Originally posted, 9 August 2024 – Electric Vehicles: Tariffs Unlikely to Deter Growth as Incentives and Innovation Take Hold – Authored by: Andrew Ye, CFA

The recent imposition of tariffs on Chinese-made electric vehicles (EVs) by the United States and European Union raises concerns about the projected growth and adoption of EVs. However, ongoing government incentives, price competition, and infrastructure development continue to pave the way for potential EV growth. As price points continue to shift lower and ownership challenges are addressed, there is ample runway for long-term demand for EVs to possibly increase.

Key Takeaways

- It is believed that the potential impact of tariffs on Chinese-made EVs is overestimated, and that the EV market potentially has growth opportunities ahead.

- Government incentives, tax breaks, and price competition in China are helping sales in China, the world’s largest EV market. Recent expansion into emerging markets and Europe are potential growth areas.

- Ongoing innovation and expansion of charging infrastructure could address key EV ownership challenges and increase long-term demand for EVs.

Tariffs to Have Limited Impact on Global EV Sales

In May 2024, President Biden increased the U.S. tariff on Chinese-made EVs to 100%, citing unfair competition.1 After completing its investigation into unfair subsidies, the European Union announced in July that it would impose tariffs on Chinese-made EVs, including those manufactured by European brands.2

While the size of the U.S. tariff seems large, the U.S. only imported 12,362 EVs from China in 2023.3 These tariffs may be seen as more of a preventative measure. A slowdown in EU imports of Chinese-made EVs is a reasonable expectation, but even with the tariffs, pricing for some Chinese-made EV models remains below European rivals. In addition, Chinese carmakers generally have healthier margins in Europe than in China.4

