durable consumer and non-durable consumer goods were 0.3% and 0.1% more expensive.

Hong Kong Business Activity Grows for Third Month

Hong Kong’s overall private sector activity moved further above the S&P Global PMI contraction-expansion threshold of 50 with the gauge climbing from 50.4 in September to 51.2 last month. It was the third-consecutive monthly improvement. October featured the steepest climb in output and new business in the past 12 months. In response, businesses added employees and increased their purchasing volumes. Input cost increases eased, but firms passed the higher costs onto customers. Local Asian markets drove the higher demand with orders from Mainland China growing for the first time in a year. Conversely, businesses had a downbeat view of conditions during the coming year, primarily a result of US import taxes and the shift toward online consumption. Nevertheless, sentiment is still better than it has been for most of 2025.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account