Tech stocks are getting slammed despite Samsung posting a blockbuster earnings report that signaled unwavering appetites for memory chips deemed essential for the AI buildout. But elevated prices for those semiconductors have investors worried about the sustainability of the purchasing momentum, as firms have been pulling all kinds of levers to raise the significant dollars necessary to fund these massive technological initiatives. Debt deals, initial and secondary equity offerings and free cash flow drawdowns are some of the strategies being used to capitalize the expenditure plans which carry uncertain return prospects. Meanwhile, Wall Street sentiment is additionally deteriorating due to heightening geopolitical tensions, after several tankers experienced attacks in the Strait of Hormuz, resulting in an adverse lift in energy costs. The jumps in crude oil and natural gas, while modest, are raising inflation expectations and driving rates and the greenback north as the yield curve ascends in bear-steepening fashion led by duration. Furthermore, rebounding fuel charges have the 10- and 30-year Treasuries trading above pivotal resistance levels of 4.50% and 5%. Still, 7 of the 11 major equity sectors are advancing amidst strong interest in defensive names. The positive cyclical outlook is also supported by this morning’s weekly ADP-print depicting steady, albeit slowing hiring, helping to briefly send the Dow Jones Industrial Average to a fresh record. Elsewhere, precious metals are suffering losses, and greater hedging demand has volatility protection instruments seeing heavier premiums.

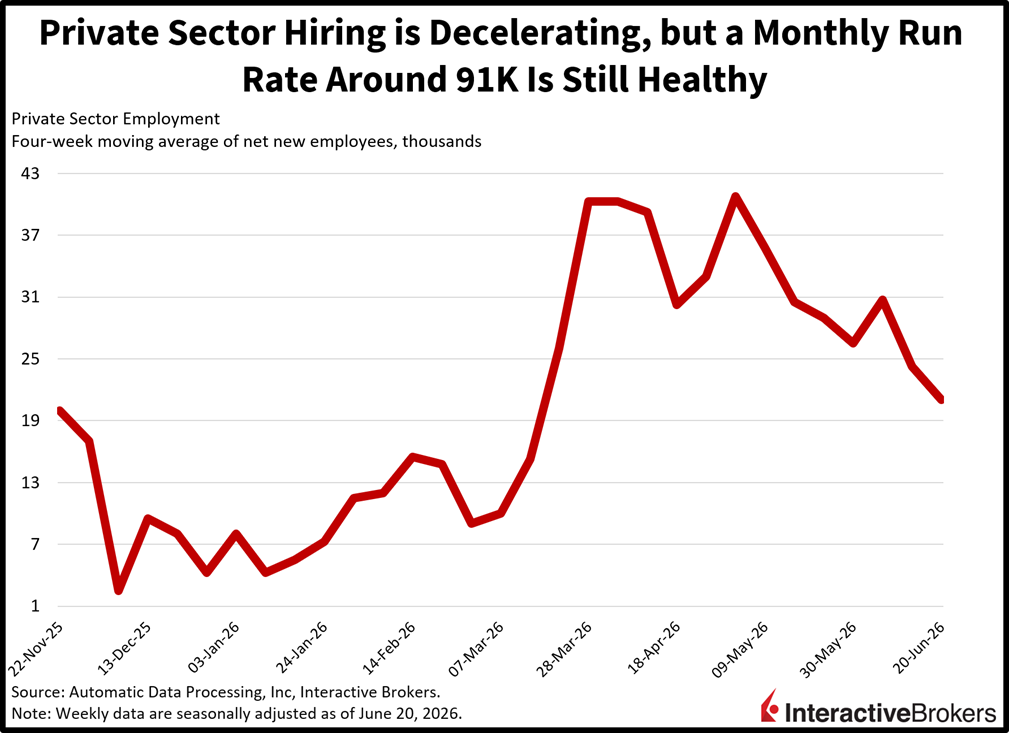

Private-Sector Hiring Slows

Private sector hiring decelerated at the beginning of the summer as worker supply constraints related to subdued labor force participation and restrictive immigration adversely affected payroll expansions. Firms added an average of 21k employees in each of the four weeks during the period that ended June 20, slowing for the second consecutive week and from 24.25k in the prior print, according to ADP. Still, the headline number indicates a monthly run rate of around 91k, which is still strong and points to muted unemployment and ongoing economic momentum. However, if the monthly pace falls below 65k, then risks of deteriorating labor conditions and weakening cyclical health rise materially.

Past performance is not indicative of future results.

