21 January 2026 – Greenland’s geopolitical storm

January is turning out to be anything but quiet on the geopolitical front. First came the raid on Venezuela, followed by protests in Iran and renewed concerns about US intervention. Now, a diplomatic crisis over Greenland has erupted, and we’re only two-thirds of the way through the month.

Tariffs, déjà vu?

Yes, trade wars and tariffs are so 2025—but US-Europe tensions over Greenland are spilling over into real world trade. Eight European countries—including two non-EU members, the UK and Norway—are suddenly staring at a new tariff regime: a 10% additional tariff starting February 1 rising to 25% on June 1 unless Denmark agrees to a sale before then.

Markets wobbled on the news, with US and European equities slipping, and both US Treasury yields and gold edging higher. Still, the market reaction has been mild so far, raising the real question: are tariffs really coming imminently? We don’t think so—at least not immediately.

The timeline is simply too tight for any meaningful deal to be negotiated by February 1, making it far more likely that this is a tactic to force negotiations. President Trump is meeting with European leaders at Davos this week, but that’s almost certainly the opening move in the negotiations, not the finale. Any concessions are likely to come in the form of extended deadlines, and not on the tariffs themselves. And looming over all this is the legal question of whether the International Emergency Economic Powers Act can even be lawfully used as the basis for imposing geopolitically motivated tariffs.

What is the real US goal?

Think of Greenland not as a land grab, but as an attempt to renegotiate the terms of an alliance. The US argument—that Denmark and Europe cannot independently defend Greenland—is largely correct but also somewhat beside the point. The US already provides decisive security via NATO coordination, local base infrastructure, and early warning capabilities. What Washington is really after is more control: faster decision-making, fewer political constraints, and veto power in an Arctic region it now sees as a strategic frontline. Defense capacity is the justification; operational autonomy is the goal.

The strategic logic is clear: Russia’s expanding militarization of the Arctic, China’s increasing interest in seeking access, and NATO’s consensus frictions. Danish sovereignty—or Greenland’s self-rule—creates political constraints the US wants eased. This doesn’t necessarily mean annexation is the optimal solution, as that would come with legal, social, and alliance-level downsides. Instead, Washington would likely accept several alternatives short of outright “ownership,” as long as Denmark (and Europe) ultimately concedes broader US economic and military prerogatives.

What scenarios are likely?

Scenario 1: A renegotiated status—not annexation (80% probability)

Negotiations between mismatched powers are never pretty, but they are a geopolitical reality here. Europe may have economic leverage, but the US-European relationship is geopolitically unbalanced because Europe relies heavily on US security guarantees, especially amid the ongoing war in Ukraine.

The US also has a structural advantage: one powerful executive branch leading a unified state versus a patchwork of EU and non-EU states working to overcome coordination challenges. Taken together, in our view, these factors make it likely that some redefined status for Greenland emerges in 2026-2027. The most probable outcome, we believe, is one that nominally preserves Danish sovereignty—perhaps with a slimmer chance Greenland gains independence—but cedes significant economic and military authority to the US.

Scenario 2: Status quo (10-15% probability)

This seems hard to imagine given how aggressively the US President has elevated the issue. Still, 2026 could generate enough competing crises requiring global attention to push Greenland temporarily out of the spotlight. Europe’s underappreciated advantage here is time: the longer negotiations drag on, the greater the chance that other priorities rise to the top—for example, progress on Cuba or Iran. And while the isolationist foreign policy wing of MAGA shapes much of the rhetoric, the vast majority of Trump 2.0 foreign policy decisions have enjoyed the imprimatur of realists, who also happen to be trans-Atlanticists. Any durable shift in Greenland’s status requires their involvement, and they do not see alliance discord as strategically useful in strengthening America’s position in the world.

Scenario 3: Outright annexation—low but not zero (5-10%)

This is a very low probability, though not impossible, scenario. Annexation carries clear downsides: legal complexity, social and governance costs, and a near-guaranteed rupture in trans-Atlantic relations. From Europe’s perspective, it would be catastrophic, effectively dismantling even the facade of collective security. Both sides have strong incentives to avoid this outcome, but it remains a risk if negotiations accidentally veer into miscalculation and someone crosses a red line that becomes difficult to unwind.

Past performance is not indicative of future results.

The risk of a rough ride

While we’re confident about the ultimate direction of travel, we’re less confident that we will get there without damage. The risk of miscalculation feels higher than during last year’s trade talks, despite the similarities. The US president is emboldened by a string of foreign policy wins and is increasingly mindful of his legacy—and territorial expansion would be a dramatic one.

