Originally Posted, 5 September 2024 – Monthly markets review – August 2024

A look back at markets in August when shares experienced extreme volatility at the start of the month.

The month in summary:

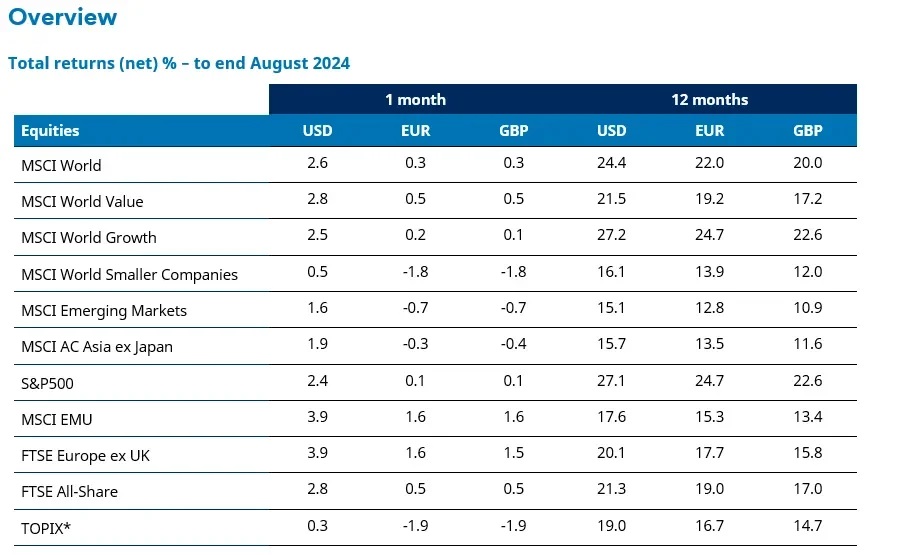

Global equities gained in August but the month began on a volatile note. In particular, shares in Japan suffered steep falls early in the month.

Please note any past performance mentioned is not a guide to future performance and may not be repeated. The sectors, securities, regions, and countries shown are for illustrative purposes only and are not to be considered a recommendation to buy or sell.

US

US shares ended higher in August but the month began with extreme market volatility and some sharp stock market falls. These occurred as investors reacted to weak US economic data and priced in several interest rate cuts by the end of the year. However, data later in the month provided some reassurance, as did some resilient corporate earnings.

The market volatility was in part sparked by weak US jobs data. The non-farm payrolls report showed that 114,000 jobs were added in July, well below the consensus expectation of 175,000. The unemployment rate rose to 4.3%. Meanwhile, the July ISM manufacturing report indicated further contraction in manufacturing activity, with a reading of 46.8, down from 48.5 in June.

Following the weaker economic data, investors grew worried that the US Federal Reserve (Fed) may have left it too late to cut interest rates, raising the risk of a “hard landing” or recession for the economy. However, data released later in the month proved more reassuring. US retail sales rose by 1% in July, well above expectations of a 0.3% increase.

The stock market volatility abated and investors looked ahead to a speech by Fed chair Jerome Powell at the Jackson Hole central bank symposium towards the end of August. He indicated that the US labour market has indeed cooled but that the pace of rate cuts would depend on incoming data. This was interpreted as leaving the door open for a 50 basis point rate cut in September.

The S&P 500 ended the month higher with consumer staples, real estate and healthcare among the top performing sectors. Energy and consumer discretionary registered negative returns.

Eurozone

Eurozone shares gained in August. Real estate and communication services were among the strongest performing sectors while energy and information technology lagged. Expectations of further interest rate cuts helped to boost rate-sensitive sectors such as real estate.

Data showed that annual inflation in the eurozone was estimated at 2.2% in July, down from 2.6% in August. The drop in inflation towards the European Central Bank’s 2% target was perceived to make it more likely that the ECB would cut rates at the September meeting, following a 25 bps cut in July.

Meanwhile, the flash eurozone purchasing managers’ index (PMI) ticked up to 51.2 in August, from 50.2 in July. The expansion was supported by the services sector, while the manufacturing reading remained below 50. The service sector was boosted by the staging of the Olympic Games in Paris. PMI data is based on surveys of companies in the manufacturing and service sectors. A reading above 50 indicates growth while below 50 indicates contraction.

UK

UK equities rose over the month. The healthcare, consumer staples and industrials sectors were the top contributors over the period. Energy, basic materials and financials detracted the most.

UK Prime Minister (PM) Keir Starmer warned of a “painful” autumn budget. He signalled potential tax increases and spending cuts due to an estimated £22 billion shortfall in public finances. The PM added those with the “broadest shoulders” will bear the heaviest burden, sparking speculation around which taxes might be raised.

The Bank of England’s (BoE) Monetary Policy Committee (MPC) made its first rate cut in four years, reducing the Bank Rate by 25 basis points to 5.00%. However, there was caution around further reductions which drove sterling higher against the dollar and euro.

