A $50 billion lift in Micron’s domestic capital expenditure plans is reviving the semiconductor trade by strengthening the case that the AI build-out remains in its early innings. The announcement is bolstering tech enthusiasm and has the Nasdaq 100 leading benchmark gains amidst all of the major indices advancing alongside 8 of the 11 sectors in the green. The rebound is transpiring even as the Magnificent 7 names fail to participate much in this session’s advance due to uncertain return prospects tied to their significant investments in the modern infrastructure. Investor sentiment is also improving as a result of plummeting crude prices as participants gauge that President Trump doesn’t want intense Middle East hostilities occurring prior to a midterm election in which the Republicans carry just a narrow lead in sustaining their Senate majority. Those tumbling oil and natural gas costs, meanwhile, are helping to loosen financial conditions via subdued Fed hike expectations, plunging yields and a depreciating greenback, factors that are conducive to buoyant stock buying. Non-energy commodities are additionally benefiting from the resurgence in animal spirits, however, with precious metals and copper especially driving the train. Hedging interest is waning in light of the risk-on attitude on Wall Street, with volatility protection instruments seeing lighter premiums.

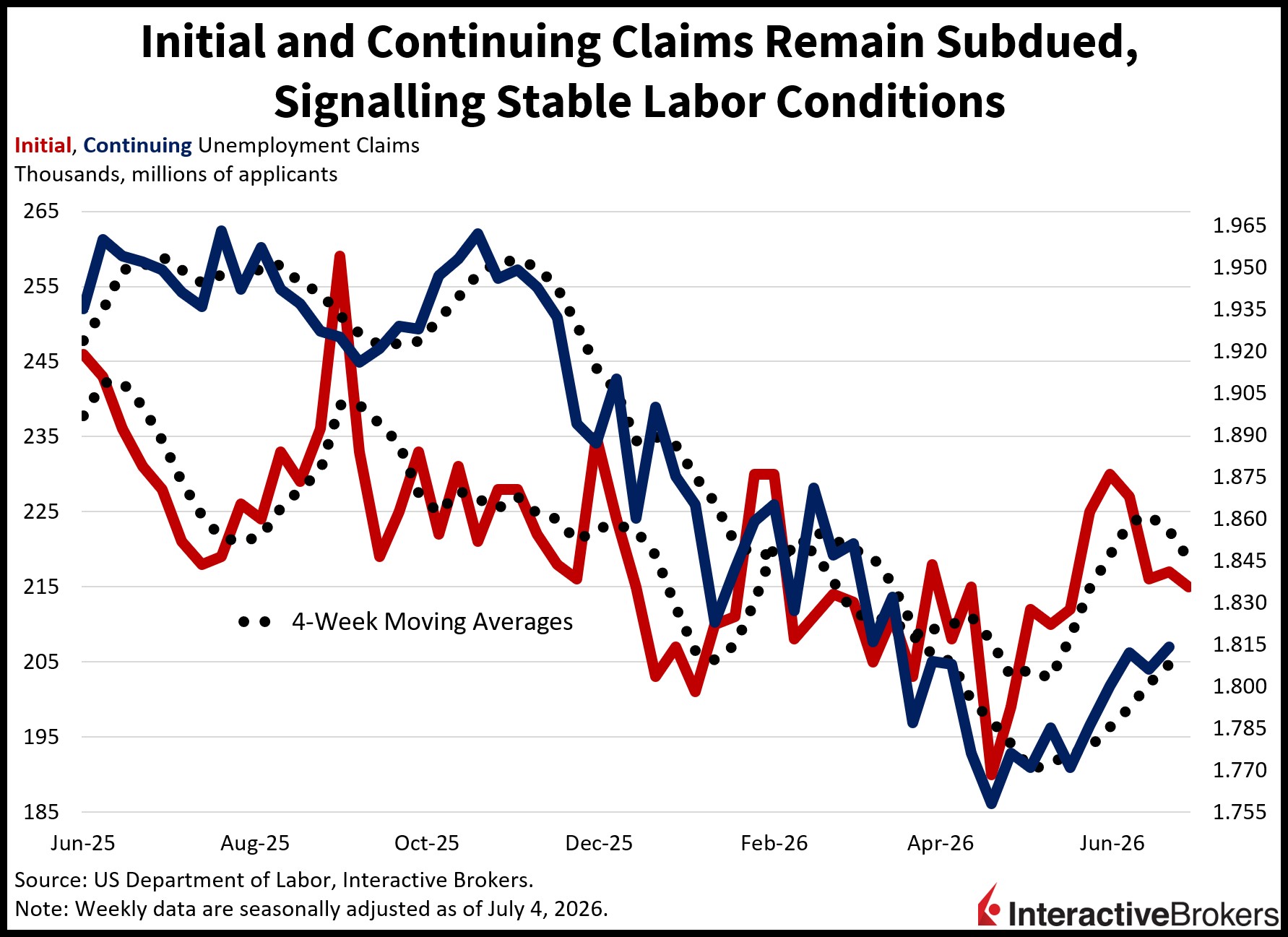

Unemployment Claims Stay in the Zone

