Originally Posted, 11 June 2025 – Enhancing gold exposure for non-USD investors

Key Takeaways

- The US dollar has weakened after a period of strong appreciation.

- Dollar movements significantly impact gold prices in USD terms.

- Non-USD investors may miss gains due to adverse currency effects.

- Currency hedging gold can help EUR and GBP investors boost returns.

After a prolonged appreciation comes a depreciation phase for the US dollar

The US dollar basket appreciated significantly between May 2021 and September 2022, rising by 25% as the Federal Reserve (Fed) led the global monetary tightening cycle. However, from September 2022 to October 2024, the dollar mostly depreciated within a range, falling around 10%. A sharp rebound followed, with the dollar gaining 10% between October 2024 and January 2025. This surge was driven by the perception that the US economy was on a stronger footing than its peers, reducing expectations of imminent monetary easing by the Fed—supporting dollar strength.

The appreciation accelerated following Donald Trump’s victory in the November 2024 US presidential election. Markets anticipated pro-growth, low-tax policies would further boost the economy. However, since January 2025, the dollar has weakened considerably, with the dollar basket now trading well below its October 2024 trough. Much of the earlier optimism surrounding Trump’s policies has eroded, particularly amid rising concerns about demand destruction stemming from an escalating trade war. The dollar basket is now down nearly 10% from its January 2025 peak.

Figure 1: US dollar basket (DXY)

Source: WisdomTree, Bloomberg. January 2020 – April 2025. Monthly data. Dollar Basket (DXY) is a measure of the value of the US dollar against a basket of currencies (Euro, Swiss franc, Japanese Yen, Canadian Dollar, British Pound and Swedish krona). Historical performance is not an indication of future performance and any investments may go down in value.

Market outlook: further dollar weakness expected

Market sentiment suggests further dollar weakness. According to Bloomberg’s survey of foreign exchange analysts, the dollar basket is expected to decline from its current level of 100 to 97.6 by Q1 2026. Forward markets also indicate euro appreciation against the dollar, with the EUR/USD exchange rate projected to rise from 1.13 to 1.16 over the same period.

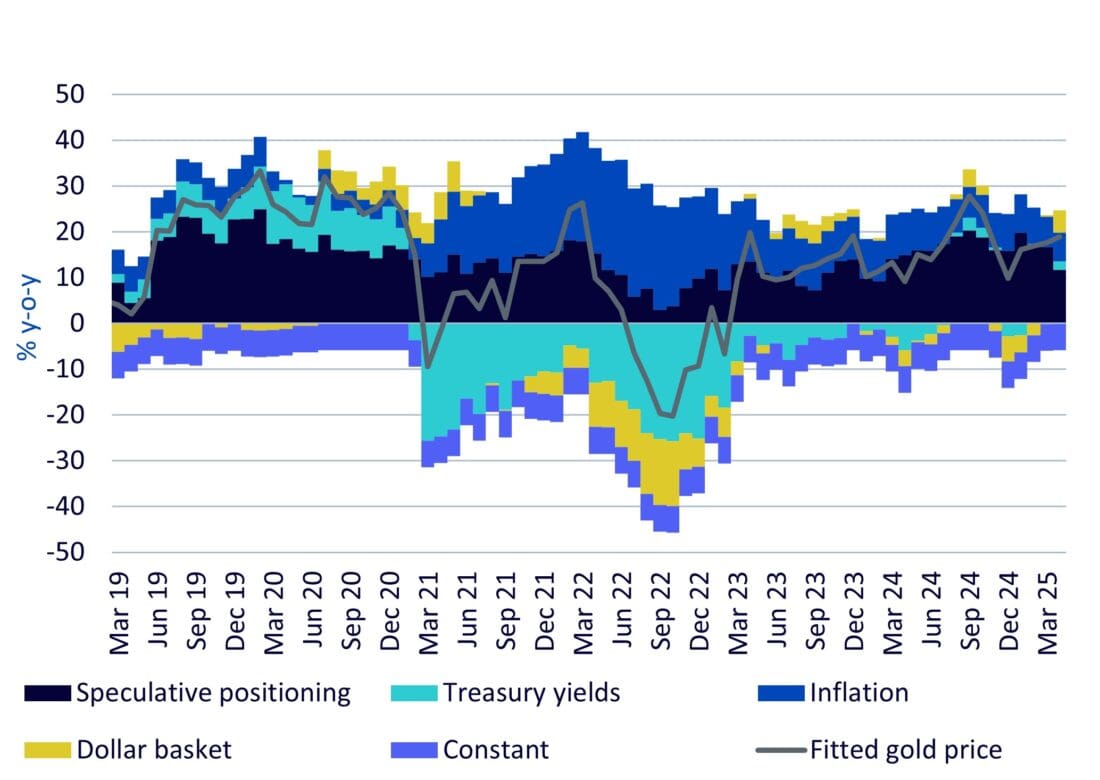

US dollar and gold

The US dollar exchange rate is a key driver of gold price behaviour in dollar terms. Our proprietary gold model shows that the dollar’s appreciation during 2021–2022 significantly weighed on gold performance. In contrast, dollar depreciation in 2023 contributed positively to gold prices. More recently, in March and April 2025, renewed dollar weakness once again supported gold gains.