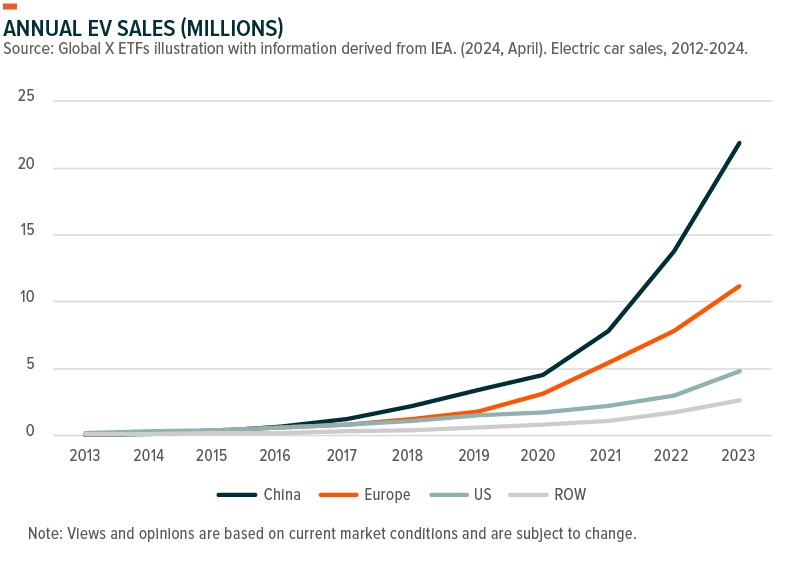

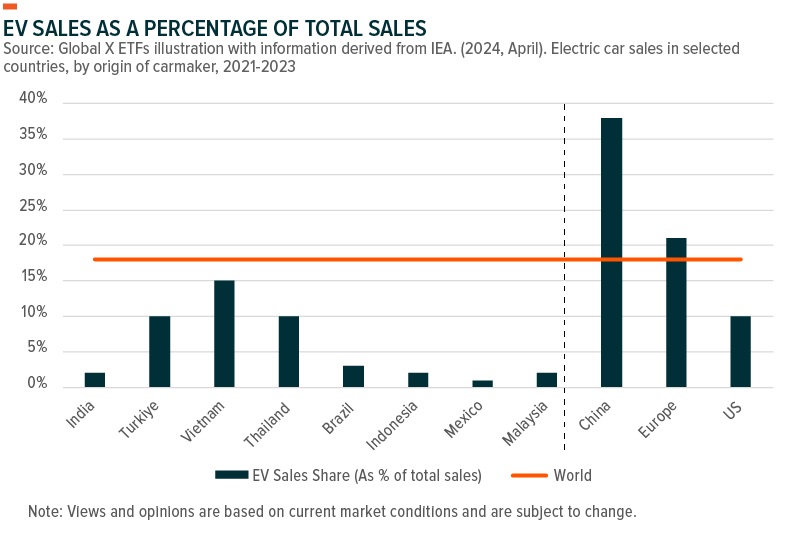

China remains the largest market for EV sales by a comfortable margin, accounting for more than 50% of global EV sales over the past two years.5 These tariffs are not expected to have much of an impact on China’s market share.

Government Support and Expansion Plans are Positives for Chinese EVs

A view on global EV sales requires an assessment of the Chinese domestic market. While national subsidies were phased out in 2022, other forms of state support and favourable policies may be capable of continuing to drive Chinese EV sales growth.

Despite the phase-out of the national EV subsidies in 2022, China still achieved 35% sales growth in 2023.6 In 2024, demand remains robust, helped by a purchase tax exemption in place until the end of 2025.7 In addition, regional governments are offering localised subsidies. For example, in late April the Beijing government announced a US$1,380 subsidy until the end of 2024 for EV buyers who replace their petrol cars.8 Another positive is competition among carmakers, which has led to steep discounting. The discounting is not limited to Chinese carmakers; notably, Tesla has cut its prices several times in the past year.9 These factors helped China’s new energy vehicle (NEV) sales rebound in June, with several carmakers posting record sales volumes.10

Chinese EV companies have begun focusing on offshore production as a means of accessing new markets. In July 2024, BYD opened a manufacturing plant in Thailand, its first factory in Southeast Asia.11 This factory followed the Thailand government’s announcement that it would expand incentives for consumers to purchase EVs.12 Several other Chinese carmakers, including Great Wall Motor and SAIC Motor, have also established manufacturing operations in Southeast Asia.13

In December 2023, BYD announced the construction of its first European manufacturing plant in Hungary.14 In July 2024, BYD announced plans to construct a $1 billion factory in Turkey, which is due to commence production at the end of 2026 and expected to manufacture 150,000 cars per year.15 This factory was the culmination of BYD’s search for a location for a European passenger car plant, which BYD Executive Vice President Stella Li first mentioned in a Bloomberg interview in December 2022.16 Beyond production, these facilities in Europe may also present potential opportunities to avoid EU tariffs put in place.

EV sales in the Rest of World are still low in absolute terms relative to China, the EU, and the US, the three biggest markets. The Rest of World accounted for just 6.4% of global EV sales in 2023. However, this cohort is expected to pick up the pace as EVs increase as a proportion of total car sales in emerging markets. Cheaper models might gain the bulk of the market share.

