Stocks were slipping further after yesterday’s significant losses as corporate earnings took center stage and economic data shifted to the back seat. Quarrels in Washington didn’t help either with President Trump sending confrontational messages to Beijing and Fed Chair Powell. The Commander in Chief wants the central bank leader to follow in the footsteps of the ECB, which reduced its key benchmark by 25-bps this morning. The disagreement offers market participants déjà vu similar to the Head of State’s first term, when he would get upset that the institution wouldn’t lower short-term rates. Investors are picking up equities though as illustrated by sector breadth being impressively positive, but a disappointing outlook from United Health Group is weighing on the indices. Investors are also scooping up forecast contracts as well as futures tied to the greenback and crude oil.

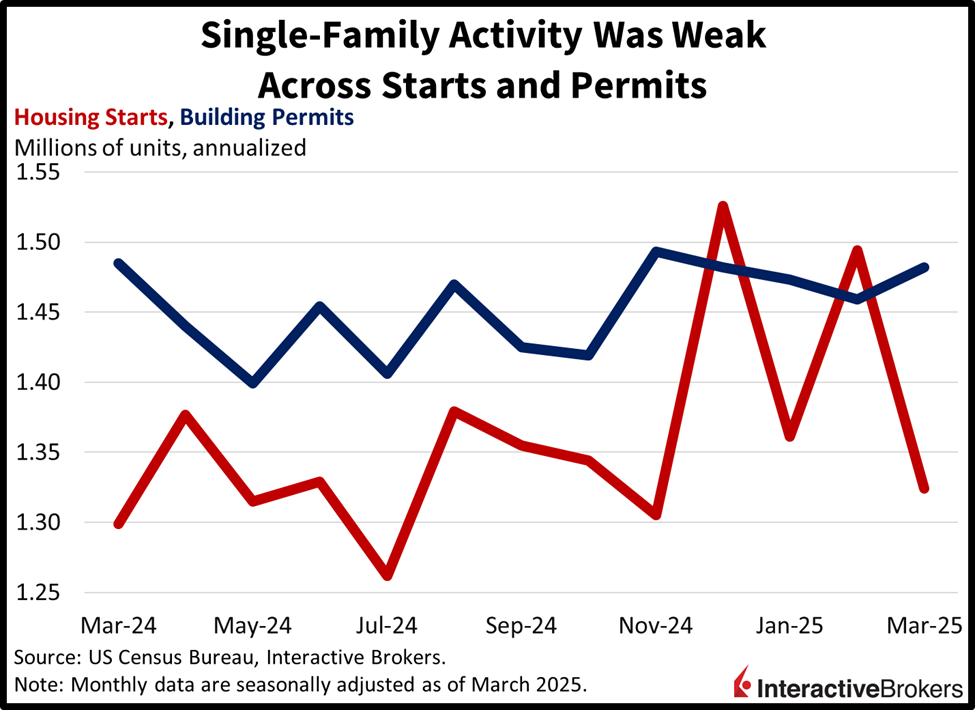

Builders Focus on Rentals Instead of Singles

Weak demand for single-family homes depressed construction activity last month, but permit filings for rental-oriented apartment buildings increased sharply.

The pace of housing starts fell a sharp 11.4% month over month (m/m) to 1.324 million seasonally adjusted annualized units (SAAU) in March, weaker than the 1.42 million median estimate and February’s 1.49 million. It was the weakest result since November. Conversely, permits rose for the first time in four months, rising to 1.482 million SAAU, exceeding expectations of 1.45 million and the previous month’s 1.459 million.

The single-family component was especially disappointing, with its pace of starts falling 14.2% m/m to the lowest level since July of last year while apartment buildings remained unchanged. Similarly, permits featured a 2% drop in single-family houses but a sharp 10.1% jump in apartment buildings. From a regional perspective, sizeable declines in the West and South of 30.9% and 17.1% overwhelmed the 76.2% and 1.4% gains in the smaller Northeast and Midwest areas. Permits were up in three out of four regions with the West, Northeast and South advancing 5.8%, 4.3% and 3% while the Midwest slipped 9.5%.

