Risk-on winds are dominating Wall Street today as progress on the US-Iran negotiations raises optimism concerning a sustained retreat in crude oil and yields. A potential peace deal, which is offsetting the adverse impact of some overnight tensions between both nation’s militaries, would materially strengthen business fundamentals and the economic outlook. Revenues would be bolstered by widening household spending capacity in response to relief at the pump and lower borrowing costs. Corporate profit margins stand to benefit too against the backdrop of lighter fuel charges and interest expenses as well as narrowing credit spreads. A reported softer-than-anticipated decline in consumer confidence this morning also aided sentiment. Stocks are surging on the news because the promising Middle East development could conceivably provide an add-on to stellar rallies that have taken the indices in aggregate to double-digit year-to-date appreciation rates already with the Russell 2000, Nasdaq 100 and S&P 500 benchmarks all reaching fresh records this session. Sector participation is mixed, however, with tech, industrial and materials doing most of the heavy lifting as 6 of the major 11 categories ascend. In fixed income, the Treasury curve is sinking about 5 to 6 basis points throughout the complex as investors increasingly consider that the Fed may remain on hold in light of descending inflation expectations. Elsewhere, non-energy commodities and the greenback are advancing, cryptocurrencies are declining, and prediction markets are catching bids.

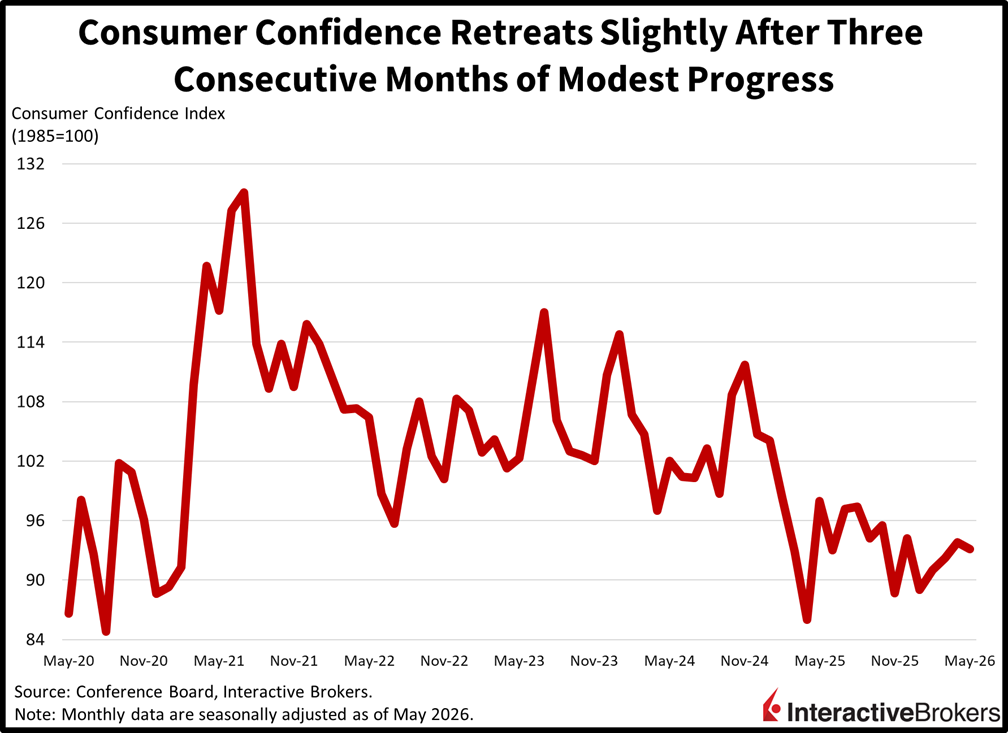

Consumer Confidence Falls Less than Expected

Consumer confidence declined in May following three consecutive months of modest progress, although survey respondents were increasingly optimistic about the road ahead rather than current conditions. The Conference Board’s headline figure of 93.1 depicted a lighter-than-anticipated fall as the median estimate stood at 92 while April’s print came in at 93.8. The present situation and expectations indices shifted in bifurcated fashion. The former dropped from 124.4 to 121.2 while the latter rose from 73.4 to 74.4. Households reflected worries about inflation from the war with pain at pump dominating conversations. Still, folks were more upbeat on business possibilities and job opportunities six months out.

