Originally posted, 24 March 2025 – What do Germany’s spending plans mean for economic growth?

Germany’s parliament has approved plans by incoming Chancellor Friedrich Merz to loosen borrowing limits. The law will exempt spending on defence and security from Germany’s strict debt rules. It also enables the creation of a €500 billion infrastructure fund.

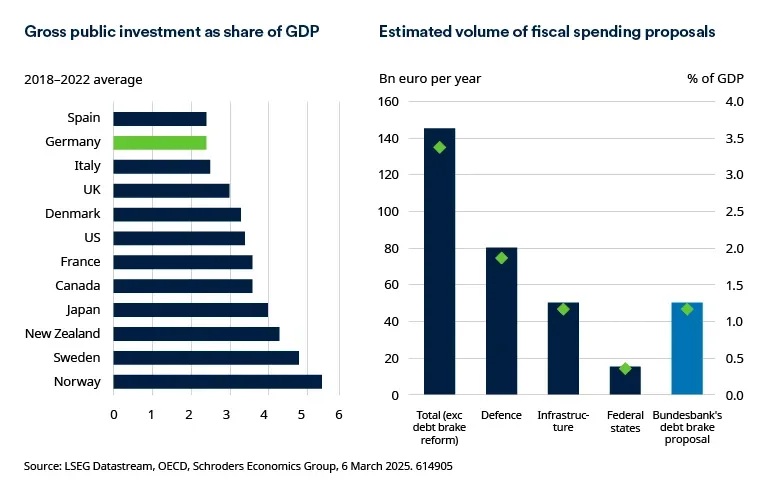

Significant shift in fiscal spending

This represents a very important change to fiscal policy. Germany has traditionally been a laggard among high-income countries in terms of gross public investment, prioritising balanced budgets instead. The recent stimulus is set to increase the spending-to-GDP ratio by more than two percentage points per year.

Looking closer at the details of the proposal, defence expenditure exceeding 1% of GDP is exempt from the constitutional debt brake (the debt brake keeps the structural deficit below 0.35% of GDP).

EU leaders have recently highlighted their preference to tilt defence spending towards European producers rather than buying US weapons. While this is stimulative of economic growth, it could increase geopolitical tensions with the US and raises risks of a trade war between the two sides of the Atlantic.

The debt brake will also be changed to allow the federal states to incur new annual debt of 0.35% of GDP, whereas up until now they have not been allowed to take on new debt. And an infrastructure fund will be created to spend €500 billion over the next 12 years.

Impact on near-term growth

The new measures are not likely to significantly change the outlook for 2025 as it will take time for the spending to filter through the economy. However, for 2026 and 2027, the impact on growth could be significant, potentially adding one percentage point to growth per year over the next two years.

The shift in fiscal policy could also support growth via the confidence channel. Economic expectations have already started to rise following the fiscal stimulus announcement and the recent uptick in the manufacturing purchasing managers’ index (PMI) could signal the sector is turning a corner after several months of stagnation. (The manufacturing PMI is a measure of the prevailing direction of economic trends in manufacturing and is based on a monthly survey of supply chain managers).

There has been much excitement in markets about the prospect of these new spending plans being implemented. We think this excitement is justified, given the years of waiting for such measures, and it should prove to be reflationary.

Supply side reform still needed

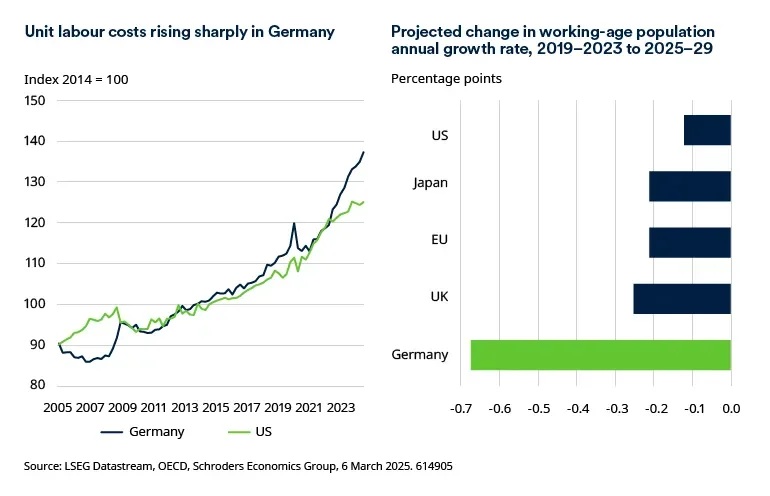

However, even with this enormous stimulus, the German economy still faces significant challenges. The long-term impact on growth will depend heavily on whether the new stimulus includes supply-side reforms to address structural problems.

For growth to be higher in the medium to long term, we need to see the spending be accompanied by a pro-growth agenda. This would incentivise German businesses to invest domestically again, as well as attracting foreign investment.

In particular, Germany needs to address the recent steep rise in unit labour costs. This has been mainly driven by a shrinking working-age population and declining productivity.

Another factor to take into consideration is how quickly the spending will come through. The infrastructure fund is large at €500 billion but this is set to be spent over a 12-year period. Capacity could become a blocker given limited capacity in the infrastructure sector (and in defence). Ramping up demand too quickly could therefore prove inflationary.

Disclosure: Schroders

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account