Risk assets rallied in Q3 on strong corporate earnings and relatively stable U.S. economic growth. The quarter also highlighted various secular trends that could potentially set the stage for long-term earnings growth and share price gains, says the Research Team.

Key takeaways:

- In Q3, the stock market rallied on strong earnings, relatively stable U.S. growth, eased trade fears, and Federal Reserve (Fed) rate cuts.

- Artificial Intelligence (AI) enthusiasm remained a powerful driver of market returns, and we believe the continued AI investment cycle benefits the outlook for companies across multiple sectors, including technology, communication services, energy, and utilities.

- Given lingering U.S. economic uncertainty, we think investors should prioritize companies exposed to secular trends in areas such as AI, commercial aerospace, electrification, digitization, and healthcare innovation.

The stock market rallied in the third quarter on strong corporate earnings and relatively stable U.S. economic growth. Investors moved away from their worst-case fears about U.S. trade policy, which boosted the performance of risk assets.

The Fed started to lower policy rates during the quarter, which may reduce funding costs while providing a tailwind for market sectors such as residential construction. Additionally, we have been encouraged by positive economic news outside of the U.S., especially in Europe, which may offer opportunities for companies with international exposure.

As we look ahead, we will continue to monitor shifting macro and policy currents and their impact on companies.

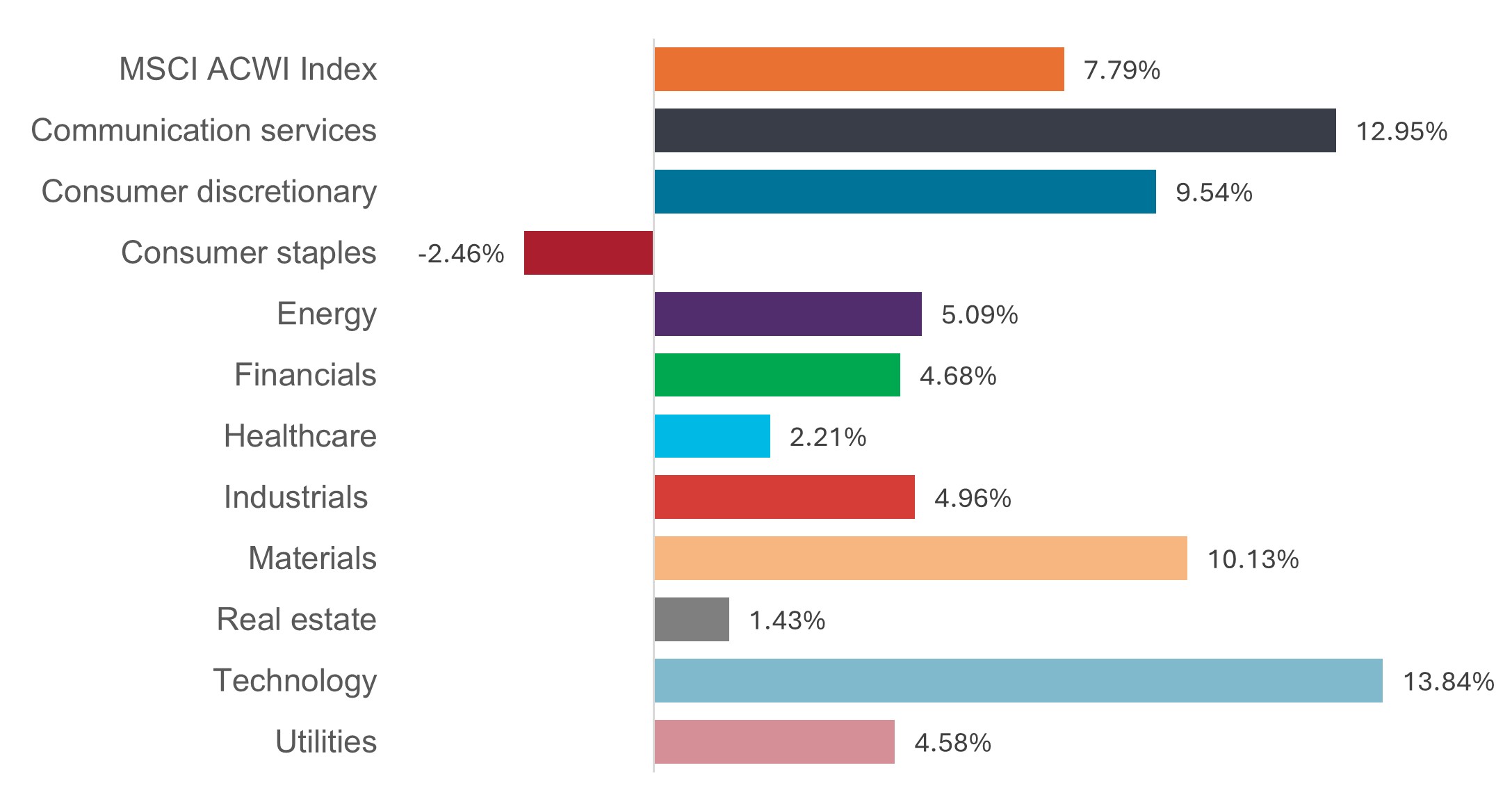

Q3 2025 Global equity performance (total return)

All but one sector performed positively during the quarter, with the technology sector leading the way. Defensive sectors, such as consumer staples, struggled as markets rallied.

Source: Bloomberg, data from to 30 June 2025 to 30 September 2025. Returns are for the MSCI All Country World Index (ACWI) and its 11 sectors. The MSCI ACWI Index captures large- and mid-cap representation across 23 developed markets and 24 emerging markets countries.

Technology: AI remains a powerful source of investment opportunities

Denny Fish and Jonathan Cofsky

What happened: Tech stocks were notable performers in the third quarter as continued strong capital spending on AI provided an earnings tailwind for leading hardware, semiconductor, and semiconductor equipment companies. We also saw increased usage of AI applications, particularly for companies with leading large language models (LLMs). At the same time, investor concerns over an AI-related competitive disruption pressured shares of application software companies.