Past performance is not indicative of future results

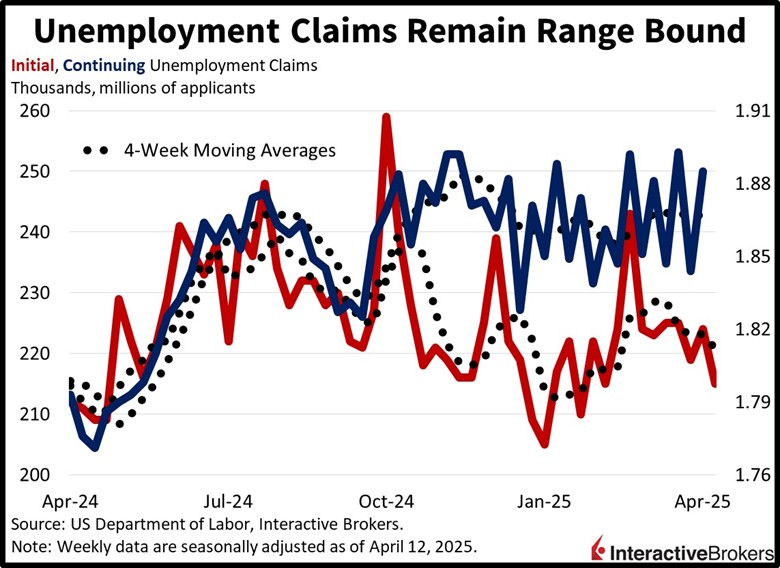

Labor Market Stability Continues

Unemployment claims remained range bound during the last two weeks in another indication of stable labor conditions. Initial claims declined to 215,000 for the week ended April 12, lighter than the median estimate of 225,000 and the prior period’s 224,000. Continuing claims rose, however, to 1.885 million for the week ended April 5, higher than the 1.870 million expected and the previous seven-day interval of 1.844 million. Four-week moving averages also shifted in bifurcated fashion from 223,250 and 1.866 million to 220,750 and 1.867 million.

Past performance is not indicative of future results

Dow Decline Weighs on Sentiment

Markets are bearish as it’s tough for indices to be green when the Dow Jones Industrial is plunging 1.5%. Still the other major domestic benchmarks have made it to positive several times throughout the session so far; however, at the moment, the Russell 2000 is unchanged and the Nasdaq 100 and S&P 500 gauges are each down 0.1%. Treasurys are near their flatlines as the 2- and 10-year maturities change hands at 3.77% and 4.30%. The greenback is catching bids, meanwhile, as traders try to get it back above its pivotal technical level of 100. The US Dollar Index is up 25 basis points (bps) as the domestic currency appreciates relative to most of its major counterparts, including the euro, pound sterling, franc, yen and loonie. It is depreciating versus the yuan and Aussie tender though. Commodity majors are suffering losses except for crude oil, as WTI climbs 1.8% to $63.06 per barrel following Washington adopting a firmer stance against Tehran and seeking to reduce exports of the critical liquid. Elsewhere, silver, gold, copper and lumber are down 1.8%, 1.2%, 0.9% and 0.3%.

An Increasingly Delicate Monetary Policy Balance

Disagreements between central banks and political leaders aren’t unique to President Trump or the United States. Indeed, disputes have occurred many times throughout history and across geographies. For elected officials, sacrificing economic growth and employment strength to tame inflation generally isn’t a desirable path. But the risks of long-term price pressures are especially damaging over time and it’s a major reason why most monetary policy authorities are supposed to be apolitical from a rules standpoint. But pressure from heads of states has had market participants questioning the justification for interest rate moves. In this case, President Trump doesn’t mind short-term inflation while his policies make their way through their economy, but the Fed does, and that’s the root of the conflict. Will Chair Powell say that tariff inflation will be transitory again?

International Roundup

ECB Cuts Key Rate, Points to Economic Shocks

Citing uncertainty regarding the ongoing trade war, the European Central Bank (ECB) trimmed its key interest rate 25 bps to 2.25% this morning, a move that most analysts anticipated. It was the bank’s seventh reduction since June. The ECB also updated its monetary policy description by removing a statement that the key rate is restrictive. In discussing the change, however, ECB President Christine Lagarde said the notion of a neutral rate only applies in a “shock free world.” Bloomberg quoted the chief policymaker as saying that anyone who thinks we are in a shock free world “should have their head examined.’’ She also stated that downside risks to GDP growth have increased.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at the Warnings and Disclosures section of your local Interactive Brokers website.

Disclosure: Bonds

As with all investments, your capital is at risk.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account