BoE Governor Andrew Bailey said the MPC would move ahead cautiously, while Deputy Governor Clare Lombardelli added that the BoE’s base case for inflation is benign, but risks remain of an “alternative world” in which inflation moves higher again.

It was revealed inflation ticked up slightly to 2.2% year-on-year in July. Meanwhile, the first second quarter estimate of GDP growth showed that output expanded by 0.6% quarter-on-quarter (q/q), only a touch slower than the 0.7% q/q increase achieved in the first quarter.

Japan

The volatility of the Japanese equity market increased amid a sharp sell-off in the early part of the month. However, investor sentiment sharply improved towards the end of the month. The market ended August with a moderate decline of -2.9% for the TOPIX Total Return in yen terms. The market turbulence was associated with a sharp movement in the yen, which appreciated over the course of the month.

On 5 August, the Nikkei 225 stock market index recorded its largest decline in history in terms of index points. This decline surpassed the magnitude of the Black Monday crash in 1987. In percentage terms, the 12.4% drop was the second-largest single-day decline on record. The market sharply rebounded (+10.2%) on the following day, 6 August.

Despite the market turbulence, corporate earnings and macroeconomic figures showed solid progress. The April to June quarterly earnings were better than expected on aggregate. Real wage growth (which takes inflation into account) finally turned positive, although this was partially influenced by one-off bonus payments.

Japanese GDP growth also provided evidence of solid economic growth, supported by domestic demand, with an expansion of 0.8% q/q for the second quarter. The Bank of Japan adjusted its message to a more moderate tone, while the Fed indicated its intention to cut interest rates in September. These developments supported investor sentiment in both the Japanese and US stock markets.

The news of Prime Minister Kishida’s decision not to run for the presidential election for the LDP, the ruling party, did not have a material effect on the equity market. This is because there will not be a significant shift in economic policies by the new prime minister, who will be determined at the end of September.

Asia (ex Japan)

Asia ex Japan equities gained in August. The Philippines, Indonesia and Malaysia were the best-performing markets in the MSCI AC Asia ex Japan Index. South Korea, India and China were the worst-performing markets in the index. South Korea was the only market to end the month in negative territory, as technology stocks gave up some of their recent gains. Shares in Taiwan achieved modest gains. Taiwan remains the best-performing index market in the year-to-date period.

Share price growth in China was muted in August as the country’s slow recovery from the Covid-19 pandemic and the ongoing real estate crisis continued to weigh on sentiment, with many investors remaining on the sidelines as they wait for stronger fiscal support from the Chinese government.

Hong Kong stocks performed well in the month, with hopes that the US Fed will start cutting interest rates in September helping to boost investor sentiment. However, Hong Kong is the weakest performer in the index in the year-to-date period, with a negative overall return.

Emerging markets

Following sharp declines at the start of the month on the back of US recession fears and a Bank of Japan interest rate hike, emerging market (EM) equities recovered to finish August in positive territory, albeit behind developed market peers. Dovish comments from Fed Chair Jerome Powell at the annual Jackson Hole summit later in the month were helpful for EM returns, as was a weaker US dollar.

Some of the smaller Asian emerging markets were the top performers in the month, including the Philippines, Indonesia, Malaysia and Thailand, all of which were boosted by local currency appreciation against the US dollar. Brazil’s outperformance was also helped by local currency strength. In South Africa, the rand rallied too, and better inflation data prompted optimism about the potential for interest rate cuts in the coming months. The Taiwan market recovered following July’s global sell-off of technology-related stocks.

Index heavyweights India and China both posted positive returns but lagged the EM index, with the latter negatively affected by softer economic activity data releases. Korea fell in US dollar terms with some memory-related technology stocks particularly hard hit.

Meanwhile, peso weakness weighed on equity market returns in Mexico, raising concerns about potential inflationary pressure in the months ahead. The central bank also cut its policy rate by 25bps to 10.75%. Turkey posted the biggest losses in US dollars among its EM peers given local currency depreciation, some weaker-than-expected Q2 earnings results and ongoing foreign equity outflows.

