Originally Posted 27 October 2025 – Monthly Cash Review – GBP

GBP INVESTMENT UPDATE – SEPTEMBER 2025

The Bank of England (BoE) Monetary Policy Committee (MPC) voted by 7-2 to maintain the base rate at 4.00% at the 18 September meeting, an outcome that was widely expected.

Economic Data

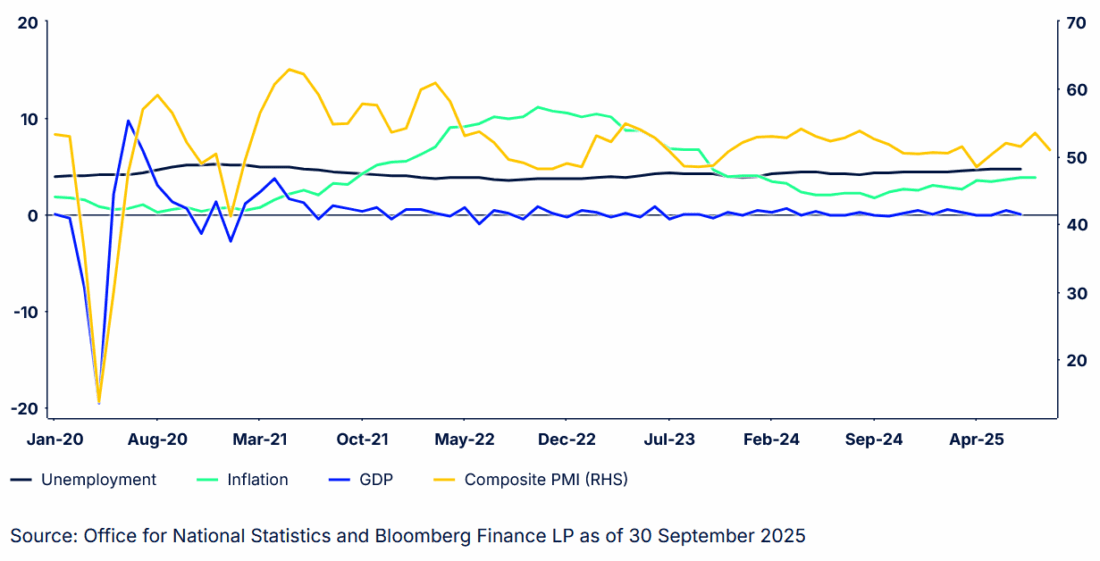

- Headline inflation for August remained steady at 3.8%, while the core inflation eased from 3.8% to 3.6%, both of which were in line with consensus expectations. Services inflation dipped from 5.0% to 4.7%, marginally below the BoE’s forecast of 4.8%. The declines in core and services inflation were mainly due to a drop in airfares inflation. Food inflation rose again, up from 4.9% to an 18-month high of 5.1%.

- GDP for July was flat, in line with consensus expectations, following month-on-month growth of 0.4% in June.

- The S&P Global composite purchasing managers’ index (PMI) fell from 53.5 in August to 51.0 in September, lower than consensus expectations of 53.0—readings above the 50 level are indicative of growing economic activity. The services PMI fell from 54.2 to 51.9 and the manufacturing PMI output balance slumped from 49.3 to 45.4. The employment PMI remained broadly unchanged at 46.6.

- The unemployment rate for July remained stable at 4.7%. Private sector regular pay growth eased from 4.8% to 4.7%, keeping it on track to meet the BoE’s forecast of 4.6% for September.

Markets

Policy guidance from the BoE was essentially unaltered with the statement retaining text that “a gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate”. The BoE view was that the flow of data since August contained “limited economic news”. It was noted in the minutes that there appeared to be “less of an immediate risk that the labour market would loosen very rapidly” while “upside risks around medium-term inflationary pressures remain prominent in the Committee’s assessment of the outlook”. There is a concern that the recent rise in inflation could feed into wages. The committee retained language that policy is not on a “pre-set path” and will remain “responsive to the accumulation of evidence”, aiming to retain maximum optionality—this means that decisions will be data dependent on a meeting-to-meeting basis. BoE Governor Andrew Bailey stated that he continues “to think that there will be some further reductions, but the timing and scale of those is more uncertain”. In addition, the MPC voted to slow the pace of its QT programme from £100bn to £70bn, which was a smaller reduction than the consensus forecast.

On the economic data front, headline inflation has rebounded significantly from 1.7% in September 2024 due to rises in utilities, fuel, and food inflation, as well as some one-off jumps in water bills and vehicle excise duties. It is expected to peak in September before dropping back. GDP data continues to reflect an economy that is still struggling to gain momentum from the drag of previous hikes in taxes and the possibility of more to come in the Autumn Budget. September’s flash PMI reports suggest that the downside risks around economic activity may be growing. The unemployment rate has risen as businesses continue to reduce headcount to counter the April rises in the National Insurance Contributions for employers and the minimum wage.

The Autumn Budget is scheduled for 26 November and there is much speculation around what the final outcome will look like. Policy U-turns around welfare and winter fuel cuts, rising gilt yields, and increased public sector borrowing increase the risk of a larger hole in the public finances and raises questions around this will be financed. The new youth employment scheme announced at the Labour party conference and the elimination of the two-child cap on child benefit, will require financing at a future stage. There is an expectation is that circa £30bn of fiscal tightening is required in the upcoming budget, with Chancellor Rachel Reeves expected to raise taxes. The question then shifts to how this will be implemented. The prospect of larger tax rises than previously assumed will likely dampen activity in the near term.

