The article “The Many Facets of Stock Momentum” was originally posted on Alpha Architect blog.

Stock momentum has long been a workhorse idea. Buy recent winners. Sell recent losers. Critics argue those profits mostly come from riding factor trends like value, size, or industry tilts. This paper pushes back. It shows there is a durable, stock-specific momentum component tied to how prices react to firm news around earnings dates. The result is a cleaner, lower-risk way to capture momentum without leaning so heavily on broad factor moves.

The Many Facets of Stock Momentum: Distinguishing Factor and Stock Components

- Xavier Gérard and Laura Jehl

- Financial Analyst Journal, 2025

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

Key Academic Insights

• There is real stock-specific momentum, not just factor timing

The authors isolate the part of 12-month momentum that comes only from returns in short windows around each firm’s earnings announcements over the prior year. This earnings-announcement component predicts future returns in the US, Europe, and Japan over three decades. It remains significant after controlling for changing factor exposures.

• Classic momentum loads on factors, the earnings-announcement component does not

Traditional 12-1 momentum carries substantial exposure to market, value, and industry effects. The earnings-announcement strategy shows much lower systematic risk and a high correlation between long and short legs. That makes it a purer expression of firm-level information.

• Short-term PEAD has faded, longer-horizon announcement momentum persists

Strategies that trade only the latest earnings surprise have weakened in recent years. Aggregating all announcement windows over the past year continues to work. Turnover is also about half that of the short-horizon approach.

• Factor momentum can subsume classic stock momentum in the US but not the announcement component

A principal-component factor-momentum strategy is strong in the US and explains classic momentum. It does not explain the longer-term earnings-announcement strategy. That piece remains economically and statistically robust.

• Long-run behavior differs, classic momentum can reverse, announcement momentum does not

When you extend formation to 24 months and skip a year before holding. classic momentum shows reversal in the early 2000s, consistent with prior evidence of overreaction. The earnings-announcement component shows no short- or long-run reversal. consistent with underreaction to firm-specific news.

Practical Applications for Investment Advisors

• Use earnings based momentum as your “core” sleeve

When you allocate to momentum, prioritize a sleeve that is built only on returns around earnings announcements over the last year. It is still momentum, but it is closer to company specific news and less dependent on style or market swings. This can sit alongside your value, quality, and low volatility tilts in a multi factor portfolio.

• Be explicit about how much factor risk you want

Classic momentum often hides big bets on growth versus value, sectors, and industries. If you already get those tilts from other parts of the portfolio, size classic momentum smaller and size the earnings announcement sleeve larger. For model portfolios, treat announcement based momentum as a “clean” stock selection overlay. treat classic momentum as a more cyclical factor bet.

• Use momentum as a behavior story, not a magic trick

This paper supports a simple narrative you can share with clients. Markets are slow to fully price company specific news, especially when it comes drip fed through multiple earnings announcements. You are not “chasing heat”. You are systematically leaning into places where investors underreact to information and away from places where they tend to overreact to broad market themes. That framing helps clients see momentum as disciplined process, not speculation.

How to Explain This to Clients

“Momentum isn’t just riding waves in big style factors. Some of it comes from markets slowly digesting company-specific news around earnings. By focusing on those brief windows, we can capture a steadier form of momentum with fewer side bets on value, size, or industries. It is a cleaner way to use momentum in a diversified portfolio”

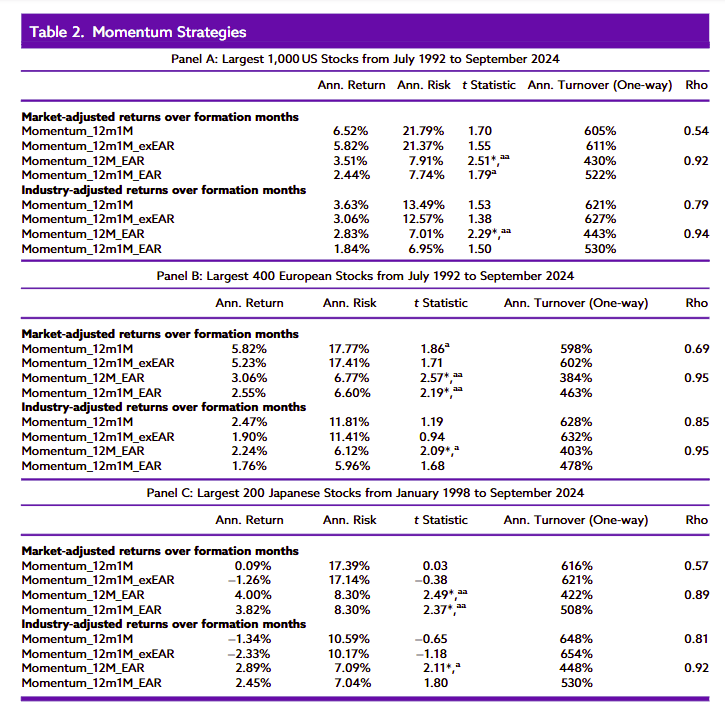

The Most Important Chart from the Paper

Table 2 compares analysis of the performance of a traditional stock momentum strategy and that of the longer-term earnings-announcement strategy in the large-capitalization segments of three developed markets: the US, Europe, and Japan.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index. Past performance is not indicative of future results.

Abstract

This study aims to investigate the recent controversy surrounding the existence of stock-specific momentum. Stock momentum consists of both factor- and stock-specific components, but the risk associated with factor momentum might hinder the impact of stock-specific momentum. Using earnings announcement returns that occur during the formation months of the stock momentum strategy, the study captures a component largely unaffected by factor momentum, thereby mitigating the bad-model problem. This stock-specific momentum source predicts future returns, does not reverse in the long run, and is pervasive, as similar results are found in the US, Europe, and Japan over the last 30 years.

Disclosure: Alpha Architect

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account