Claims for unemployment benefits for the past two-week period continued to depict a stable job market with employers refraining from layoffs. Initial filings declined to 215k during the interval that ended July 4, dropping below the 218k economist consensus estimate and the preceding period’s 217k. Continuing applications rose modestly to 1.814 million through the time span culminating on June 27, considerably below the 1.820 million anticipated. In the preceding period, continuing claims totaled 1.80 million. Four-week moving averages shifted in bifurcation fashion from 222.5k and 1.801 million to 218.7k and 1.808 million.

Past performance is not indicative of future results.

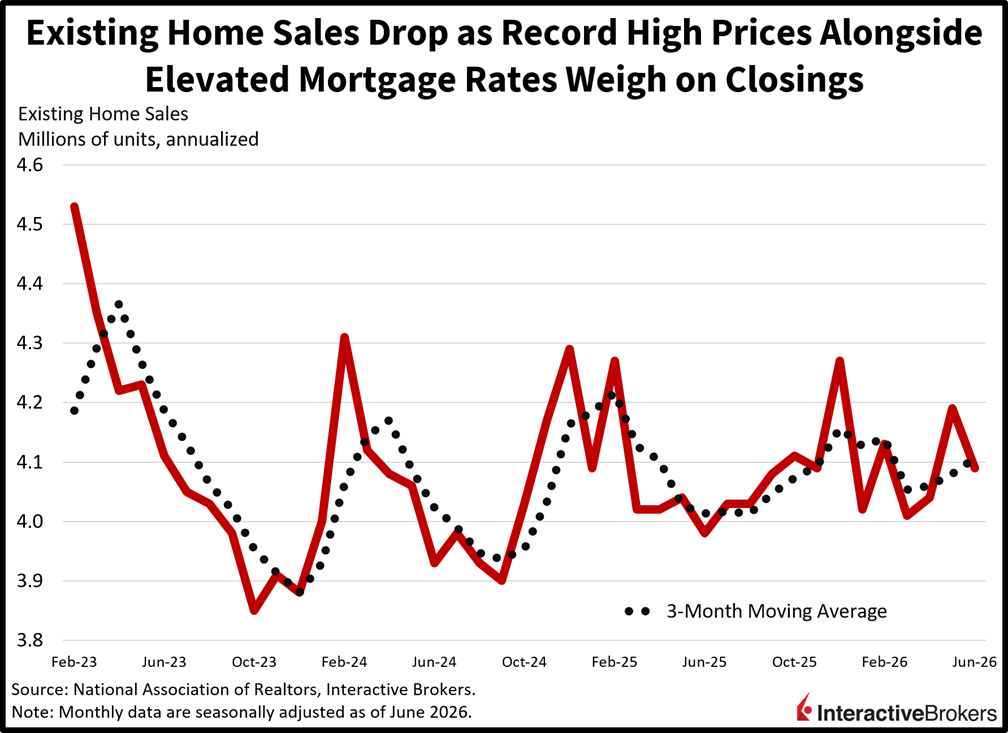

All-Time High Prices Stymie Existing Home Sales

Existing home sales fell in June, snapping a two-month streak of increases as record-high prices pushed potential buyers out of the market, according to the National Association of Realtors. The 4.09 million seasonally adjusted annualized units (SAAU) sold was a 2.4% month-over-month (m/m) decline and below the projection for a repeat of May’s 4.19 million transactions. It was also a reversal from May’s 3.7% m/m increase. The weakness was broad as follows:

- The condominiums and co-ops segment registered a 2.7% m/m decline

- The single-family segment posted a 2.4% m/m drop

Among regions, the Northeast was an outlier, posting a 2.1% m/m increase. In other regions, the Midwest, South and West experienced declines of 3%, 3.6% and 1.3%, respectively. Despite the contraction in property deeds switching hands, inventory fell 0.6% from May. Meanwhile, the median existing home price climbed 1.8% year over year (y/y) to $460,600, an all-time high. The average mortgage rate, furthermore, at 6.49%, remained nearly unchanged from 6.44% in May. Nevertheless, it was down from 6.82% in the year-ago period.