Modest Oil Lift Isn’t a Huge Deal, But Climbing Yields Are

Today’s modest increase in crude oil costs isn’t likely to become a longer-term problem as appetites for heightened military aggression remain muted for both Washington and Tehran. Emblematic of the subdued geopolitical risk is the West Texas Intermediate benchmark climbing to just over $70 per barrel, less than $4 north of the July trough that was near $67. But yields are increasingly sensitive to upticks in inflationary uncertainties, as new Fed Chair Kevin Warsh is highly attentive to any impulse that could prolong the central bank’s journey to its 2% target. This responsiveness is certainly warranted, considering that price pressures peaked at 4.2% in May and are currently running at around 3.7%, a number that is far too elevated; however, the rapid 0.5% deceleration that resulted from plunging fuel charges, slowing rents and anemic residential valuation expansions. There are still reasons to be cautious about fixed-income though, as tariff-related charge increases, a rebound in gasoline and/or ongoing buoyant consumer demand keep the headline ahead of 3%, a low bar at this juncture although it’s 50% above the institution’s objective.

International Roundup

Household Spending in Japan Exceeds Estimates

Household spending in Japan climbed 3.7% month over month (m/m) in May but was 0.4% lower than in the year-ago period, according to the Statistics Bureau of Japan. The m/m result accelerated from 1.6% in April and exceeded the 1.4% expected by a consensus of economists. Spending relative to the year-ago period, furthermore, was better than the estimate of a 2.5% drop and April’s 0.5% contraction.

For the year-over-year (y/y) metric, transportation and communications spending slipped 15.8%. The fuel, light and water charges group and the category of culture and recreation, furthermore, sank 7.6% and 3.1%. Categories that experienced increased sales and the extent of the changes were as follows:

- Furniture and household utensils, 23%

- Education, 21.7%

- Clothing and footwear, 4%

- Medical care, 3.3%

- Food, 2.4%

- Housing, 0.7%

But Wage Growth Trails Expectations

Overall wage income in Japan grew 3.2% y/y in May on a nominal basis, missing the economist consensus estimate of 3.4% and slowing from 3.6% in the preceding month. On a real basis, or after inflation, wages were 1.4% higher following April’s 2% gain. Also in May, overtime pay was up 2.9% y/y, a smaller jump than 4.8% in April.

Japan Leading Index Hits Five-Year High

Japan’s Leading Index rose from 116.1 in April to 116.8 in May, which narrowly missed the economist consensus estimate of 116.9 but nevertheless reached the highest level in five years, according to preliminary data from the Cabinet Office. The gauge depicts strong performance in manufacturing and services sectors with the country’s economy appearing to be resilient to the Middle East energy shock and supply chain disruptions. The country’s Coincident Indicator, a gauge of current conditions, also strengthened, climbing 0.4% after April’s 1.3% advance.

Canada’s Trade Surplus Climbs

A 51% m/m jump in the value of unwrought aluminum and alloy shipments along with higher prices helped push Canada’s May trade surplus to a four-year high of C$4.24 billion, according to Statistics Canada. Economists anticipated a C$2.9 billion surplus after exports exceeded the value of imports by C$3.4 billion in April.

The value of merchandise shipped abroad in May climbed 0.9% m/m, marking the fourth consecutive month of expansion. May was also the fourth consecutive month of increased exports to the US with Canada’s southern neighbor spending 1.5% more on the country’s products. Canada also trimmed its purchases of US merchandise by 1.4%. As a result, Canada’s trade surplus with the US went from $10.3 billion in April to $11.6 billion in May, the strongest print since January 2025.

More broadly, Canada’s overall goods imports climbed in 9 of 11 product categories but the overall value edged down 0.2%. The weaker activity was driven by an 18% drop in purchases of metal and non-metallic mineral products. In this category, imports of semi-finished iron or steel products sank 22.7% while waste and scrap of metal sank 20%. Imports of basic and semi-finished products of non-ferrous metals and non-ferrous metal alloys, furthermore, fell 21.2%. Conversely, Canada’s purchases of batteries and battery chargers from China contributed to imports of consumer goods climbing 3.5%.

But Purchasing Managers’ Index Weakens

Canada’s Ivey Purchasing Managers’ Index fell from 58.2 in May to 56.2 last month, substantially missing the 59.1 level anticipated by a consensus of economists. The read was also a three-month low.

The following categories posted the stated declines from May to June:

- Ivey Employment Index, 54.3 to 53.6

- Ivey Supplier Deliveries Index, 44.7 to 44.2

- Ivey Prices Index, 78 to 73.7

Conversely, the Ivey Inventories Index advanced from 47.9 to 50.9

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Precious Metals

Precious metals may not be available in all locations, please check your local IBKR website for availability.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account