Looking ahead: The emergence of AI has been a major driver of technology stocks over the past three years, as investors scrambled to gain exposure to this generational opportunity. We see AI as a multi-decade secular trend that has the potential to be more transformative than mobile and cloud.

At the same time, we recognize we could see ebbs and flows in AI capital investment. Industry growth may face bottlenecks, such as the availability of power and the pace of data center development, that could impact how quickly new AI capacity can be added. For this reason, we expect AI demand to far outpace supply.

Additionally, we believe the market has entered the second stage of the AI investment cycle as advancements in LLMs and updated business strategies have enabled investors to better assess the prospects of individual market segments and companies. We expect continued strong growth potential for companies in the AI semiconductor supply and support chains, as well as for hyperscalers and developers of infrastructure software that can help enterprises structure their data for AI.

Energy & Utilities: Powering AI’s expansion

What happened: Energy and Utilities stocks lagged the broader MSCI ACWI Index in the third quarter. However, energy stocks outperformed crude oil prices, which declined on concerns about market oversupply heading into a period of seasonal demand weakness.

Looking ahead: We believe energy companies are well equipped to weather a period of lower prices until supply/demand fundamentals improve. Notably, we believe companies with high-quality, long-duration assets are underappreciated by the market. We expect companies with decades of low-cost investment opportunities to be relative winners through the cycle.

We believe utilities stocks could receive increased attention from investors given the tremendous power requirements of AI. We see no signs that AI-related capital investment or data center buildout is abating, and we believe the AI complex will remain a large consumer of electricity. In our view, this demand, combined with the ongoing electrification of the broader economy, makes a strong case for investing in utilities, especially companies with exposure to unregulated power markets. While regulated utilities have less direct exposure to these trends, we see the potential for multiple expansion for these stocks given the expected strength and duration of the power growth theme.