Past performance is not indicative of future results.

Bonds Make Sense as a Hedge Here

Yields are far too elevated at the long end of the curve at this juncture and bonds have several paths to meaningful appreciation as follows:

- A relaxation in geopolitical tensions that brings oil back into the 60s. President Trump has incentives to try and keep gasoline prices low heading into the midterm elections, especially in consideration of a narrow GOP Senate lead as shown by prediction markets.

- The worst inflation is behind us as the Consumer Price Index (CPI) almost certainly peaked at 4.2% in May. As the CPI heads back into the mid to low 3s this autumn, the 20- and 30-year maturities are poised to drop at least 25 basis points (bps). Their current levels of approximately 5.08% across both durations are likely 200 bps north of a CPI trough of 3.1% before year-end, and that spread is far too wide from a historical perspective.

- There’s a strong chance that the elevated interest rates of today will soften momentum in the labor market. While jobs have surprised to the upside significantly in the first half of the year, it’s likely that employment will continue its modest deceleration of recent months because labor supply is too constrained when considering the restrictive immigration situation. Additionally, growing AI adoption is weighing on worker demand in big-tech and finance. Yields are too elevated as well for rate-sensitive small biz, manufacturing and construction to contribute more and serve as positive offsetting factors.

- The cure for elevated yields may end up being elevated yields, eventually slowing hiring, investment and consumer spending while subsequently delivering strong gains to duration longs.

- Fed Chair Warsh remaining hawkish and focused squarely on the inflation side of the central bank’s dual-mandate is likely to weigh on longer-term growth expectations and invert the curve as the fixed-income complex incrementally lifts recession risk stemming from tight policy.

- The equity risk premium is quite low here, so some duration as a hedge makes sense against the backdrop of a weak seasonal period of stocks coming up in August and September that could benefit a defensive bond trade.

International Roundup

China’s Retail Inflation Slows but Climb of Wholesale Charges Accelerates

Consumer price pressures eased in China last month, but wholesale inflation intensified, marking the fifth consecutive month in which businesses fetched more for their products rather than having to lower their stickers.

The CPI was down by 0.3% m/m after falling 0.1% in May. An economic consensus called for prices to slip 0.2%. Relative to the year-ago period, consumers dished out 1% more compared to the 1.2% y/y climb in May. Economists anticipated a 1.1% pace. The June core CPI, which strips out food and energy, matched the broader index’s result after hitting 1.1% in the preceding month. June’s y/y headline was dampened by food prices falling 1.6% after sinking 1.7% in the preceding month. Other items climbed 1.5%, a deceleration from 1.9% in May. Within that category, industrial sticker growth eased from 3.9% to 2.9%. Services became 0.8% more expensive.

Gate prices, meanwhile, were up 4.1% y/y, matching the economist consensus estimate and accelerating from 3.9%. When compared to May, however, prices were down 0.3%, a result of softer global oil prices. The y/y print reflects the elevated base effect, or a comparison to a low number y/y. Indeed, wholesale prices declined every month from October 2022 until February of this year, and in the year-ago period, gate prices registered a 12-month 3.6% decline. Coal mining, electrical machinery, ferrous metals and electronics also contributed to the higher y/y print.

New to Interactive Brokers?

Open AccountDisclosure: Interactive Brokers Affiliate

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Precious Metals

Precious metals may not be available in all locations, please check your local IBKR website for availability.

Join The Conversation

If you have a general question, it may already be covered in our FAQs page. go to: IBKR Ireland FAQs or IBKR U.K. FAQs. If you have an account-specific question or concern, please reach out to Client Services: IBKR Ireland or IBKR U.K..

Visit IBKR U.K. Open an IBKR U.K. Account