Figure 2: Gold price attribution

Source: Bloomberg, WisdomTree price model, data as of April 2025. Fitted gold price is growth in gold price (year-on-year) expected by the model. The bars represent the components of the model. Speculative positioning is net non-commercial positioning in gold futures markets (that is, netting shorts away from long positions as reported by the Commodity Futures Trading Commission). Treasury yields is the nominal yield to maturity on a 10-year US Treasury Bond. Inflation is the annual growth of the US Consumer Price Index. Historical performance is not an indication of future performance and any investments may go down in value.

Capturing all gold gains for a non-USD investor

For investors managing portfolios in non-USD currencies, gains from gold’s appreciation due to dollar depreciation can be elusive—especially if the dollar is weakening against their home currency. As illustrated in the chart below, gold’s strongest performance has been in USD terms. In contrast, gold priced in EUR and GBP has appreciated only about half as much.

Figure 3: Gold performance in various currencies

Source: WisdomTree, Bloomberg. 1 January 2025 – 23 May 2025. Daily data. Historical performance is not an indication of future performance and any investments may go down in value.

Investors managing portfolios in EUR or GBP can enhance returns by using currency-hedged gold products. Currency hedging allows them to benefit more directly from gold price movements, without the drag from adverse currency shifts.

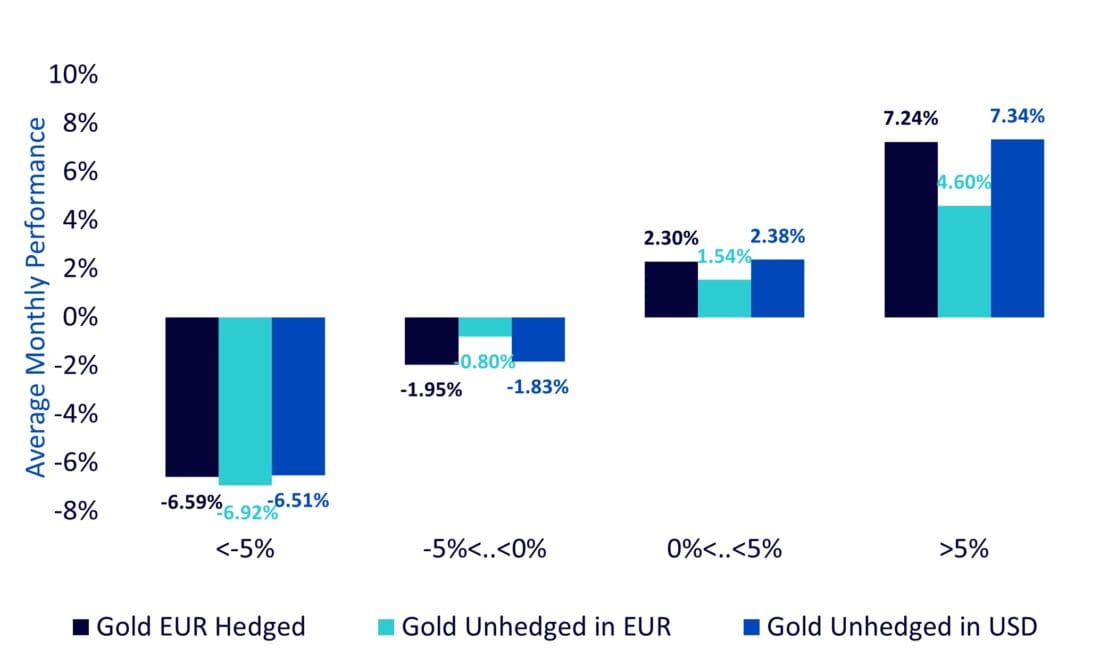

Historically, currency hedging has helped investors capture more of gold’s upside:

In EUR terms, since 2004, during months when gold prices rose more than 5%:

- Unhedged EUR gold exposure increased by 6.53% on average.

- USD gold increased by 7.79%, creating a gap of 1.26%.

- Currency-hedged EUR gold exposure rose 7.67%, narrowing the gap to just 0.12%.

Figure 4: Historic performance of gold, hedged and unhedged, EUR

Source: WisdomTree, Bloomberg. December 2003 – April 2025. Monthly data. Historical performance is not an indication of future performance and any investments may go down in value.

In GBP terms, since 2016, during similar gold surges:

- Unhedged GBP gold exposure increased by 4.60% on average.

- USD gold rose by 7.34%, a gap of 2.74%.

- Currency-hedged GBP gold exposure gained 7.24%, reducing the gap to just 0.10%.

Figure 5: Historic performance of gold, hedged and unhedged, GBP

Source: WisdomTree, Bloomberg. December 2016 – April 2025. Monthly data. Historical performance is not an indication of future performance and any investments may go down in value.

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account