Communication Services: AI and digital disruption are powerful themes

What happened: The Communication Services sector delivered strong performance in the third quarter, outpacing the broader MSCI ACWI Index. Google parent company Alphabet was a standout performer in the sector as the stock rebounded on reduced fears about disruptions to the Search business and the company’s positioning for an AI future. Netflix was a relative laggard in the quarter following a run of very strong earnings growth and share price gains. Meta Platforms was also a relative underperformer as concerns around its growing capital spending overshadowed strong growth in advertising revenues.

Looking ahead: In the near-term, we will continue to monitor economic fundamentals, such as slowing job growth and the potential inflationary impact of tariffs, which could impact cyclical market segments such as the advertising ecosystem. We remain upbeat on the long-term outlook for the communications services sector. We are especially excited about opportunities around AI, which we believe has the potential to be even more pervasive and value-generating than the market now expects. Within the communication services sector, we anticipate continued consolidation around the largest digitally native platforms that are best equipped to attract both content (supply) and users (demand).

Industrials: Focusing on stable growers and self-help stories

What happened: Industrials stocks extended their strong year-to-date performance but underperformed the broader market in the third quarter. Despite this underperformance, we saw no significant deterioration in company outlooks or fundamentals. Indeed, recent data indicated that industrial activity remained relatively stable despite concerns about tariffs.

Looking ahead: We remain alert for signs of strengthening industrial activity while we monitor developments around tariffs, geopolitical stability, and consumer and business confidence.

While valuation multiples for such companies have seen some expansion, we remain excited about strong revenue growth potential that may flow through to higher margins and profits. Given lingering economic uncertainty, we also favor companies that are making operational improvements or are exposed to unique catalysts that may drive stable profit growth even in uncertain times.

Financials: Cyclical and secular global trends creating opportunities

What happened: Financials stocks participated in the broad third-quarter rally, supported by signs of resilient economic growth and consumer spending. We also saw improved capital markets performance and an increase in initial public offerings.

Looking ahead: In our view, the global financial services sector continues to offer a rich landscape in which to deploy our deep fundamental research. We have continued to see favorable cyclical trends across many areas of the global financial markets. These include relatively low levels of credit losses and delinquencies and attractive pricing for property and casualty insurance. Interest rates also remain well above zero in most major markets.

We are also excited about secular trends such as growth in electronic payments and have seen opportunities for businesses leveraging proprietary data and advanced technologies like AI. Furthermore, we have seen opportunity in several European banks that we believe may benefit from significant capital return, an improved regulatory backdrop, and potential industry consolidation.

Consumer: Bottom-up stock selection remains key to navigating uncertainty

What happened: Consumer discretionary stocks outperformed the broader MSCI ACWI Index in the third quarter. Consumer spending growth remained relatively stable as real wages continued to expand for most households. Against this backdrop, we saw standout share price performance by companies such as home furnishings retailer Wayfair, automotive parts seller O’Reilly Automotive, and discount retailer TJX Companies.

Looking ahead: We have been encouraged by resilient consumer spending, especially among higher income households. At the same time, we remain cautious about slowing employment growth and the potential impact of shifting U.S. trade policies on inflation and consumer budgets. Given these crosscurrents, we are focused on companies with high-quality business models, strong balance sheets, and resilient earnings growth. We have also found opportunities with companies benefiting from secular growth themes such as digitization and AI.

Healthcare: Industry remains committed to innovation

What happened: The healthcare sector has faced an unusual amount of policy uncertainty in 2025, but we saw several positive developments in the third quarter. Drugmakers received greater clarity on tariffs and a steady pace of drug approvals. Biotechnology companies benefited from clinical progress and increased deal activity, including several multibillion-dollar acquisitions.

Looking ahead: We are also excited about a number of developments we could see in coming quarters. In the biotech space, we anticipate a rapid pace of data readouts in major treatment areas, including cancers and neurological diseases, as well as in specialty areas such as myotonic dystrophy and achondroplasia. Above all, we have continued to see a strong industry commitment to innovation

Disclosure: Janus Henderson

The opinions and views expressed are as of the date published and are subject to change without notice. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes and are not an indication of trading intent. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Janus Henderson and is being posted with its permission. The views expressed in this material are solely those of the author and/or Janus Henderson and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account