Global bonds

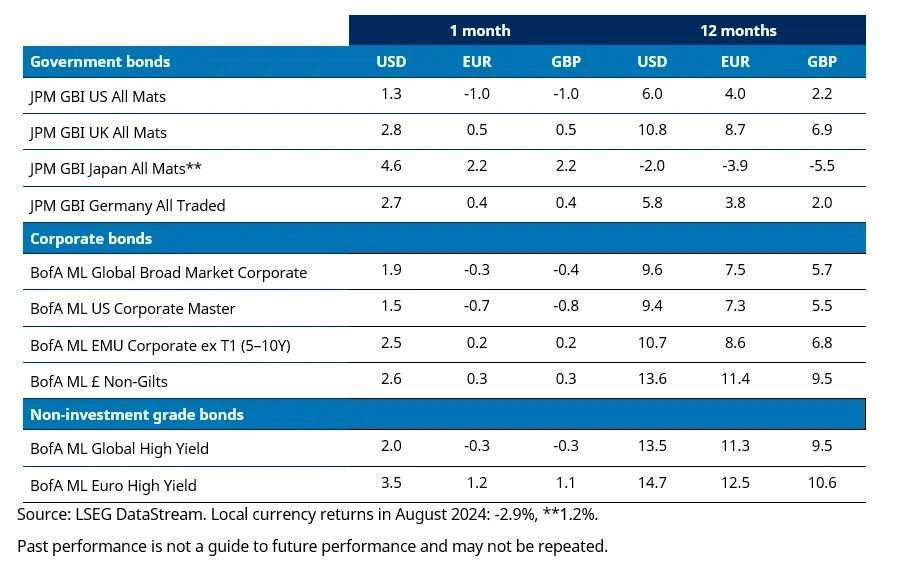

August was a volatile, but broadly positive, month for fixed income. US markets outperformed those in other major economies as investors focused on the imminent start of interest rate cuts from the US Fed amid increasing concerns about weakness in the US economy. Corporate bonds outperformed, again led by the US, with high yield returns ahead of those for investment grade. High yield bonds are more speculative than their investment grade counterparts, with a credit rating below investment grade.

Following the Fed’s meeting on the last day of July, chair Jerome Powell gave markets a steer that the mid-September meeting would deliver the first interest rate cut of the cycle. That guidance was followed by a decline in leading manufacturing indicators globally and a weaker-than-expected non-farm payrolls figure at the start of August. The combination sent US Treasury yields plunging (meaning prices rose), the VIX index (a measure of market volatility) spiking to levels last seen during 2020, and the market pricing 125bps of US interest rate cuts by early 2025.

This reaction in markets was partly reversed in the first two weeks of August. However, US Treasury yields continued to move lower again though the second half of the month, reflecting softer inflation figures, weak housing data, and dovish Fed comments focused on the downside risks to employment. Powell’s Jackson Hole speech on 23 August noted “ample room to respond to any risks” and was again widely interpreted as signalling the Fed’s intention to cut rates in September. The US yield curve steepened over the month as yields on shorter maturity bonds fell by more than those at the long end.

Other major government bond markets saw more modest gains. European data – in particular, weak manufacturing PMIs – continued to point towards a downturn in the eurozone economy and its potential vulnerability to shocks. Interest rate expectations consequently moved lower, with a further 25bps cut from the ECB fully priced in for September.

In the UK, the Bank of England cut interest rates on 1 August. A decline in the unemployment rate, a rise in job vacancies, and further improvements in PMI survey data suggest that the UK is now in a growth recovery phase. Market expectations currently point to three interest rate cuts in the UK over the next six months, with the first of these likely to happen only in November.

Credit markets recovered from their sharp sell-off at the start of August to outperform government bonds over the month. Corporate bonds performed better in the US (supported by a focus on materially lower interest rates in the US) than in Europe (given more signs of a weakening European economy). High yield corporate bonds generally outperformed investment grade, again led by the US.

Currency markets also reflected expectations of more substantial interest rate cuts in the US than elsewhere, with the US dollar weakening significantly against other major currencies.

Convertible bonds protected investors in the early August market falls. However, in the subsequent rally, equities overtook convertibles. At the end of what was a positive month for equities, convertibles once more had a participation in the upside that was well below average. The FTSE Global Focus index, hedged in US dollars, ended the month with a gain of 0.9%.

Commodities

The S&P GSCI Index registered a modest decline in August. Energy and livestock were the weakest components of the index, while agriculture, industrial metals and precious metals achieved modest price gains. Within energy, all sub-components ended the month in negative territory.

In agriculture, coffee and cocoa both achieved strong price gains. In industrial metals, the price of zinc and aluminium were sharply higher, while gains for copper and nickel were more muted. The price of lead was modestly lower. In precious metals, gold prices rose, while silver fell back slightly.

Past performance is not indicative of future results

Past performance is not indicative of future results

Disclosure: Schroders

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Bonds

As with all investments, your capital is at risk.

Disclosure: Mutual Funds

Not all funds are available to retail investors. Mutual Funds are investments that pool the funds of investors to purchase a range of securities to meet specified objectives, such as growth, income or both. Investors are reminded to consider the various objectives, fees, and other risks associated with investing in Mutual Funds. Please read the prospectus accordingly. This communication is not to be construed as a recommendation, solicitation or promotion of any specific fund, or family of funds. Interactive Brokers may receive compensation from fund companies in connection with purchases and holdings of mutual fund shares. Such compensation is paid out of the funds' assets. However, IBKR does not solicit you to invest in specific funds and does not recommend specific funds or any other products to you. For additional information please visit the Mutual Funds section of your local Interactive Brokers website.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account