The recent pickup in headline inflation and the expectation of a further increase in September is likely to keep the BoE on hold. Market implied rates (Figure 1) for October finished the month at 3.95%, meaning the market expects the base rate to remain at 4.00%. The implied rate for December ended September at 3.91%, suggesting diminishing expectations for a rate cut before the end of 2025.

Figure 1: Market Implied Interest Rate Expectations

Past performance does not guarantee future results.

Fund

Following the September BoE meeting, market pricing remains unchanged with no further interest rate cuts expected for 2025. Gilt yields remain elevated ahead of the November budget and given the uncertainty around what the budget could contain, fund investments were shortened to reduce fund weighted average maturity (WAM) and higher liquidity levels were maintained to provide additional flexibility against any potential market volatility. The fund took advantage of high-yielding, short-dated issuance from sovereigns, supranationals, and agencies, along with rising overnight gilt repo yields. Fund liquidity requirements, both overnight and weekly, remained well in excess of minimum requirements at all times. Fund liquidity was covered with a combination of government and supranational holdings, gilt repo and bank deposits. The fund credit rating exceeded requirements at all times.

Figure 2: A Snapshot of UK Economic Data

Past performance does not guarantee future results.

Disclosure: State Street Global Advisors

Do not reproduce or reprint without the written permission of SSGA.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

State Street Global Advisors and its affiliates (“SSGA”) have not taken into consideration the circumstances of any particular investor in producing this material and are not making an investment recommendation or acting in fiduciary capacity in connection with the provision of the information contained herein.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Investing involves risk including the risk of loss of principal.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer.

COPYRIGHT AND OTHER RIGHTS

Other third party content is the intellectual property of the respective third party and all rights are reserved to them. All rights reserved. No organization or individual is permitted to reproduce, distribute or otherwise use the statistics and information in this report without the written agreement of the copyright owners.

Definition:

Arbitrage: the simultaneous buying and selling of securities, currency, or commodities in different markets or in derivative forms in order to take advantage of differing prices for the same asset.

Fund Objectives:

SPY: The investment seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500® Index. The Trust seeks to achieve its investment objective by holding a portfolio of the common stocks that are included in the index (the “Portfolio”), with the weight of each stock in the Portfolio substantially corresponding to the weight of such stock in the index.

VOO: The investment seeks to track the performance of a benchmark index that measures the investment return of large-capitalization stocks. The fund employs an indexing investment approach designed to track the performance of the Standard & Poor’s 500 Index, a widely recognized benchmark of U.S. stock market performance that is dominated by the stocks of large U.S. companies. The advisor attempts to replicate the target index by investing all, or substantially all, of its assets in the stocks that make up the index, holding each stock in approximately the same proportion as its weighting in the index.

IVV: The investment seeks to track the investment results of the S&P 500 (the “underlying index”), which measures the performance of the large-capitalization sector of the U.S. equity market. The fund generally invests at least 90% of its assets in securities of the underlying index and in depositary receipts representing securities of the underlying index. It may invest the remainder of its assets in certain futures, options and swap contracts, cash and cash equivalents, as well as in securities not included in the underlying index, but which the advisor believes will help the fund track the underlying index.

The funds presented herein have different investment objectives, costs and expenses. Each fund is managed by a different investment firm, and the performance of each fund will necessarily depend on the ability of their respective managers to select portfolio investments. These differences, among others, may result in significant disparity in the funds’ portfolio assets and performance. For further information on the funds, please review their respective prospectuses.

Entity Disclosures:

The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

SSGA Funds Management, Inc. serves as the investment advisor to the SPDR ETFs that are registered with the United States Securities and Exchange Commission under the Investment Company Act of 1940. SSGA Funds Management, Inc. is an affiliate of State Street Global Advisors Limited.

Intellectual Property Disclosures:

Standard & Poor’s®, S&P® and SPDR® are registered trademarks of Standard & Poor’s® Financial Services LLC (S&P); Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones); and these trademarks have been licensed for use by S&P Dow Jones Indices LLC (SPDJI) and sublicensed for certain purposes by State Street Corporation. State Street Corporation’s financial products are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates and third party licensors and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability in relation thereto, including for any errors, omissions, or interruptions of any index.

BLOOMBERG®, a trademark and service mark of Bloomberg Finance, L.P. and its affiliates, and BARCLAYS®, a trademark and service mark of Barclays Bank Plc., have each been licensed for use in connection with the listing and trading of the SPDR Bloomberg Barclays ETFs.

Distributor: State Street Global Advisors Funds Distributors, LLC, member FINRA, SIPC, an indirect wholly owned subsidiary of State Street Corporation. References to State Street may include State Street Corporation and its affiliates. Certain State Street affiliates provide services and receive fees from the SPDR ETFs.

ALPS Distributors, Inc., member FINRA, is distributor for SPDR® S&P 500®, SPDR® S&P MidCap 400® and SPDR® Dow Jones Industrial Average, all unit investment trusts. ALPS Distributors, Inc. is not affiliated with State Street Global Advisors Funds Distributors, LLC.

Before investing, consider the funds’ investment objectives, risks, charges, and expenses. For SPDR funds, you may obtain a prospectus or summary prospectus containing this and other information by calling 1‐866‐787‐2257 or visiting www.spdrs.com. Please read the prospectus carefully before investing.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from State Street Global Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or State Street Global Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account