Past performance is not indicative of future results.

Stocks Could Soar If WTI Sinks to $75, 10-Year to 4.20%

With the S&P 500 almost up 10% year to date while the Russell 2000 and Nasdaq 100 have appreciated nearly 20% in less than five months, stocks are bound to soar if there’s a lasting peace deal signed in the Middle East. WTI crude is poised to sink to $75 per barrel while the 10-year plunges to 4.20% if an agreement is reached, which would bode well for long-term inflation expectations, risk premiums and the economic outlook. Such a development would likely propel equities considerably through year-end assuming there are no volatility sparks along the way. In the meantime, however, Wall Street and the Fed will have to digest several Consumer Price Index reports coming in north of 4%.

International Roundup

Singapore MTI Maintains GDP Forecast

The Singapore Ministry of Trade and Industry is maintaining its February forecast for GDP to grow between 2% and 4% this year. It anticipates that global demand for AI products will continue, but the US-Iran war will trim overall foreign demand for the country’s products. Monetary policy worldwide is another headwind. Earlier this year, many central banks held accommodative policies, but with the closure of the Strait of Hormuz creating shortages of fertilizers, aluminum and energy commodities, the developments are increasingly causing organizations to adopt restrictive stances.

And Inflation is Stable

Singapore’s annualized inflation rate was unchanged in April while prices fell relative to March. The headline Consumer Price Index was up 1.8% year over year (y/y), slightly cooler than the economist consensus estimate of 2% and unchanged from the preceding month’s pace. The m/m metric showed a 0.3% decline following the 0.5% March climb. The Core CPI, which strips out certain items with volatile prices, was also benign with its annualized pace falling from 1.7% to 1.4%. Economists anticipated the same rate as in March.

Within the headline m/m print, housing and utilities sank 2.2%. The information and communication group and the clothing and footwear category, meanwhile, were down 1.5% and 0.5%. Categories with price increases and the extent of the changes were as follows:

- Transport, 1.6%

- Health, 0.4%

- Miscellaneous goods & services, 0.4%

- Food, 0.2%

- Household durables and services, 0.2%

- Recreation, sports and culture, 0.2%

- Education, 0.1%

Singapore Industrial Production Jumps

Singapore’s industry boosted production in April by 17.6% y/y and 5.8% m/m, easily surpassing the economist consensus estimates of 12% and 1.5% and the y/y and m/m March rates of 9.2% and 3.5%. When excluding biomedical manufacturing, results were even stronger, with output up 21.5% y/y. Within the y/y headline, electronics led the charge, soaring 44% and led by infocomms, consumer electronics and semiconductors. Accelerating global demand for AI products supercharged the category’s results. General manufacturing was also impressive, growing 16.9% with strong production of structural metal and beverages. Precision engineering and transport engineering, furthermore, were up 15.1% and 10.1%. Engineering services for production of AI were robust and airlines’ requests for aircraft parts, maintenance and overhaul were healthy. Weakness in medical device manufacturing and increasing costs of oil and other materials caused the biomedical manufacturing group and the chemicals sector to experience declines of 16.1% and 17.6%, respectively.

Investment Flows to China Weaken

China experienced a 10.3% y/y decline in foreign direct investments during the first four months of 2026 despite the US and various European countries plowing more money into the country’s economy. China is suffering from a glut of manufacturing capacity, but US companies increased their capital allocated to the country by 24.5% y/y. Luxembourg, Switzerland, and France also increased their investments by 110.3%, 60.8%, and 58.3%, respectively.

Canada’s Profits Climb on Higher Commodity Prices

First-quarter profits in Canada were up 2% from the final three months of 2025 with higher commodity prices shoring up results. When compared to the same quarter of 2025, profits were 3.4% higher.

Disclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account