Originally Posted 21 August, 2025 – Chart to watch: Are corporate credit spreads too tight?

Authors: Tim Winstone, CFA , Brad Smith and Celia Soares

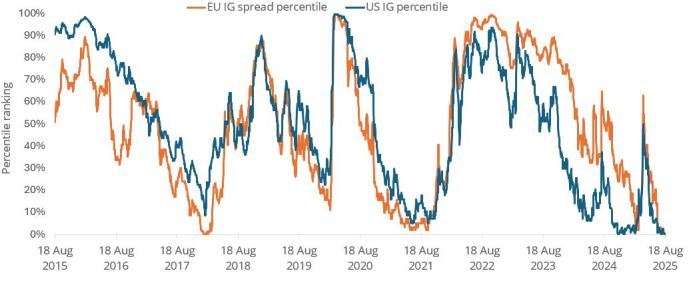

US investment (IG) spreads are around all-time tights, while Euro IG spreads are at the post Global Financial Crisis lows seen around seven years ago, when the hunt for yield amid low rates drove demand for credit. Have we then reached peak compression? As uncertainties and risks remain, how can investors navigate this environment?

Key takeaways:

- IG credit spreads have tightened due to strong supply-demand dynamics, better-than-expected economic data, and tariff relief.

- A slowing supply of IG credit in H2 and corporate fundamentals, supported by AI-driven capital expenditures (capex), are key to watch as potential supportive factors for spreads going forward.

- Dispersion in individual credits could rise from here as the impact of tariffs is priced in, so careful security selection alongside a shift to higher quality could aid portfolio resilience amid uncertainty.

Source: Janus Henderson Investors, Bloomberg, EU IG: ICE BofA Euro Corporate Index; US IG: ICE BofA US Corporate Index, as at 18 August 2025. Past performance does not predict future returns.

Behind the tightening of IG credit spreads, strong technicals (supply/demand dynamics), better-than-expected economic data, and tariff relief have been drivers. There has been a record quarter of inflows into European IG credit[1], driven by attractive yields. The initial yield is crucial as it largely determines the total returns in fixed income.

The supply of European IG credit is expected to slow in the second half of the year, which means technicals should continue to remain supportive for spreads. This is similar in the US, where the net supply is anticipated to be negative for 2025[2]. Another tailwind for the asset class is corporate fundamentals accelerating in 2026, driven by higher deficit spending increase from the ‘One Big Beautiful Bill’ (OBBB)[3] and a beneficial tax environment, supported by easing monetary policy in the US, while Europe gains from German-led fiscal stimulus.

Corporate fundamentals are under scrutiny, especially as companies increase spending driven by Artificial Intelligence (AI).

Despite tariffs being enacted, landing at 15% for Europe, markets have remained resilient, and the worst-case scenario has been priced out by trade deals and investor optimism. But we expect tariffs and tight spreads to undoubtedly lead to intra-sector dispersion in corporate credit as investors begin to price in the impact across supply chains and sector dynamics. Our investment focus is shifting to higher quality while taking advantage of single name opportunities and maximising carry, a key determinant of total returns in fixed income.

Footnotes

[1] Source: Morgan Stanley based on EFPR data, between May and July 2025.

[2] Source: JP Morgan, as at July 2025. There is no guarantee that past trends will continue, or forecasts will be realised.

[3] The OBBB, or One Big Beautiful Bill, is a U.S. federal statute enacted by the 119th Congress, primarily focused on tax and spending policies as part of President Donald Trump’s second-term agenda

ICE BofA Euro Corporate Index: The ICE BofA Euro Corporate Index is an index that tracks the performance of investment-grade corporate bonds denominated in Euros.

ICE BofA US Corporate Index: The ICE BofA US Corporate Index value, which tracks the performance of US dollar denominated investment grade rated corporate debt publicly issued in the US domestic market.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Disclosure: Janus Henderson

The opinions and views expressed are as of the date published and are subject to change without notice. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes and are not an indication of trading intent. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Janus Henderson and is being posted with its permission. The views expressed in this material are solely those of the author and/or Janus Henderson and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account