Addressing EV Ownership Concerns Through Funding and Innovation

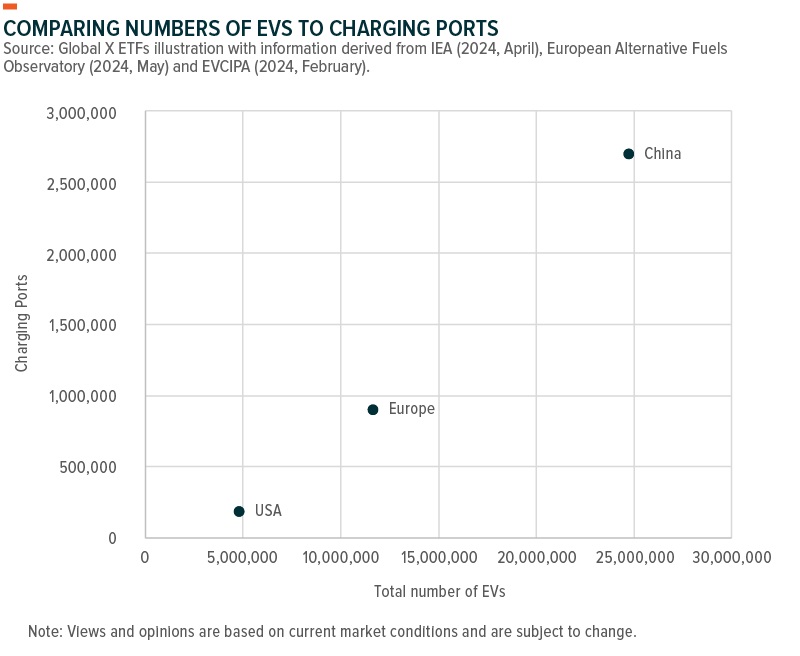

The continued rollout of EV charging infrastructure remains an important part of the solution to addressing concerns about range and charging times. A report by the European Automobile Manufacturer’s Association (ACEA) noted that 61% of the EU’s 632,423 charging points were in just three countries, the Netherlands, France and Germany as of year-end 2023.17 Only 13.5% of the chargers have fast-charging capabilities.18

Targeted policies and funding are required to meet the EU’s goal of 3.5 million chargers by 2030.19 In the United States, President Biden set a target of 500,000 chargers by 2030.20 However, the National Renewable Energy Laboratory projects that the country needs 1.2 million chargers, based on the assumption of 33 million EVs.21 The Infrastructure Investment and Jobs Act (IIJA) directs $7.5 billion to build out a national network of EV charging stations as part of the New Electric Infrastructure (NEVI) Formula Program and the Charging and Fuelling Grant Program.22 Continued public and private funding will be critical to the development of EV infrastructure and increasing global EV adoption.

Range anxiety also remains a deterrent for potential EV buyers, despite advancements in charging infrastructure and battery technology extending the range of new EVs. A possible solution, as a complement to traditional EV charging infrastructure, is battery swapping. The idea of quickly exchanging a discharged battery for a fully charged battery is not new. Tesla piloted the technology in 2014,23 but did not to pursue it due to insufficient demand to make it economically viable.24

A decade later, the size of the global EV market and increasing adoption rates may address previous doubts about the scale and demand for battery swapping. Challenges persist, but recent developments suggest progress. At the end of 2023, Chinese carmaker Nio had installed 2,300 battery swap stations across China, and it plans to install 1,000 more in 2024.25 As of 8 August 2024, Nio has now swapped over 50 million batteries in total,26 a process that now takes less than five minutes.

Aiming to establish industry standards for swappable batteries and expand the service network, Nio formed a battery swap alliance with five other Chinese carmakers.27 Nio also partnered with Chinese electricity producers and grid operators to enhance grid services and make its battery swapping stations more efficient.28

In Europe, Stellantis, the conglomerate that owns 14 brands, including Citroën, Fiat, and Peugeot, partnered with California-based battery-swapping company Ample to trial the technology.29 If there is strong demand, large automotive groups like Stellantis could standardise and integrate this technology across its brand portfolio.

Autonomous driving is another key area that may boost global EV adoption and sales. After over 3.8 million miles of testing, Waymo, a subsidiary of Alphabet, recently opened its fully automated Waymo One service in San Francisco.30 Anyone in San Francisco can download the app and hail a ride in a fully automated vehicle. In addition, China recently approved Level 3 automated driving trials on public roads for nine Chinese carmakers. 31

Conclusion: Overcoming Obstacles to Drive Global EV Sales

U.S. and EU tariffs on Chinese-made vehicles may seem like roadblocks, but we view them more as bumps in the road that are potentially unlikely to significantly impact China’s EV market or global EV sales. Ongoing EV innovation, improvement and expansion in charging infrastructure, and government-led incentives may continue to attract new EV buyers. Furthermore, EVs becoming less expensive due to a combination of advancing technology, original equipment manufacturer (OEM) discounting, and government incentives could facilitate expansion into new markets and increase their total addressable market.

This document is not intended to be, or does not constitute, investment research

Disclosure: Interactive Brokers Third Party

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Global X ETFs Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or Global X ETFs Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account