Trump’s success in extracting concessions from Europe last year may encourage him to press for another favorable deal. But European attitudes have hardened too. Running down the clock on Trump and his administration will remain Europe’s go-to strategy, yet pressure is growing to avoid anything that looks like appeasement. All together, it creates real potential to stumble into a trade war.

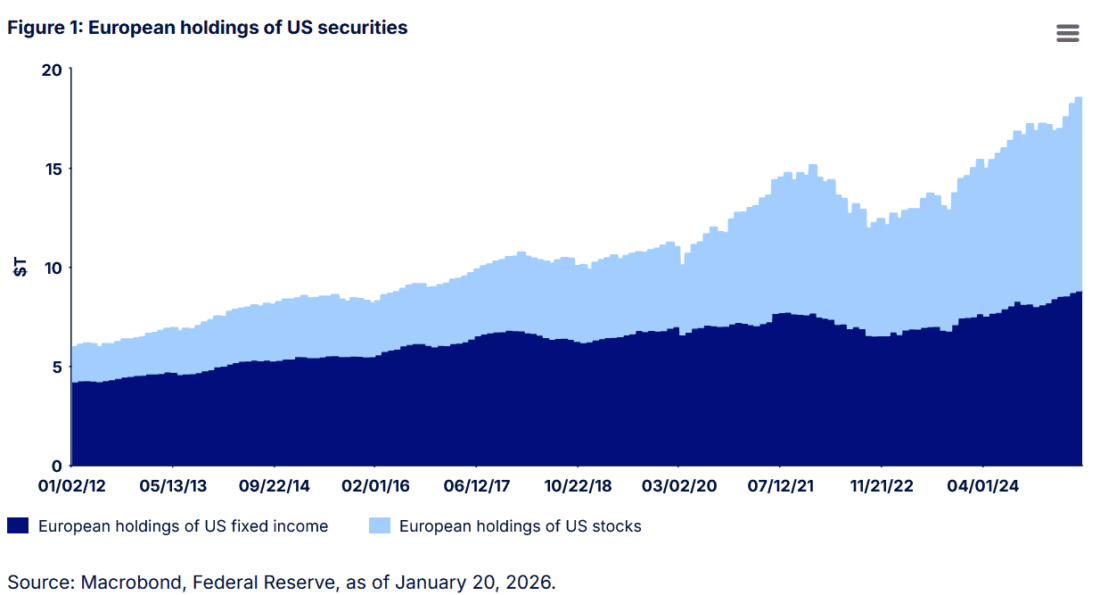

In such a trade war, financial markets may not just absorb damage—they could become Europe’s primary weapon. Europe collectively owns nearly $20 trillion in US financial assets, so sizable capital reallocation would move markets (Figure 1). The White Houses closely watches US market performance, factoring it into its decision-making calculus. Consumer confidence and spending buoy the US economy, much of it on the back of the wealth effect from high stock market returns. As a result, targeting US financial markets may well be the EU’s most potent form of leverage.

Another pathway would be the idea behind the “anti-coercion” tool under consideration in Brussels, which could hit US services exports and intellectual property—in other words, the earnings engine that drives US stock market strength.

What it means for markets and investors

- Gold: The market’s reaction has been negative but relatively muted so far. Looking ahead, any escalation in tensions would naturally support gold given its role as the go-to haven for geopolitical risks

- EURUSD: More counter-intuitively, escalating tensions could also be positive for EURUSD. A “sell America” signal from Europe, combined with already low hedge ratios among European investors and the US dollar’s (USD’s) sensitivity to shifts in global equity sentiment—creates room for near-term Euro strength

- European bonds: Rising tensions could also likely push long-term European bond yields higher as larger fiscal deficits would need to be priced in, implying steeper curves for most European government bonds

- European equity market: Escalation could be broadly bearish for European exporters, especially those heavily exposed to US demand, which constitutes a large share of Europe’s equity market. Notably, as an exception, rising tensions would be a positive signal for European defense stocks, which stand to benefit from any widening trans-Atlantic rift and the associated rise in fiscal spending

- Global equities: And if the EU activates its anti-coercion instrument, signaling willingness to expand the trade war beyond the goods trade, that could be strong bearish signal for global equities across the board

The most likely outcome to all this, in our view, is a negotiated reset that expands US influence without breaking formal sovereignty. But the path to get there will be a bumpy one, and it’s fraught with real geopolitical and market risk. Missteps are possible, and the growing use of financial markets as leverage suggests the next moves will matter well beyond the Arctic.

