Stocks are leaping to fresh record highs amidst broad sector participation as investors cheer positive US-China talks in Beijing. Sentiment was bolstered by an expectation that the world’s two largest economies will collaborate more, especially with top American CEOs participating to help grow cooperation across crucial themes like AI, manufacturing and supply chains. Meanwhile, the powerhouses seemed to agree that the Strait of Hormuz should be reopened, as the Middle East conflict continues to be top of mind for Wall Street against the backdrop of crude oil remaining well above $100 per barrel. Concerns about elevated energy costs are being offset by strong economic data, however, as the third consecutive month of retail sales expansion was accompanied by subdued unemployment claims, which points to a healthy consumer that is being supported by robust labor conditions. In trading, every major equity segment and subcategory is advancing ex materials and biotech, the greenback is strengthening, commodities are sinking, rates and volatility protection instruments are nearly unchanged.

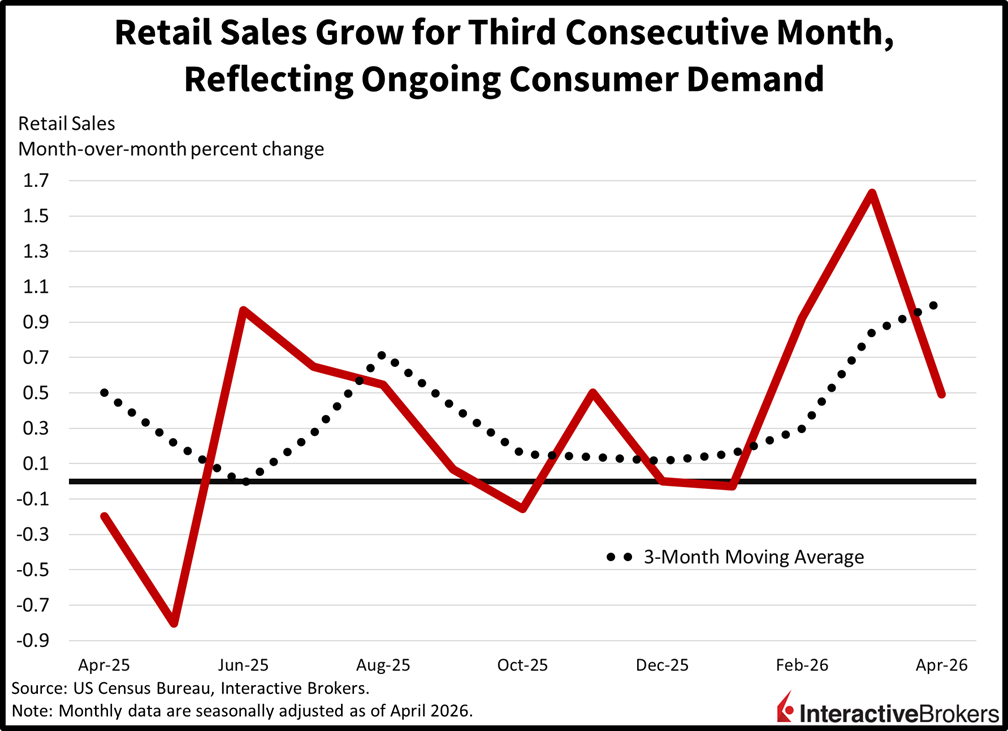

Shoppers Shrug off Higher Gasoline Prices

April retail sales expanded for the third consecutive month, reflecting a robust consumer that hasn’t had trouble managing rising costs. The 0.5% month-over-month (m/m) gain was exactly as expected and slowed from March’s 1.6% rate of expansion. The lift was broad-based, too, with nine of the thirteen major categories experiencing growth. Sellers focused on gasoline, electronics/appliances, sporting goods, ecommerce, food/beverage, restaurants/bars, miscellaneous items, building materials, and general merchandise saw revenues increase 2.8%, 1.4%, 1.4%, 1.1%, 0.8%, 0.6%, 0.3%, 0.1% and 0.1% m/m. Health and personal care stores were unchanged, while furniture, clothing and motor vehicles contracted 2%, 1.5% and 0.4%.