To help you stay ahead of the geopolitical curve, don’t miss our latest macroeconomic insights.

Disclosure: State Street Global Advisors

Do not reproduce or reprint without the written permission of SSGA.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

State Street Global Advisors and its affiliates (“SSGA”) have not taken into consideration the circumstances of any particular investor in producing this material and are not making an investment recommendation or acting in fiduciary capacity in connection with the provision of the information contained herein.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

COPYRIGHT AND OTHER RIGHTS

Other third party content is the intellectual property of the respective third party and all rights are reserved to them. All rights reserved. No organization or individual is permitted to reproduce, distribute or otherwise use the statistics and information in this report without the written agreement of the copyright owners.

Definition:

Arbitrage: the simultaneous buying and selling of securities, currency, or commodities in different markets or in derivative forms in order to take advantage of differing prices for the same asset.

Fund Objectives:

SPY: The investment seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500® Index. The Trust seeks to achieve its investment objective by holding a portfolio of the common stocks that are included in the index (the “Portfolio”), with the weight of each stock in the Portfolio substantially corresponding to the weight of such stock in the index.

VOO: The investment seeks to track the performance of a benchmark index that measures the investment return of large-capitalization stocks. The fund employs an indexing investment approach designed to track the performance of the Standard & Poor’s 500 Index, a widely recognized benchmark of U.S. stock market performance that is dominated by the stocks of large U.S. companies. The advisor attempts to replicate the target index by investing all, or substantially all, of its assets in the stocks that make up the index, holding each stock in approximately the same proportion as its weighting in the index.

IVV: The investment seeks to track the investment results of the S&P 500 (the “underlying index”), which measures the performance of the large-capitalization sector of the U.S. equity market. The fund generally invests at least 90% of its assets in securities of the underlying index and in depositary receipts representing securities of the underlying index. It may invest the remainder of its assets in certain futures, options and swap contracts, cash and cash equivalents, as well as in securities not included in the underlying index, but which the advisor believes will help the fund track the underlying index.

The funds presented herein have different investment objectives, costs and expenses. Each fund is managed by a different investment firm, and the performance of each fund will necessarily depend on the ability of their respective managers to select portfolio investments. These differences, among others, may result in significant disparity in the funds’ portfolio assets and performance. For further information on the funds, please review their respective prospectuses.

Entity Disclosures:

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

SSGA Funds Management, Inc. serves as the investment advisor to the SPDR ETFs that are registered with the United States Securities and Exchange Commission under the Investment Company Act of 1940. SSGA Funds Management, Inc. is an affiliate of State Street Global Advisors Limited.

Intellectual Property Disclosures:

Standard & Poor’s®, S&P® and SPDR® are registered trademarks of Standard & Poor’s® Financial Services LLC (S&P); Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones); and these trademarks have been licensed for use by S&P Dow Jones Indices LLC (SPDJI) and sublicensed for certain purposes by State Street Corporation. State Street Corporation’s financial products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates and third party licensors and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability in relation thereto, including for any errors, omissions, or interruptions of any index.

BLOOMBERG®, a trademark and service mark of Bloomberg Finance, L.P. and its affiliates, and BARCLAYS®, a trademark and service mark of Barclays Bank Plc., have each been licensed for use in connection with the listing and trading of the SPDR Bloomberg Barclays ETFs.

Distributor: State Street Global Advisors Funds Distributors, LLC, member FINRA, SIPC, an indirect wholly owned subsidiary of State Street Corporation. References to State Street may include State Street Corporation and its affiliates. Certain State Street affiliates provide services and receive fees from the SPDR ETFs.

ALPS Distributors, Inc., member FINRA, is distributor for SPDR® S&P 500®, SPDR® S&P MidCap 400® and SPDR® Dow Jones Industrial Average, all unit investment trusts. ALPS Distributors, Inc. is not affiliated with State Street Global Advisors Funds Distributors, LLC.

Before investing, consider the funds’ investment objectives, risks, charges, and expenses. For SPDR funds, you may obtain a prospectus or summary prospectus containing this and other information by calling 1‐866‐787‐2257 or visiting www.spdrs.com. Please read the prospectus carefully before investing.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from State Street Global Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or State Street Global Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Precious Metals

Precious metals may not be available in all locations, please check your local IBKR website for availability.

Disclosure: Bonds

As with all investments, your capital is at risk.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account