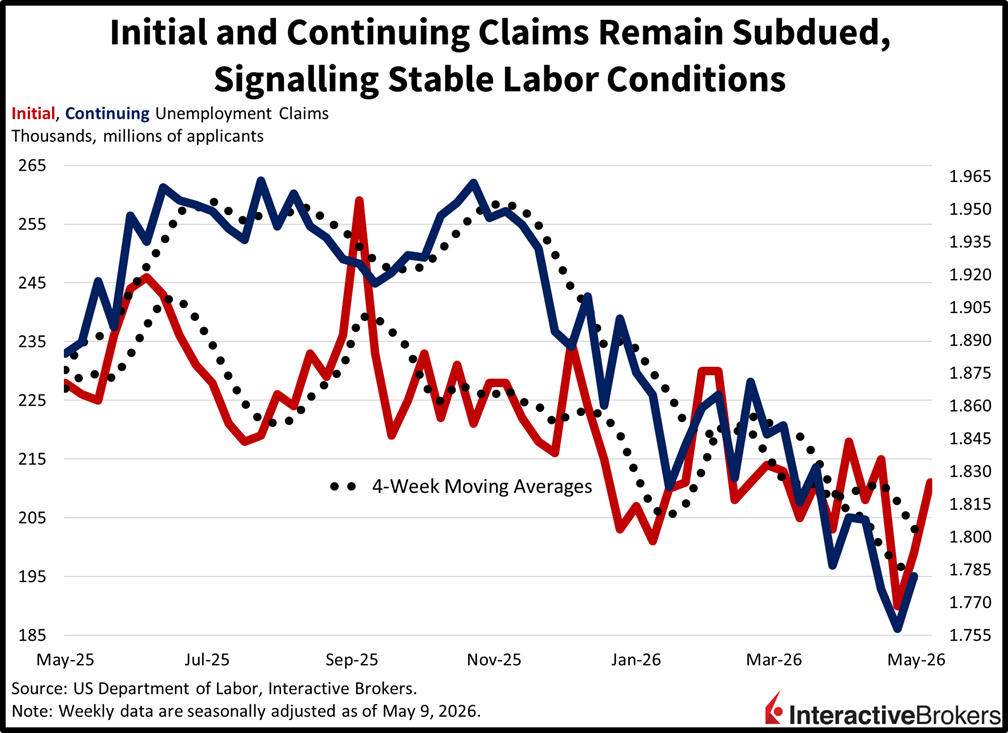

Benign Claims Point to Stable Labor

Labor conditions remain healthy, according to this morning’s unemployment claims release, which signaled the ongoing trend of subdued layoffs. Initial filings rose slightly to 211k during the week ended May 9, above the median estimate of 205k and the prior period’s 199k. Continuing applications also increased marginally, rising to 1.782 million, beneath the 1.79 million expectation and the 1.758 million from the previous interval. Four-week moving averages were pretty flat, coming in at 203.75k and 1.781 million.

China Discussions Great for Markets

The positivity regarding US-China talks is removing what could have been a significant risk for markets—the two nations not getting along. The amicable discussions are paving the way for further upside on Wall Street as fears of tariffs, AI restrictions and Beijing supporting Tehran are quelled. President Trump’s ability to thread the needle with Xi Jinping is additionally supporting Wall Street by improving investors’ confidence in the commander in chief’s ability to continue achieving foreign policy wins. Indeed, the Nasdaq 100 is up 16% year-to-date while the S&P 500 is closing in on 10% in what’s shaping up to be the fourth consecutive annum of double-digit percentage returns for equities. And with a long seven and a half months left in 2026, a 12-month period delivering gains in excess of 20% is certainly on the cards.

International Roundup

UK GDP Strengthens

First-quarter gross domestic product (GDP) growth in the UK accelerated but results for the final month of the reporting period were mixed, according to preliminary data from the Office for National Statistics. During the first quarter, construction, capital formation, production and services contributed to growth, although the administrative and support service activities category was a headwind.

The quarter-over-quarter (q/q) expansion of 0.6% matched the economist consensus estimate and accelerated from the 0.2% advance in the final quarter of 2025. GDP also quickened on a year-over-year (y/y) basis with its 1.1% pace exceeding both the preceding period’s 1% ascent and the 0.8% economist estimate. Output by the services sector jumped 0.8% during the first quarter, a much stronger showing than the 0.2% hike in the fourth quarter. It was also 1.4% higher than during the first three months of 2025. For the q/q print, consumer-facing services and the separate business sectors category were up 0.8% and 0.7%. However, output from the administrative and support service activities, which dropped 1.0%, largely due to declines in the employment activities component and the rental and leasing activities category. Output from the production sector, however, grew 0.2% q/q, a decline from 1.3% in the fourth quarter but flat relative to the year-ago period.

Within the q/q data, gains in manufacturing and electricity, gas, steam and air conditioning supply were offset by weakness in mining, quarrying, water supply, sewerage, waste management and remediation services. Also during the first quarter, construction output was up 0.4% q/q, but was down 1.3% y/y. New work activity contracted but repair and maintenance grew by 3.4% overall and by 4.1% for private residences. In another development, the q/q 0.7% ascent of first quarter business investment missed the consensus estimate of 1.1% but reversed from the 2.9% slip in the preceding period. Conversely, it was down 1.8% y/y after expanding by the same amount in the fourth quarter. More broadly, overall expenditure gains were driven by an uptick in gross capital formation, household consumption and government consumption. For March, GDP was up 1.2% y/y and 0.3% m/m compared to the 1% and 0.4% y/y and m/m growth in February. Economists anticipated a 0.7% y/y expansion and a 01% m/m contraction.

UK Trade Deficit Deepens

The UK’s goods trade deficit climbed from $22.8 billion in February to $27.2 billion in March, exceeding the economist consensus estimate for imports to exceed exports by $19.8 billion. Imports climbed 2.1% with purchases of goods from both the European Union and non-European countries growing. During the month, the value of refined oil and fuels imported by the UK climbed, primarily due to higher prices. The UK also increased its purchases of German automobiles. Meanwhile, imports of chemicals sank slightly. Meanwhile, a rise in shipments to European Union countries pushed the value of exports up by 1.9%. The flow of crude oil to the Netherlands rose and Germany increased its purchases of pharmaceutical and medicinal products. Italy, however, experienced a decline in demand for UK manufactured automobiles.

Canada Wholesaling Exceeds Estimates

The total value of transactions on the wholesale level in Canada was 1.9% higher in March than in the preceding month. The pace slowed from the 2.4% growth rate in February but exceeded the economist consensus estimate of 1.3%.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account